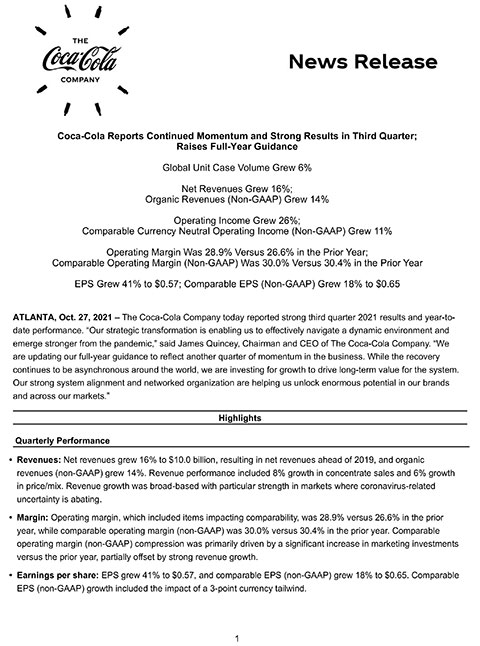

Coca-Cola Reports Continued Momentum and Strong Results in Third Quarter; Raises Full-Year Guidance

Coca-Cola Reports Continued Momentum and Strong Results in Third Quarter; Raises Full-Year Guidance

Global Unit Case Volume Grew 6%

Net Revenues Grew 16%;

Organic Revenues (Non-GAAP) Grew 14%

Operating Income Grew 26%;

Comparable Currency Neutral Operating Income (Non-GAAP) Grew 11%

Operating Margin Was 28.9% Versus 26.6% in the Prior Year;

Comparable Operating Margin (Non-GAAP) Was 30.0% Versus 30.4% in the Prior Year

EPS Grew 41% to $0.57; Comparable EPS (Non-GAAP) Grew 18% to $0.65

ATLANTA--(BUSINESS WIRE)--The Coca-Cola Company today reported strong third quarter 2021 results and year-to-date performance. “Our strategic transformation is enabling us to effectively navigate a dynamic environment and emerge stronger from the pandemic,” said James Quincey, Chairman and CEO of The Coca-Cola Company. “We are updating our full-year guidance to reflect another quarter of momentum in the business. While the recovery continues to be asynchronous around the world, we are investing for growth to drive long-term value for the system. Our strong system alignment and networked organization are helping us unlock enormous potential in our brands and across our markets.”

Highlights |

Quarterly Performance |

- Revenues: Net revenues grew 16% to $10.0 billion, resulting in net revenues ahead of 2019, and organic revenues (non-GAAP) grew 14%. Revenue performance included 8% growth in concentrate sales and 6% growth in price/mix. Revenue growth was broad-based with particular strength in markets where coronavirus-related uncertainty is abating.

- Margin: Operating margin, which included items impacting comparability, was 28.9% versus 26.6% in the prior year, while comparable operating margin (non-GAAP) was 30.0% versus 30.4% in the prior year. Comparable operating margin (non-GAAP) compression was primarily driven by a significant increase in marketing investments versus the prior year, partially offset by strong revenue growth.

- Earnings per share: EPS grew 41% to $0.57, and comparable EPS (non-GAAP) grew 18% to $0.65. Comparable EPS (non-GAAP) growth included the impact of a 3-point currency tailwind.

- Market share: The company gained value share in total nonalcoholic ready-to-drink (NARTD) beverages, which included share gains in both at-home and away-from-home channels. The company’s value share in total NARTD beverages remains ahead of the 2019 level.

- Cash flow: Year-to-date cash flow from operations was $9.2 billion, up $3.0 billion versus the prior year, driven by strong business performance, five additional days in the first quarter and working capital initiatives. Year-to-date free cash flow (non-GAAP) was $8.5 billion, up $3.0 billion versus the prior year, driven by strong cash flow from operations.

Company Updates |

- Business environment: Global unit case volume continued to benefit from ongoing recovery in many markets. Third quarter volume was ahead of 2019, and there was sequential improvement in volume versus the second quarter on a two-year basis driven by improved performance in away-from-home channels along with continued strength in at-home channels. While recovery continues to look different across markets and the supply chain environment remains dynamic, the company is progressing on its strategic transformation and is leveraging the networked organization to drive growth for the system.

