PUTEAUX, France--(BUSINESS WIRE)--Regulatory News:

emeis (Paris:EMEIS):

Improving the fundamentals of our core activities to support future performance

- The Group's transformation draws on its people, the quality of care it provides and the optimisation of its processes. These three focus areas are the levers of tomorrow's operational and financial performance. We are already seeing progress (satisfaction rate up to 92.4%, stabilisation of teams with staff turnover down -3 points and absenteeism down -1.4 points since 2022, a sharp -21% decrease in the frequency rate of work-related accidents with lost time in six months, etc.), and gradual effects on operating indicators.

- emeis has reaffirmed its ambition to become a mission-led company in 2025.

Growth in all core activities and in all geographical areas

- Solid growth of +9.2%, including +8.9% on an organic basis, reflecting the initial payoffs from the measures taken in the last 18 months.

- The occupancy rate is up in all geographical areas and all core activities (by +2.6 points on average).

- Positive price effect also observed across all the Group's markets (of +5.5% on average).

- The solid level of business since the start of the second half of the year confirms this favourable trend.

EBITDAR stable due to stimulus measures in France

- Discrepancy between the immediate effects of stimulus measures on expenses and the more gradual effects on revenue.

- Residual impacts of the recent inflationary episode.

A gradually recovering balance sheet

- Net debt down to €4,425 million at end-June 2024, i.e., down -€217 million over six months and down almost €4.8 billion over 12 months.

- Financial expenses down -24%, reflecting the positive impact of the financial restructuring.

- Progress on the property disposal programme: €452 million since mid-2022, including €159 million since January.

- Free cash flow improved by +€111 million, reflecting some of the effects of the precautionary measures taken in recent months, but remained negative at -€178 million.

Confirmation of EBITDAR target and acceleration of expected disposals

- emeis confirms the outlook announced on 26 July when it published its first-half revenue figures.

- 2024 EBITDAR is expected to increase by 0% to +5%, i.e., between €700 million and €730 million.

- Stepped up ambitions for disposals of real estate and operating assets to reach €1.5 billion between mid-2022 and the end of 2025 with the aim of continuing to reduce the Group’s debt.

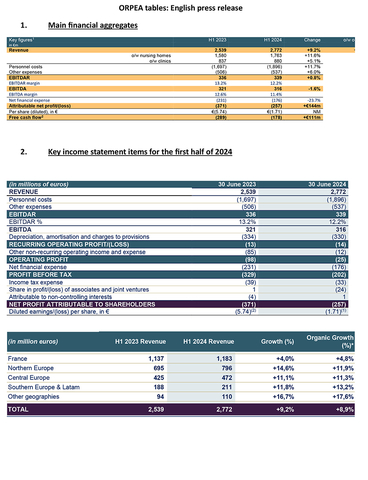

Key figures1 |

H1 2023 |

H1 2024 |

Change |

o/w organic |

in €m |

||||

Revenue |

2,539 |

2,772 |

+9.2% |

+8.9% |

o/w nursing homes |

1,580 |

1,763 |

+11.6% |

|

o/w clinics |

837 |

880 |

+5.1% |

|

Personnel costs |

(1,697) |

(1,896) |

+11.7% |

|

Other expenses |

(506) |

(537) |

+6.0% |

|

EBITDAR |

336 |

339 |

+0.8% |

|

EBITDAR margin |

13.2% |

12.2% |

||

EBITDA |

321 |

316 |

-1.6% |

|

EBITDA margin |

12.6% |

11.4% |

|

|

Net financial expense |

(231) |

(176) |

-23.7% |

|

Attributable net profit/(loss) |

(371) |

(257) |

+€144m |

|

Per share (diluted), in € |

€(5.74) |

€(1.71) |

NM |

|

Free cash flow2 |

(289) |

(178) |

+€111m |

Laurent Guillot, Chief Executive Officer, said: “The performance delivered by emeis in the first half of 2024 attests to good momentum in all our activities and geographical areas. Our non-financial indicators, particularly those relating to the occupational safety of our teams and quality of care, continue to improve, demonstrating that the transformation initiated in 2022 is now bearing fruit: the number of workplace accidents has been halved compared with 2021, staff turnover is down, and satisfaction indicators for our patients, residents and their loved ones are also improving significantly. These fundamentals provide a solid foundation for the recovery that is now underway.

