")

SEOUL, South Korea--(BUSINESS WIRE)--Korea Zinc (KRX:010130) has released a statement today to debunk false allegations and misleading claims presented by MBK Partners during the press conference held on December 10.

MBK falsely alleged that Korea Zinc has spent at least KRW 1.2 trillion under Chairman Yun B. Choi’s tenure without proper board oversight, while also claiming that these investments caused a corporate value loss of KRW 3.4 trillion.

To support these claims, MBK arbitrarily applied unfamiliar terms such as “Lost EBITDA Opportunity,” “Lost Enterprise Value Opportunity” and “Lost Shareholder Value Opportunity,” which are neither standard in accounting practices nor widely recognized in financial analysis. By using speculative assumptions and unverified data, MBK has attempted to mislead shareholders, the market, and the media, significantly damaging Korea Zinc’s reputation.

MBK has claimed that if Korea Zinc had allocated KRW 582 billion used to invest in new businesses including the resource recycling business, KRW 569 billion used to invest in funds unrelated to core businesses, and KRW 900 billion used for a share buyback into other projects, it could have generated KRW 3.4 trillion in value.

However, this assertion clearly demonstrates MBK’s lack of long-term vision and understanding of the new businesses Korea Zinc is pursuing. This also highlights MBK’s inability to manage the company in an effective way. MBK’s interpretation of Korea Zinc’s financial investment activities and business investments reflect a misunderstanding and appears to rely on selective data presentation.

Notably, MBK has even included the cost of the share buyback Korea Zinc executed to fend off their predatory hostile M&A attempts, falsely claiming that it led to a loss in corporate value.

Lack of Understanding of Korea Zinc’s Resource Recycling Business and Absence of Long-term Corporate Vision

First and foremost, Pedalpoint Holdings, including Igneo Holdings, is central to the resource recycling business and has achieved significant progress by strengthening the value chain while pursuing new business opportunities for future growth. As of Q3 this year, the project’s cumulative sales rose significantly to KRW 1.1656 trillion, while net losses decreased to KRW 30.7 billion, showing simultaneous improvements in business expansion and profitability. In particular, Pedalpoint Holdings is expected to address challenges of securing raw material critical for producing Korea Zinc’s future flagship product – eco-friendly copper.

Specifically, Korea Zinc is planning to increase its annual copper production capacity from 34,000 tons to 150,000 tons by 2028. To achieve this, the company acquired the global scrap metal trading company Kataman Metals in April. And in September, it acquired the local robotics solution company ROBOne with the goal of deploying delta robots at US facilities to improve productivity.

The resource recycling market, particularly the copper sector, has significant growth potential. According to a recent report by the International Energy Agency (IEA) titled “Recycling of Critical Minerals,” global copper scrap volumes are expected to increase from 16 million tons in 2023 to 28 million tons by 2050, with scrap from EVs and storage batteries set to grow more than 35-fold between 2030 and 2050.

MBK’s evaluation of Pedalpoint Holdings and Korea Zinc’s resource recycling business focuses solely on short-term performance. It ignores the fact that the resource recycling business is a new business area, serving as a strategic future growth engine, and shows their lack of understanding of the business’ structure and long-term value. This reveals MBK’s fundamental incomprehension of Korea Zinc’s Troika Drive and further underscores MBK’s inability to drive the new business initiatives.

Moreover, Korea Zinc would like to stress that the decision to invest in Igneo Holdings followed a thorough evaluation and analysis conducted over the course of more than a year. This included assessing the company’s value, securing equity ratios, determining investment allocations and reviewing board structures. Comprehensive due diligence was conducted with various global consulting firms on financial, legal and environmental aspects. Investment advisory was handled by a global investment consultancy, which conducted coordination and valuation reviews. Korea Zinc’s technical team also performed technology assessments.

These procedures were reported to management and reviewed by the board before final approval. Even Young Poong’s advisor Jang Hyung-Jin agreed to the transaction on two occasions. Despite this, MBK is now making baseless allegations about this matter.

MBK’s Distortion of the Nature of Financial Investments

MBK has also misrepresented the nature of financial investments such as fund investments. Some of these funds were liquidated early, and the capital has since been successfully recovered. Other funds have even generated profits.

Nonetheless, MBK has falsely claimed that these fund investments resulted in complete losses. They have made a speculative argument, stating that redirecting the funds to business investments would have prevented damaging corporate value, a claim that lacks any credible basis.

MBK’s Misguided Assertions Regarding Share Buyback Costs

MBK has also criticized Korea Zinc for purchasing treasury shares through a share buyback program, which was initiated to address MBK’s hostile takeover attempt. Their claim that this action has negatively impacted Korea Zinc’s corporate value lacks substantiation and raises questions about assigning responsibility.

Industry experts unanimously agree that Korea Zinc wouldn’t have incurred share buyback costs if not for MBK’s hostile M&A attempt. If this capital had been used for new business investments, it could have generated billions in enhancing corporate value. Moreover, MBK’s actions have increased Korea Zinc’s debt and weakened its investment capacity, significantly harming the company’s value.

A recent employee survey also revealed that a huge number of Korea Zinc employees have been experiencing immense stress due to MBK’s hostile M&A attempt. This has disrupted daily operations and inflicted serious damage on Korea Zinc’s corporate competitiveness and human resources.

Overlooking the Partner Young Poong’s Low Corporate Value and Weak Governance

MBK has turned a blind eye to the severe corporate value erosion at Young Poong, their partner in this hostile M&A against Korea Zinc.

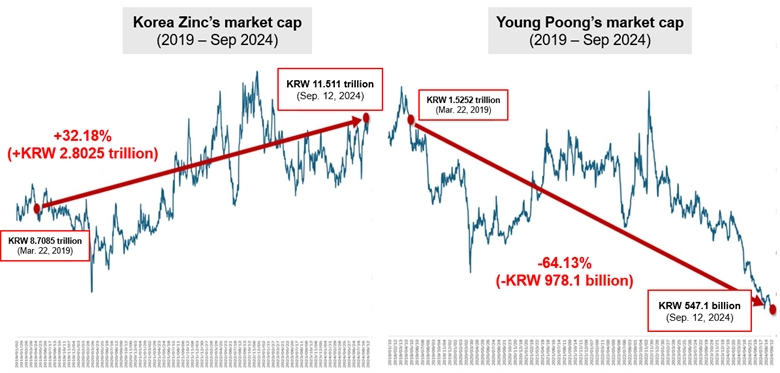

For listed companies like Korea Zinc, corporate value is generally measured through market capitalization. From March 22, 2019, to September 12, 2024, Korea Zinc’s market cap grew from KRW 8.7085 trillion to KRW 11.511 trillion, a 32.2% increase. In contrast, Young Poong’s market cap fell from KRW 1.5252 trillion to KRW 547.1 billion, a 64.1% decline.

A Korea Zinc representative stated, “MBK is disparaging Korea Zinc, which has risen to become a global leader in non-ferrous metals with support from employees, shareholders and local communities, by distorting statistics and making baseless claims. Moreover, through their hostile M&A attempt, MBK is actively damaging Korea Zinc’s corporate value.”

They added, “In line with the long-term vision and plans emphasized at last December’s Investor Day, Korea Zinc will steadily pursue its goals to achieve KRW 25 trillion in sales by 2033. This includes advancing the renewable energy, secondary battery materials and resource recycling businesses.”