- Engaging and attracting consumers through a new platform for Trademark Coca-Cola: The company has launched a new brand platform for Trademark Coca-Cola called “Real Magic,” the first in five years. The “Real Magic” brand philosophy is rooted in the insight that magic lives in unexpected moments of connection that elevate the everyday into the extraordinary. The platform includes a new design identity for the trademark, including a fresh expression called the Coca-Cola “Hug” logo. The company will engage consumers with experiences anchored in consumption occasions, such as meals and breaks, and aligned with consumer passion points like music, gaming and sports. The company launched the “Real Magic” platform with the “One Coke Away From Each Other” campaign, which runs through October and includes social, digital and out-of-home executions.

- Commitment to a World Without Waste: In 2018, the company launched the World Without Waste strategy, renewing a focus on creating a circular economy for plastic packaging and eliminating waste in the environment. In line with this strategy, the company made important changes to its policies, goals and partnerships. The company remains committed to being part of the solution to the plastics pollution problem and has made progress, but there is still much more to do. In a recently released report on plastic pollution from As You Sow, the company scored the highest (out of 50 companies) for its efforts in reducing plastic pollution, including its strong commitment to recycling, transparency for its packaging use and support for producer responsibility initiatives. Earlier this month, the company revealed a breakthrough prototype bottle – its first to be made from 100% plant-based plastic (bPET), excluding cap and label, produced using technologies that are intended to be commercially scaled and that have a lower carbon footprint than virgin oil-based plastics. Additionally, the system continues to make key investments to ensure access to recycled-content packaging material. The company’s bottling partner in Indonesia and Dynapack Asia announced the construction of a PET recycling facility in West Java that will create a closed-loop plastic packaging supply chain.

- Leveraging a streamlined portfolio to fuel the innovation pipeline: The company is building a strong innovation pipeline that leverages big bets as well as intelligent experimentation. The networked organization is lifting and shifting several local and regional brands to additional markets around the world, including Costa® ready-to-drink, in the key markets of Japan and China, and the dairy brand fairlife™ in China. The scaled launch of new and improved Coca-Cola® Zero Sugar has resulted in an increase in key consumer metrics and contributed approximately 25% of Trademark Coca-Cola’s growth in the third quarter. The company also continues to be consumer centric by using intelligent experimentation at the local market level, including the launch of Aquarius® with functional benefits and the extension of the Ayataka® tea brand with Ayataka Cafè in Japan.

Operating Review – Three Months Ended October 1, 2021 |

Revenues and Volume |

|||||||||

Percent Change |

Concentrate

|

Price/Mix |

Currency

|

Acquisitions,

|

Reported Net

|

|

Organic

|

|

Unit Case

|

Consolidated |

8 |

6 |

2 |

0 |

16 |

|

14 |

|

6 |

Europe, Middle East & Africa |

8 |

5 |

0 |

0 |

13 |

|

13 |

|

8 |

Latin America |

11 |

23 |

7 |

0 |

41 |

|

33 |

|

8 |

North America |

7 |

5 |

0 |

0 |

13 |

|

13 |

|

4 |

Asia Pacific |

5 |

(3) |

2 |

0 |

3 |

|

2 |

|

3 |

Global Ventures3 |

20 |

19 |

8 |

0 |

47 |

|

39 |

|

15 |

Bottling Investments |

3 |

6 |

4 |

0 |

13 |

|

9 |

|

3 |

Operating Income and EPS |

||||

Percent Change |

Reported

|

Items

|

Currency

|

Comparable

|

Consolidated |

26 |

12 |

3 |

11 |

Europe, Middle East & Africa |

14 |

4 |

0 |

10 |

Latin America |

48 |

8 |

10 |

30 |

North America |

19 |

6 |

0 |

13 |

Asia Pacific |

5 |

5 |

2 |

(2) |

Global Ventures |

—4 |

— |

— |

— |

Bottling Investments |

48 |

(33) |

41 |

41 |

|

|

|

|

|

Percent Change |

Reported EPS |

Items

|

Currency

|

Comparable

|

Consolidated EPS |

41 |

24 |

3 |

14 |

| Note: Certain rows may not add due to rounding. | |

1 |

For Bottling Investments, this represents the percent change in net revenues attributable to the increase (decrease) in unit case volume computed based on total sales (rather than average daily sales) in each of the corresponding periods after considering the impact of structural changes, if any. |