In the first half of the year, revenue rose by almost 9%, which is above comparable figures for the sector. This performance was driven by a 2.6-point improvement in the average occupancy rate and a 5.5% positive price effect across all our activities and geographical areas. Although we must remain vigilant and cautious, this upward trend has been evident since the start of the third quarter, proof of the favourable operating momentum that is taking shape.

The stability of the Group's EBITDAR over the first half of 2024 reflects our investment in the emeis teams in necessary response to the recent gradual increase in occupancy rates. In the short term, however, the effort made by emeis in France is being offset by all the other geographies where EBITDAR margins are on the rise.

We now need to extend and accelerate today’s recovery momentum, and build on our Group’s sustainable strengths for the years to come. To do this, we are capitalizing on a more robust balance sheet, while preparing to transform emeis into a mission-led company next year, based on our mission statement: 'Together, let’s stand as a strength for the vulnerable among us'.”

About emeis

With nearly 78,000 experts and professionals in healthcare, care, and supporting the most vulnerable among us, emeis operates in around 20 countries with five core activities: psychiatric hospitals, post-acute and rehabilitation hospitals, nursing homes, home care services, and assisted-living facilities.

Every year, emeis welcomes 283,000 residents, patients, and other beneficiaries. emeis is committed and is taking action to rise to a major challenge facing our society, i.e., the increase in the number of people placed in vulnerable positions as a result of accidents or old age, and the rising number of cases of mental illness.

emeis is 50.2% owned by Caisse des Dépôts, CNP Assurances, MAIF, and MACSF Épargne Retraite. It is listed on the Euronext Paris stock exchange (ISIN: FR001400NLM4) and is a member of the SBF 120 and CAC Mid 60 indices.

Website: www.emeis.com/en

A renewed framework and solid fundamentals

Supported by renewed governance and a strengthened Management team, emeis, embodying the new identity unveiled during the first half of the year to accelerate transformation and shape a sustainable and profitable business model, is laying solid foundations for its medium-term development.

Thanks to our many strengths enhanced by the refoundation plan, the commitment of our teams around a recognised medical project and a new corporate plan hinging on a mission statement endorsed by the shareholders, "Together, let’s stand as a strength for the vulnerable among us", the Group is already seeing the first non-financial effects of the upward trend in the Group's financial indicators (satisfaction rate up +2.3 points versus 2022 to 92.4%, a -3-point reduction in staff turnover versus 2022, a -21% reduction in workplace accidents in a six-month period).

Increase in revenue (+9%): improved occupancy rate and favourable price effect

In the first half of 2024, the emeis Group's consolidated revenue rose significantly, with growth of +8.9% on an organic basis, and +9.2% based on the current scope of consolidation.

The improvement reflects the increase in occupancy rates and favourable price increases across all the Group's core activities and geographical areas.

Overall, the Group's average occupancy rate rose by +2.6 points to 85.3%, lifted by a marked upturn in Northern Europe (+4.2 points) and Southern Europe and Latin America (+4.5 points), which is an encouraging sign for the Group's future prospects.

This recovery trend is backed up by the initial business indicators observed since the start of the second half of the year, with the rise in occupancy rates seen in June still continuing, particularly in the French market.

EBITDAR margin remains temporarily under pressure

EBITDAR came to €339 million for the period, up +0.8% on first-half 2023, representing a margin of 12.2%.

Operating profitability continued to be temporarily affected by necessary measures implemented to gradually normalise the Group's occupancy rates, with the aim of improving quality of care and support. These measures have an immediate impact on personnel costs and a gradual effect on revenue. The corresponding time lag is temporarily weighing on EBITDAR margins.

For other operating expenses, the recent inflationary episode also impacted the Group's margin, while the occupancy rate in nursing homes in France remained below its normal level.

