NEEDHAM, Mass.--(BUSINESS WIRE)--Immersion Investments, LLC and its affiliates – a top 20 shareholder of Potbelly Corporation (PBPB), parent company of the quick service restaurant chain – today issued an open letter to Potbelly’s Board of Directors and its management team urging immediate action to maximize value for shareholders.

A full copy of the letter is below:

Dear Members of Management and the Board of Directors,

Immersion Investments, LLC, together with its affiliates (collectively, "we" or "Immersion"), holds 299,906 shares of Potbelly Corporation (PBPB) ("Potbelly" or the "Company") common stock, making us one of the company’s largest shareholders.

We believe Potbelly is an underappreciated growth story. The market continues to value the stock at a meaningful discount to peers despite readily obvious improvements to the existing business and growth profile. The status quo is unacceptable. As written by Rita Mae Brown, “The definition of insanity is doing the same thing over and over and expecting different results.” We urge you to act with haste to realize value for all shareholders.

We have been impressed by management’s stewardship of the business since Bob Wright’s appointment as Chief Executive Officer in July 2020. Management has navigated the company to a solid financial footing during a period of high inflation and higher interest rates. Shop-level revenue and margins have exceeded pre-COVID levels, and the company has a significant pipeline of franchise commitments.1

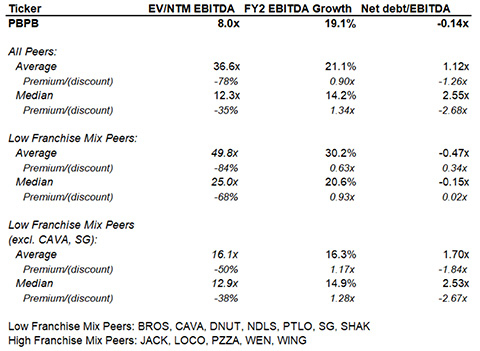

Today, Potbelly is a leading sandwich QSR concept, with best-in-class unit economics and a strong growth trajectory.2 Nonetheless, the share price has not kept pace with the improvements in the business. The median valuation multiple for Potbelly’s publicly traded peers (based on enterprise value relative to next twelve month adjusted earnings before interest, taxes, depreciation, and amortization – EV/NTM EBITDA) is greater than 12x, while Potbelly is priced at 8x next-twelve-month EBITDA estimates.3 Potbelly is an unlevered growth company, yet it’s current valuation is more reflective of a slow growth, highly levered mature company.

At the end of the second quarter on June 30th, you cited 234 committed franchise locations.4 At $1.2 million in sales per location and a 6% royalty rate, these 234 committed locations could generate nearly $17 million in extremely high margin franchise revenue. Assuming a 90% margin on this source of revenue, with minimal commensurate operating expenses, the current pipeline of locations could be contributing $15 million in additional EBITDA.5 This backlog of new locations represents a 60% increase in profitability, relative to analyst estimates calling for EBITDA of $28 million in 2024. If there is no improvement in the base operations ($28 million EBITDA) and layer on the $15 million in contribution from the franchise locations, Potbelly is priced at less than 6x EBITDA. This exercise implies no growth in the number of franchise commitments or improvements in current operations, both of which we believe to have a high likelihood of occurring. Because the company’s forward-looking growth is franchise-led, which requires significantly less capital than a company-owned unit growth strategy, the current valuation (8x on current EBITDA and <6x future EBITDA) is simply too cheap.

Given the company’s market capitalization and liquidity, we do not believe this is a “let the results speak for themselves” situation. Several years ago, the business was barely profitable, burning cash and had zero visible growth prospects. Today, we are profitable, generating cash, and have a franchise pipeline capable of delivering low-to-mid teens EBITDA growth for the next several years, yet the stock has been range-bound for nearly four years.

It is time for action and the board needs to be aggressive in pursuing alternatives for value creation, including one or more of the following:

-

Undergo a strategic review process to evaluate a sale of the entire business. There is ample private and strategic interest in growing restaurant businesses, especially ones exhibiting franchise-led growth. Given the unlevered balance sheet, we believe there is significant interest from private equity. Additionally, a sale would allow the company to easily refranchise the existing store base, which creates substantial noise in reported financial results and is generally more difficult to execute and properly communicate as a publicly traded business.

-

Aggressively repurchase shares. Despite the new share repurchase authorization put in place in May of this year, we are disappointed that more shares have not yet been repurchased given the clear undervaluation and continued open market purchases by members of management. In the quarter ending June 30th, management repurchased just 86,000 shares for $700,000.6 At this pace, it will take more than seven years to exhaust the current buyback authorization.

An active buyback at the current valuation will not just provide value to shareholders but will also provide a backstop to the volatility of what many consider an illiquid, “microcap” security. A 2021 study done by Craig Lewish and Joshua White provided evidence that, “Greater investment in stock buybacks equates to larger improvements in liquidity...this liquidity reduces transaction costs for all investors and helps facilitate orderly markets,” and “Stock buybacks are associated with significant reductions in both realized and anticipated stock return volatility.” 7

- Slow internal investments in technology and headcount and look to reduce operating expenses. Recognizing the need to keep pace with the changing face of the customer, and despite tangible improvements in store economics and significant growth in the franchise location pipeline, the company has yet to significantly leverage its spending into meaningful reported EBITDA improvement. In the absence of acceleration in same store sales, management needs to show investors greater operating leverage and profitability. Continuing to spend money without a tangible and expedient ROI is unacceptable.

We look forward to seeing the board act.

Sincerely,

J. Timothy Delaney and David Polansky

Managing Partners

Immersion Investments LLC

About Immersion Investments:

Immersion Investments operates private partnerships with a concentrated, tax-sensitive and long-term focus designed to act independently of the broader market, focusing on small- and micro-cap equities.

1 Company filings

2 Franchise disclosure documents and publicly available information

Peers: Subway, Jersey Mike’s, Firehouse Subs, Jimmy John’s

3 Capital IQ

4 Company filings

5 Immersion Investments internal estimates

6 Company filings

7 Lewis, C. M., White, J. T., (2021). Corporate liquidity provision and share repurchase programs. US Chamber of Commerce: Center for Capital Markets Competitiveness