2 |

Organic revenues, comparable currency neutral operating income and comparable currency neutral EPS are non-GAAP financial measures. Refer to the Reconciliation of GAAP and Non-GAAP Financial Measures section. |

3 |

Due to the combination of multiple business models in the Global Ventures operating segment, the composition of concentrate sales and price/mix may fluctuate materially on a periodic basis. Therefore, the company places greater focus on revenue growth as the best indicator of underlying performance of the Global Ventures operating segment. |

4 |

Reported operating income for Global Ventures for the three months ended October 1, 2021 was $114 million. Reported operating loss for Global Ventures for the three months ended September 25, 2020 was $31 million. Therefore, the percent change is not meaningful. |

In addition to the data in the preceding tables, operating results included the following:

Consolidated |

- Unit case volume grew 6% in the quarter, resulting in volume ahead of 2019, primarily led by developing and emerging markets. This was driven by ongoing recovery in markets where coronavirus-related uncertainty is abating, along with the benefit from cycling the impact of the pandemic last year. Growth in developing and emerging markets was led by India, Russia and Brazil, while growth in developed markets was led by the United States, Great Britain and Mexico.

Category performance was as follows:

- Sparkling soft drinks grew 6%, resulting in volume ahead of 2019, driven by strong performance across all geographic operating segments. Trademark Coca-Cola grew 5%, resulting in volume ahead of 2019, led by Europe, Middle East & Africa and Latin America. Sparkling flavors grew 7%, resulting in even performance on a two-year basis, led by solid growth in both Trademark Sprite and Trademark Fanta.

- Nutrition, juice, dairy and plant-based beverages grew 12%, a low single-digit acceleration versus 2019, due to solid performance by Minute Maid® Pulpy in China, Maaza® in India and Del Valle® in Mexico.

- Hydration, sports, coffee and tea grew 6%. Hydration grew 5%, with growth across all geographic operating segments. Sports drinks grew 5%, resulting in volume ahead of 2019, primarily driven by the United States and Mexico. Tea grew 4%, led by growth in Hajime™ in Japan and Gold Peak® in the United States. Coffee grew 19%, primarily driven by the ongoing reopening of Costa® retail stores in the United Kingdom as coronavirus-related uncertainty continued to abate.

- Price/mix grew 6% for the quarter, primarily driven by pricing actions in the marketplace along with favorable channel and package mix due to cycling the impact of the pandemic last year. Concentrate sales were 2 points ahead of unit case volume in the quarter, primarily attributable to bottler inventory build to manage through near-term supply disruption. Year-to-date concentrate sales were 5 points ahead of unit case volume, primarily due to five additional days in the first quarter, along with cycling the timing of shipments in the prior year.

Operating income grew 26%, which included items impacting comparability and a 4-point currency tailwind. Comparable currency neutral operating income (non-GAAP) grew 11%, driven by strong organic revenue (non-GAAP) growth across all operating segments, partially offset by a significant increase in marketing investments versus the prior year.

Europe, Middle East & Africa |

- Unit case volume grew 8% in the quarter, a low single-digit acceleration versus 2019, driven by ongoing recovery in markets where coronavirus-related uncertainty is abating, along with the benefit from cycling the impact of the pandemic last year. Growth was led by Russia and Great Britain in Europe, Nigeria in Africa, and Turkey in Eurasia and Middle East.

- Price/mix grew 5% for the quarter, driven by favorable channel and package mix due to cycling the impact of the pandemic last year, along with the timing of deductions. Year-to-date concentrate sales were 6 points ahead of unit case volume, primarily due to five additional days in the first quarter, along with cycling the timing of shipments in the prior year.

- Operating income grew 14%, which included items impacting comparability. Comparable currency neutral operating income (non-GAAP) grew 10%, primarily driven by strong organic revenue (non-GAAP) growth across all operating units, partially offset by a significant increase in marketing investments versus the prior year.

- The company gained value share in total NARTD beverages, which included share gains across most categories.

Latin America |

- Unit case volume grew 8% in the quarter, resulting in volume ahead of 2019. On a two-year basis, away-from-home volume improved sequentially versus the second quarter, while at-home volume remained strong. Growth was led by Mexico, Brazil and Argentina, driven by solid performance of Trademark Coca-Cola and the hydration category.