1- Key income statement items for the first half of 2024

In publishing its 2024 half-year results, the Group refers to financial indicators taken from its consolidated financial statements, as well as to alternative performance measures, which are presented in detail in the appendices to this press release. Definitions and calculation methods for these indicators are presented in the appendices to this press release.

(in millions of euros) |

30 June 2023 |

30 June 2024 |

REVENUE |

2,539 |

2,772 |

Personnel costs |

(1,697) |

(1,896) |

Other expenses |

(506) |

(537) |

EBITDAR |

336 |

339 |

EBITDAR % |

13.2% |

12.2% |

EBITDA |

321 |

316 |

Depreciation, amortisation and charges to provisions |

(334) |

(330) |

RECURRING OPERATING PROFIT/(LOSS) |

(13) |

(14) |

Other non-recurring operating income and expense |

(85) |

(12) |

OPERATING PROFIT |

(98) |

(25) |

Net financial expense |

(231) |

(176) |

PROFIT BEFORE TAX |

(329) |

(202) |

Income tax expense |

(39) |

(33) |

Share in profit/(loss) of associates and joint ventures |

1 |

(24) |

Attributable to non-controlling interests |

(4) |

1 |

NET PROFIT ATTRIBUTABLE TO SHAREHOLDERS |

(371) |

(257) |

Diluted earnings/(loss) per share, in € |

(5.74)(2) |

(1.71)(1) |

(1) The first-half 2024 figures have been restated to take account of the impact of the reverse stock split in March 2024, in accordance with IAS 23.

|

||

Revenue for the entire first half of 2024 came to €2,772 million, a +9.2% increase on first-half 2023 including +8.9% organic growth.

Revenue grew sharply in the first half of 2024, driven by positive price and care allowance effects (for +5.5% on average at Group level) and by a marked recovery in occupancy rates, internationally in particular, and the opening of new facilities. The rise in occupancy rates and the favourable contribution of price increases was observed across all geographical areas and all core activities.

Revenue for nursing homes was up +11.6% to €1,763 million. For clinics, it increased by +5.1% to €880 million.

The average occupancy rate rose by +2.6 points between the two periods, to 85.3% for the first half of 2024.

- The rise in the occupancy rate was driven in particular by Southern Europe and Latam (Spain, Italy, Portugal and Latin America) and Northern Europe (Germany, Netherlands, Belgium and Luxembourg).

- In France, the occupancy rate was slightly up on first-half 2023, at 85.8%, with a level above 92% for clinics and a slight increase for nursing homes (83.1% on average over the first half of 2024, i.e., up +0.1 point) which began mainly at the end of the period.

The occupancy rate for nursing homes rose by +3 points to 84.5%, and was up +0.9 points for clinics to 88%.

EBITDAR came to €339 million in the first half of 2024, up +0.8%, reflecting a margin of 12.2%. As the increase in EBITDAR from operations outside France (+€51 million) was accompanied by a reduction of the same order of magnitude in EBITDAR from operations in France, EBITDAR remained stable overall between the first half of 2023 and the first half of 2024.

The stable EBITDAR performance, despite an increase in revenue, mainly reflects a time lag between the immediate effect on expenses of operational recovery measures and their more gradual impact on revenue.

Personnel costs thus rose by +11.7% in the first half, reflecting the Group's commitment to continue improving the quality of its services and reduce staff turnover. The increase in personnel costs reflects salary increases and growth in the workforce over the period. Other operating expenses for our facilities (catering, care, energy, etc.) rose by +6.0%, mainly due to the residual effects of inflation.

EBITDA amounted to €316 million, representing a margin of 11.4%. Pre-IFRS 16 EBITDA amounted to €92 million, giving a margin of 3.3%, down -0.7 point on the same period last year.

Net financial expense fell by -24% to -€176 million, mainly reflecting the positive impact of the financial restructuring carried out over the last 12 months.

Non-recurring expenses were also down significantly in the six months ended 30 June 2024 compared with the first half of 2023, representing -€12 million for the period compared with -€85 million a year ago. The decrease mainly reflects the reduction in fees in connection with the restructuring achieved in 2023.

