")

")

")

")

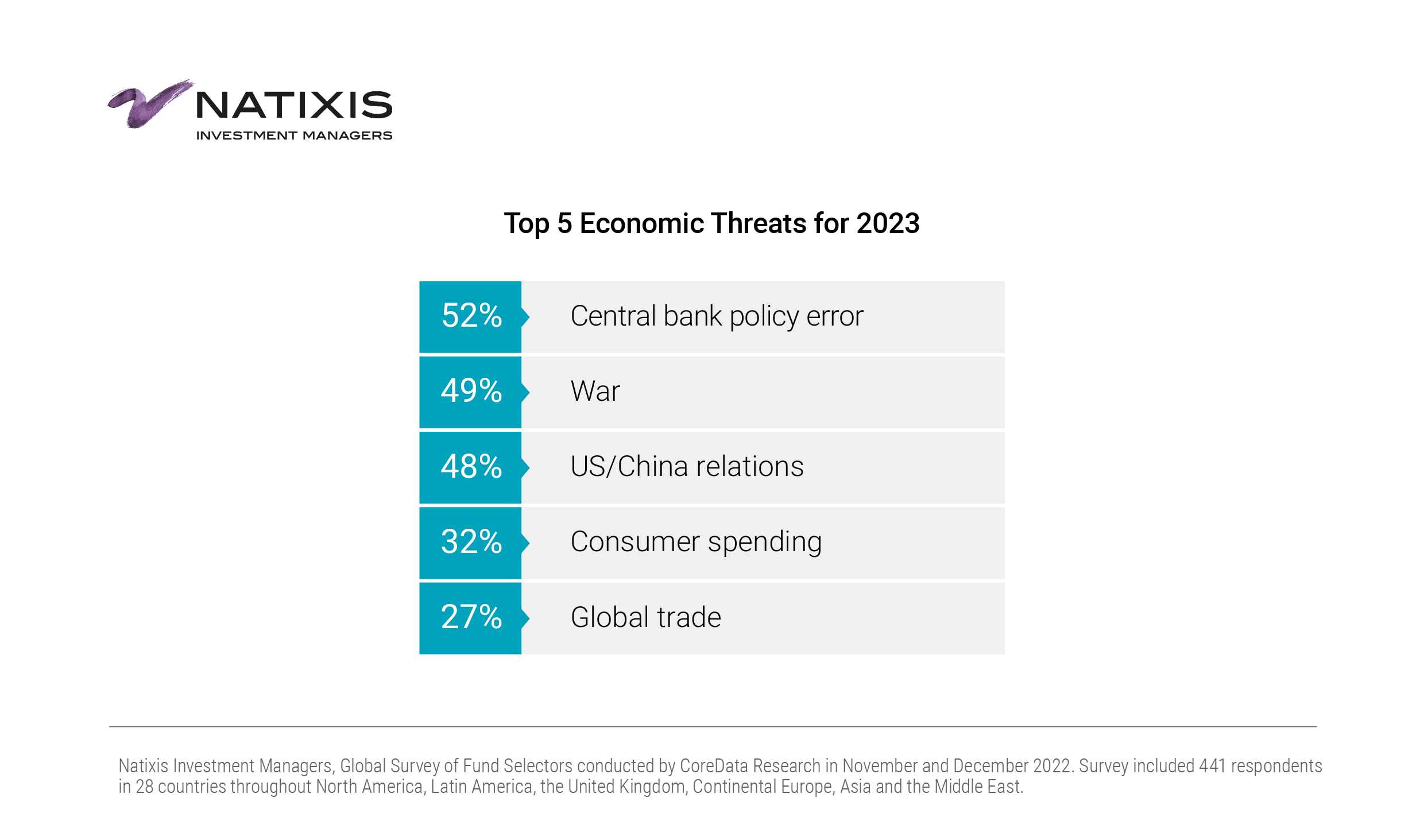

BOSTON--(BUSINESS WIRE)--Eight out of ten (84%) top investment professionals believe the US economy already is in or will be in a recession this year, and 51% think the markets are underestimating how long it will last, according to survey findings published today by Natixis Investment Managers (Natixis IM). They see a policy error by the Federal Reserve as the biggest potential threat to the US economy. Yet their outlook for the markets is surprisingly optimistic, with a mostly bullish forecast for stocks (63%) and bonds (54%) in a year when actively managed investments are expected to shine.

Natixis IM surveyed 152 US investment professionals who are responsible for their firms’ top-of-the-house selection of funds and other investment products into which $17.5 trillion client assets are invested among private banks, wirehouses, registered investment advisors, independent wealth managers and other advisory firms. The US findings are part of a larger global survey of 441 professional fund selectors conducted in December 2022.

The survey found:

- 70% of respondents are either maintaining (43%) their average 8% return assumptions for client portfolios this year or plan to adjust return assumptions even higher (27%).

- 51% expect interest rates to continue rising, while another 28% think the Fed will take a pause. Just 21% think rates will start to come down this year.

- Given the rippling effect of rates on the markets, 84% predict the stock market will be equally (37%) or even more volatile (47%) than last year.

- 56% say valuations still don’t reflect company fundamentals, even after repricing that led to nearly a 20% decline in the S&P 500 Index last year.

- 53% think the recession will expose the inadequacies of passive investing, which 51% believe has distorted relative stock prices and risk-return trade-offs, and 63% say contributes to bigger market swings when there are large flows into and out of passive investments.

“Investment performance is once again a differentiator,” said Dave Goodsell, head of the Natixis Center for Investor Research. “Ten-plus years of historically low rates accommodated a long bull market run that sent stock prices soaring and made almost any investor look like a genius. Simple, low-cost, passively-managed index funds generated big returns from high-flying, large-cap growth stocks. Last year’s steep losses was a hard lesson for millions of Americans who discovered the hidden dangers of relying too much on passive investing.”