- Price/mix grew 23%, driven by pricing actions in the marketplace along with favorable channel and package mix. For the quarter, concentrate sales were 3 points ahead of unit case volume, primarily attributable to bottler inventory build to manage through near-term supply disruption. Year-to-date concentrate sales were 6 points ahead of unit case volume, primarily due to five additional days in the first quarter and the timing of shipments in the current year.

- Operating income grew 48%, which included items impacting comparability and a 12-point currency tailwind. Comparable currency neutral operating income (non-GAAP) grew 30%, driven by strong organic revenue (non-GAAP) growth, partially offset by nearly doubling marketing investments versus the prior year.

- The company lost value share in total NARTD beverages as share gains in Brazil and Argentina were more than offset by share losses in Mexico and Bolivia.

North America |

- Unit case volume grew 4% in the quarter. Growth was driven by recovery in the fountain business as coronavirus-related uncertainty continued to abate. Sparkling flavors and juice led the growth during the quarter.

- Price/mix grew 5% for the quarter, primarily driven by pricing actions in the marketplace, recovery in the fountain business and away-from-home channels, and solid growth in juice and dairy finished-goods brands. For the quarter, concentrate sales were 3 points ahead of unit case volume, primarily due to the timing of shipments in the current year. Year-to-date concentrate sales were 3 points ahead of unit case volume, primarily due to five additional days in the first quarter.

- Operating income grew 19%, which included items impacting comparability. Comparable currency neutral operating income (non-GAAP) grew 13%, driven by strong organic revenue (non-GAAP) growth, partially offset by a significant increase in marketing investments versus the prior year.

- The company gained value share in total NARTD beverages led by recovery in away-from-home channels along with strong performance in at-home channels for sparkling flavors, sports drinks and dairy.

Asia Pacific |

- Unit case volume grew 3% in the quarter, resulting in even performance on a two-year basis. Growth was driven by India and China, partially offset by pressure in Southeast Asia due to the impact of the pandemic. Growth was led by Trademark Coca-Cola and sparkling flavors.

- Price/mix declined 3%, negatively impacted by 3 points of geographic mix due to growth in emerging and developing markets outpacing developed markets. For the quarter, concentrate sales were 2 points ahead of unit case volume, primarily attributable to bottler inventory build to manage through near-term supply disruption. Year-to-date concentrate sales were 4 points ahead of unit case volume, primarily due to five additional days in the first quarter and the timing of shipments in the current year.

- Operating income grew 5%, which included a 2-point currency tailwind. Comparable currency neutral operating income (non-GAAP) declined 2%, driven by a significant increase in marketing investments versus the prior year, partially offset by solid organic revenue (non-GAAP) growth.

- The company gained value share in total NARTD beverages driven by share gains in Japan and the Philippines.

Global Ventures |

- Net revenues grew 47% in the quarter, which included an 8-point currency tailwind. Organic revenues (non-GAAP) grew 39%. Revenue growth was primarily driven by the ongoing reopening of Costa retail stores in the United Kingdom as coronavirus-related uncertainty continued to abate.

- Operating income growth and comparable currency neutral operating income (non-GAAP) growth were driven by strong organic revenue (non-GAAP) growth.

Bottling Investments |

- Unit case volume grew 3% in the quarter. Strong growth in India and South Africa was partially offset by pressure in Southeast Asia due to the impact of the pandemic.

- Price/mix grew 6%, driven by pricing and trade promotion optimization in most markets, along with a benefit from category and package mix.

- Operating income growth of 48% included a headwind from items impacting comparability and a 32-point tailwind from currency. Comparable currency neutral operating income (non-GAAP) grew 41%, driven by solid organic revenue (non-GAAP) growth along with effective cost management.