As a result, emeis again reported an attributable net loss for the first half, in an amount of -€257 million, but with a €114 million improvement compared with the first half of 2023. On a fully diluted basis, the loss per share came out at -€1.71 versus -€5.74 in first-half 2023.

2- Estimated value of the real estate portfolio

The estimated value of the real estate portfolio was €6.3 billion, compared with €6.5 billion at the end of 2022, based on the current scope of consolidation. At end-2023, independent valuers3 appraised a total of 414 facilities located mainly in France, representing assets worth €5.3 billion.

The portfolio is appraised at the end of each financial year. At the end of December 2023, the average yield on appraised assets was approximately 6% (excluding duties).

Since the end of 2021, the value of the portfolio has been adjusted downwards by -21% on a comparable scope basis, reflecting the impact of the rise in interest rates over the period, and the corresponding increase in real estate investors' yield requirements.

3- Cash flow for the first half of 2024

Net free cash flow before financing was -€178 million, an improvement of +€111 million compared with the first half of 2023, reflecting the combination of the following factors:

-

The significant reduction in development capex (mainly real estate), which came to -€91 million (versus

-€192 million in the first half of 2023). The -€102 million decrease compared with the first half of 2023 reflects the implementation during the period of precautionary measures as part of a project review (postponements, adjustments and cancellations) in order to preserve the Group's liquidity and focus development on the most favourable transactions. - €143 million in proceeds from real estate disposals in the first half (mainly in the Netherlands, Portugal and Ireland). The latest disposals bring the total proceeds from real estate disposals received since mid-2022 to €451 million. Disposals in the coming six‑month periods may also include operating assets.

- The cost of debt in the cash flow statement rose by +€59 million to €119 million, returning to a normal level of outflows, even though a portion of borrowing costs was frozen until the first half of 2023 during the restructuring process.

- -€99 million in non-recurring items, including expenses related to the management of the crisis experienced by the Group. The vast majority of these items relate to 2023 expenses paid in the first half of 2024 and therefore correspond to outflows in respect of expenses for which provisions have already been made.

There was also a €390 million cash contribution, corresponding to the final capital increase planned as part of the Group's financial restructuring, carried out in February 2024. The equivalent of 29.3 million new shares (post reverse stock split) were created on this occasion.

As a result, the Group's net debt4 stood at €4,425 million, down -€217 million versus 31 December 2023 (€4,642 million).

4- Main consolidated balance sheet, debt and liquidity indicators

Net debt (excluding IFRS 16 lease liabilities) at 30 June 2024 stood at €4,425 million, compared with €4,642 million at end-2023. The reduction in net debt over six months is mainly due to the third capital increase (€390 million), provided under the financial restructuring plan (completed on 15 February 2024), while the Group's free cash flow, although still negative, improved by a significant €111 million compared with the first half of 2023.

As a reminder, the Group's net debt at the end of 2022 was €8.8 billion.

59% of gross debt at end-June 2024 corresponded to secured debt with the Group's main banking partners (G6), maturing mainly in October 2027. In addition, mortgage, leasing debt and other secured debt accounts for 34% of the total.

Cash and cash equivalents at the end of June 2024 amounted to €653 million, broadly comparable to the level reported at the end of 2023, and €1,053 million including a €400 million “new money” additional credit facility, which was undrawn at that date. On 1 October 2024, drawdown requests were made on this facility in accordance with the applicable documentation. The funds are expected to be made available by the lenders on 7 October 2024. The schedule of lease maturities, published in the appendix to this press release, shows €456 million maturing in the second half of 2024.

In the first half, the average cost of gross debt was 5.44%5, up from 4.71% in the first half of 2023. The increase in the average cost of debt is mainly due to the fact that the debt was converted into capital, with a lower margin than the Group average.

5- Cumulative disposals: €452 million since mid-2022, and €1.5 billion expected by the end of 2025

emeis continued to carry out a large volume of real estate disposals in an albeit tight investment market in which investors are still taking a wait-and-see approach. The drop in interest rates following the easing of monetary policy could nevertheless contribute to a gradual recovery in investment volumes.

emeis has managed to complete almost €452 million in property disposals6 since mid-2022, including €159 million in the first half. In addition, at the end of June, €106 million in further disposals were still subject to binding offers which will be finalised over the next 18 months.

In total, the volume invested by the Group since 2022 represents almost 30% of the Continental European healthcare real estate investment market, which underlines not only the Group's expertise in this area, but also the quality of its portfolio.

In order to continue reducing its debt and fulfil its bank covenants7, the emeis Group will be accelerating its disposals, and now aims to dispose of €1.5 billion in real estate8 and operational9 assets between June 2022 and December 2025.

6- 2024 outlook reaffirmed

The trends observed since the start of the second half, particularly regarding the occupancy rate of the Group's residences, confirm that the Group's operating markets are engaged in a recovery which, although more gradual than expected in France, is on an encouraging trajectory in all markets.

The Group is therefore reaffirming the outlook it issued at the end of July 2024, anticipating EBITDAR for 2024 of between €700 million and €730 million. This outlook was communicated on 26 July in the half-year revenue press release, taking into account a more gradual than expected operational recovery in France. On this basis, pre-IFRS 16 2024 EBITDA would come to around €210 million in 2024.

APPENDICES

A web conference is scheduled to be held by Laurent Guillot (Chief Executive Officer) and Jean-Marc Boursier (Chief Financial Officer) at 10:00 a.m. (CEST) on 4 October. The conference will be accompanied by a presentation and a recording of the web conference will be made available on the Company's website.

2024 HALF-YEAR CONSOLIDATED FINANCIAL STATEMENTS

emeis S.A. publishes its consolidated results for the six months ended 30 June 2024, which were approved by the Board of Directors on 3 October 2024. 10

DEFINITIONS

Organic growth |

The organic growth of the Group's revenue includes:

3. Revenue generated in the current period by facilities created during the current period or year-earlier period, and the change in revenue of recently acquired facilities by comparison with the previous equivalent period. |

EBITDAR |

Recurring operating profit before depreciation, amortisation and charges to provisions and before rental expenses. |

EBITDA |

EBITDAR net of rental expenses on leases of less than one year. |

EBITDA pre-IFRS 16 |

EBITDAR excluding rental expenses on leases of less than one year and excluding lease payments related to leases of more than one year falling within the scope of IFRS 16. |

Net debt |

Long-term debt + short-term debt - cash and marketable securities (excluding IFRS 16 lease liabilities). |

Net recurring operating cash flow |

Cash generated by ordinary activities, net of recurring maintenance and IT capital expenditure. Net recurring operating cash flow is the sum of pre-IFRS 16 EBITDA, recurring non-cash items, change in working capital, income tax paid and maintenance and IT capital expenditure. |

Net cash flow before financing |

Net cash after recurring and non-recurring items, all capital expenditure, interest expense on borrowings, and gains and losses on transactions concerning the asset portfolio. Net cash flow before financing is the sum of net recurring operating cash flow, development capital expenditure, non-recurring items, net income or expense related to the day-to-day management of the asset portfolio and financial expenses. |

_______________________________________

1 Pre-IFRS-16 key figures are provided in Appendix 1 of this press release, page 10.

2 Net cash flow before financing (see Appendix 3).

3 JLL, C&W and CBRE.

4 Excl IFRS 16 debt

5 before hedging instruments

6 Mainly sale and leaseback transactions.

7 Available liquidity in excess of €300 million, tested quarterly, and net debt/EBITDA ratio below 9x, tested half-yearly from June 2025 on €203m outstanding debt.

8 Amount expressed in net selling value before repayment of associated debt.

9 Amount expressed in equity value.

10 The half-year financial statements have been reviewed by the Statutory Auditors, whose corresponding report is currently being prepared for issue.

11 The first-half 2024 figures have been restated to take into account the impact of the reverse stock split in March 2024, in accordance with IAS 33.