Operating Review – Nine Months Ended October 1, 2021 |

Revenues and Volume |

|||||||||

Percent Change |

Concentrate

|

Price/Mix |

Currency

|

Acquisitions,

|

Reported Net

|

|

Organic

|

|

Unit Case

|

Consolidated |

13 |

5 |

2 |

0 |

20 |

|

18 |

|

8 |

Europe, Middle East & Africa |

15 |

4 |

2 |

0 |

20 |

|

18 |

|

9 |

Latin America |

13 |

12 |

(1) |

0 |

25 |

|

26 |

|

7 |

North America |

8 |

7 |

0 |

0 |

14 |

|

14 |

|

5 |

Asia Pacific |

13 |

0 |

4 |

0 |

17 |

|

13 |

|

9 |

Global Ventures3 |

24 |

13 |

10 |

0 |

47 |

|

37 |

|

18 |

Bottling Investments |

13 |

5 |

3 |

0 |

21 |

|

18 |

|

11 |

Operating Income and EPS |

||||

Percent Change |

Reported

|

Items

|

Currency

|

Comparable

|

Consolidated |

30 |

8 |

2 |

20 |

Europe, Middle East & Africa |

16 |

(1) |

2 |

15 |

Latin America |

27 |

2 |

0 |

25 |

North America |

63 |

36 |

0 |

26 |

Asia Pacific |

18 |

2 |

6 |

11 |

Global Ventures |

—4 |

— |

— |

— |

Bottling Investments |

142 |

37 |

(10) |

115 |

|

|

|

|

|

Percent Change |

Reported EPS |

Items

|

Currency

|

Comparable

|

Consolidated EPS |

16 |

(10) |

2 |

24 |

| Note: Certain rows may not add due to rounding. | |

| 1 | For Bottling Investments, this represents the percent change in net revenues attributable to the increase (decrease) in unit case volume computed based on total sales (rather than average daily sales) in each of the corresponding periods after considering the impact of structural changes, if any. |

| 2 | Organic revenues, comparable currency neutral operating income and comparable currency neutral EPS are non-GAAP financial measures. Refer to the Reconciliation of GAAP and Non-GAAP Financial Measures section. |

| 3 | Due to the combination of multiple business models in the Global Ventures operating segment, the composition of concentrate sales and price/mix may fluctuate materially on a periodic basis. Therefore, the company places greater focus on revenue growth as the best indicator of underlying performance of the Global Ventures operating segment. |

4 |

Reported operating income for Global Ventures for the nine months ended October 1, 2021 was $215 million. Reported operating loss for Global Ventures for the nine months ended September 25, 2020 was $114 million. Therefore, the percent change is not meaningful. |

Outlook |

The 2021 and 2022 outlook information provided below includes forward-looking non-GAAP financial measures, which management uses in measuring performance. The company is not able to reconcile full year 2021 projected organic revenues (non-GAAP) to full year 2021 projected reported net revenues, full year 2021 projected comparable net revenues (non-GAAP) to full year 2021 projected reported net revenues, full year 2021 projected underlying effective tax rate (non-GAAP) to full year 2021 projected reported effective tax rate, full year 2021 projected comparable EPS (non-GAAP) to full year 2021 projected reported EPS, full year 2022 projected comparable net revenues (non-GAAP) to full year 2022 projected reported net revenues, full year 2022 projected comparable cost of goods sold (non-GAAP) to full year 2022 projected reported cost of goods sold, or full year 2022 projected comparable EPS (non-GAAP) to full year 2022 projected reported EPS without unreasonable efforts because it is not possible to predict with a reasonable degree of certainty the actual impact of changes in foreign currency exchange rates throughout 2021 and 2022; the exact timing and amount of acquisitions, divestitures and/or structural changes throughout 2021 and 2022; the exact timing and amount of items impacting comparability throughout 2021 and 2022; and the actual impact of changes in commodity costs throughout 2022. The unavailable information could have a significant impact on the company’s full year 2021 and full year 2022 reported financial results.

Full Year 2021

The company expects to deliver organic revenue (non-GAAP) growth of 13% to 14%. – Updated

For comparable net revenues (non-GAAP), the company expects a 1% to 2% currency tailwind based on the current rates and including the impact of hedged positions. – Unchanged

The company’s underlying effective tax rate (non-GAAP) is estimated to be 18.6%. This does not include the impact of the ongoing tax litigation with the U.S. Internal Revenue Service, if the company were not to prevail. – Updated

Given the above considerations, the company expects to deliver comparable EPS (non-GAAP) growth of 15% to 17% versus $1.95 in 2020. – Updated

Comparable EPS (non-GAAP) percentage growth includes a 2% to 3% currency tailwind based on the current rates and including the impact of hedged positions. – Unchanged

The company expects to generate free cash flow (non-GAAP) of approximately $10.5 billion through cash flow from operations of approximately $12.0 billion less capital expenditures of approximately $1.5 billion. This does not include any potential payments related to the ongoing tax litigation with the U.S. Internal Revenue Service. – Updated

Fourth Quarter 2021 Considerations – New

Comparable net revenues (non-GAAP) are expected to include an approximate even currency impact based on the current rates and including the impact of hedged positions.

Comparable EPS (non-GAAP) is expected to include an approximate 2% currency tailwind based on the current rates and including the impact of hedged positions.

The fourth quarter has six fewer days compared to fourth quarter 2020.

Full Year 2022 – New

The company is providing the following considerations for 2022:

- The company is confident in the underlying momentum in the business, supported by our transformation work, innovation agenda, and a more efficient and effective approach to marketing.

- The company expects elevated commodity inflation, and comparable cost of goods sold (non-GAAP) is expected to include a mid single-digit percentage commodity headwind based on the current rates and including the impact of hedged positions.

- Additionally, the company will continue to invest in the marketplace to support ongoing growth in organic revenues (non-GAAP).

-

The company is providing the initial currency outlook for full year 2022 as follows:

- Comparable net revenues (non-GAAP) are expected to include an approximate 2% to 3% currency headwind based on the current rates and including the impact of hedged positions.

- Comparable EPS (non-GAAP) is expected to include an approximate 2% to 3% currency headwind based on the current rates and including the impact of hedged positions.

The company will provide full year 2022 guidance when it reports fourth quarter earnings.

Notes |

- All references to growth rate percentages and share compare the results of the period to those of the prior year comparable period, unless otherwise noted.

- All references to volume and volume percentage changes indicate unit case volume, unless otherwise noted. All volume percentage changes are computed based on average daily sales, unless otherwise noted. “Unit case” means a unit of measurement equal to 192 U.S. fluid ounces of finished beverage (24 eight-ounce servings), with the exception of unit case equivalents for Costa non-ready-to-drink beverage products which are primarily measured in number of transactions. “Unit case volume” means the number of unit cases (or unit case equivalents) of company beverages directly or indirectly sold by the company and its bottling partners to customers or consumers.

- “Concentrate sales” represents the amount of concentrates, syrups, beverage bases, source waters and powders/minerals (in all instances expressed in equivalent unit cases) sold by, or used in finished beverages sold by, the company to its bottling partners or other customers. For Costa non-ready-to-drink beverage products, “concentrate sales” represents the amount of coffee (in all instances expressed in equivalent unit cases) sold by the company to customers or consumers. In the reconciliation of reported net revenues, “concentrate sales” represents the percent change in net revenues attributable to the increase (decrease) in concentrate sales volume for the geographic operating segments and the Global Ventures operating segment after considering the impact of structural changes, if any. For the Bottling Investments operating segment, this represents the percent change in net revenues attributable to the increase (decrease) in unit case volume computed based on total sales (rather than average daily sales) in each of the corresponding periods after considering the impact of structural changes, if any. The Bottling Investments operating segment reflects unit case volume growth for consolidated bottlers only.

- “Price/mix” represents the change in net operating revenues caused by factors such as price changes, the mix of products and packages sold, and the mix of channels and geographic territories where the sales occurred.

First quarter 2021 financial results were impacted by five additional days as compared to first quarter 2020, and fourth quarter 2021 financial results will be impacted by six fewer days as compared to fourth quarter 2020. Unit case volume results for the quarters are not impacted by the variances in days due to the average daily sales computation referenced above.

Conference Call |

The company is hosting a conference call with investors and analysts to discuss third quarter 2021 operating results today, Oct. 27, 2021, at 8:30 a.m. ET. The company invites participants to listen to a live webcast of the conference call on the company’s website, http://www.coca-colacompany.com, in the “Investors” section. An audio replay in downloadable digital format and a transcript of the call will be available on the website within 24 hours following the call. Further, the “Investors” section of the website includes certain supplemental information and a reconciliation of non-GAAP financial measures to the company’s results as reported under GAAP, which may be used during the call when discussing financial results.

Contacts

Investors and Analysts: Tim Leveridge, koinvestorrelations@coca-cola.com

Media: Scott Leith, sleith@coca-cola.com