The survey findings show that fund selectors now envision more of a stock-pickers market, in which active investments outperform (68%) and prove essential for generating alpha (80%). Most (82%) expect a wider spread, or dispersion, between the best and worst performing returns on individual securities in an index versus all of them moving in lockstep as they have. This creates greater opportunity for active managers to capture the upside of market dislocations and mis-priced or undervalued securities.

Shoring up client portfolios

Fund selectors are recommending small but significant allocation shifts to shore up client portfolios. Their top portfolio risk concerns are inflation (71%), interest rates (62%) and volatility (47%). Most (67%) agree that the market environment will require frequent rebalancing.

Most (73%) expect rising rates to usher in a resurgence in traditional fixed income, which is welcome news since 60% think investors have taken on too much risk chasing yields elsewhere. They are increasing allocations to bonds of all types, mostly government bonds (44%) and investment-grade corporate bonds (43%) while keeping an eye on rate moves. Most want to see 10-Year Treasury yields above 4.5%, including 20% who are looking for yields greater than 5%, before lengthening durations. For now, 69% are recommending measures such as short-term bond ETFs, to counter duration risk.

Sixty percent say they continue to recommend allocations to alternatives because of increased market risks. Within alternatives, fund selectors are mostly adding infrastructure investments (44%) private equity (44%) and private debt (39%). They also recommend increasing allocations to absolute return strategies (38%) and greater use of options-based overlays, such as hedged equity (34%). Half (52%) say they are holding onto their existing real estate investments, and 32% plan to add more, suggesting that despite challenges facing the real estate sector, it adds value as an inflation hedge.

Fund selectors remain bullish on stocks, with 48% increasing allocations to US equities this year. They think the energy, financial and healthcare sectors are most likely to outperform, and that the tech sector will stabilize, with more predicting information technology to outperform (40%) than underperform (31%) the market this year. Outside the US equities market, fund selectors also plan to increase allocations to emerging market (46%), European (29%) and Asia-Pacific (24%) equities.

Geopolitical tensions are a game-changer with all eyes on the US and China

From an investment perspective, fund selectors are mostly concerned with what the US Federal Bank does. Beyond that and on a whole other level, they see war and relations between the US and China as the biggest threats to the economy, a concern that factors into their market outlook and portfolio strategies.

The survey of US fund selectors and larger global survey found:

- 64% of fund selectors in the US and 69% globally, including 70% in Asia, think the global economy is moving toward two separate spheres of economic activity.

- While 84% overall believe the US dollar will maintain its position as the world’s dominant currency, 60% in the US and 63% globally think the dollar will lose strength this year. Those in Asia (74%) are most likely to forecast a weakening dollar.

- 55% in the US and 62% globally agree that economic growth will slow as supply chains shift to more domestic production and “friend-shoring.” Those in Asia are most likely to agree (77%).

Fine-tuning the investment offering

Fund managers are fine-tuning the product offering on their firm’s platform to address heightened market risks and provide advisors with a wider range of investment strategies to meet clients’ needs.

More than half (56%) are increasing the number of actively managed funds on their platform. On average, 60% of the funds they offer now are actively managed. They also are adding private assets (50%), sustainable investment options (47%), hedge funds (34%) and thematic investments (34%) to capitalize on innovation opportunities and demographic trends.

Notably, fund selectors are enhancing their model portfolio offerings, mostly because model portfolios help to streamline the investment management process (87%), enable advisors to spend more time addressing clients needs (82%), and help to ensure a consistent investment experience for clients (77%) while managing risk exposure for the firm (77%). They agree that heightened market volatility is accelerating advisors’ use of model portfolios (65%) and that models enhance the alpha potential for their clients (64%).

The survey also found:

- 58% of fund selectors are finding greater need for specialty models to complement the core models advisors use as a base for building client portfolios.

- The types of specialty models they are adding include models with enhanced customization tailored or high net worth clients (46%) and models with a focus on alternatives (43%), income generation (44%), tax management (40%); sustainability (34%), sustainability (34%) and thematics (26%).

- 51% are increasing the number of model portfolios built and managed by third-party asset managers this year, giving priority to asset managers best at active risk management (50%), and tactical asset allocation (40%).

A full copy of the global report on the 2023 Natixis Investment Managers Pro Fund Selector Survey can be found at https://www.im.natixis.com/us/research/2023-fund-selector

The views and opinions expressed may change based on market and other conditions. This material is provided for informational purposes only and should not be construed as investment advice. There can be no assurance that developments will transpire as forecasted. Actual results may vary.

All investing involves risk, including the risk of loss. No investment strategy or risk management technique can guarantee return or eliminate risk in all market environments.

Methodology

Natixis Investment Managers’s Global Survey of Fund Selectors was conducted by CoreData Research and completed in December 2022. The global survey included 441 respondents throughout North America, Latin America, the United Kingdom, Continental Europe, Asia and the Middle East and who collectively are responsible for $30 trillion in client assets under management.

About Natixis Investment Managers

Natixis Investment Managers’ multi-affiliate approach connects clients to the independent thinking and focused expertise of more than 20 active managers. Ranked among the world’s largest asset managers1 with more than $1 trillion assets under management2 (€1 trillion), Natixis Investment Managers delivers a diverse range of solutions across asset classes, styles, and vehicles, including innovative environmental, social, and governance (ESG) strategies and products dedicated to advancing sustainable finance. The firm partners with clients in order to understand their unique needs and provide insights and investment solutions tailored to their long-term goals.

Headquartered in Paris and Boston, Natixis Investment Managers is part of the Global Financial Services division of Groupe BPCE, the second-largest banking group in France through the Banque Populaire and Caisse d’Epargne retail networks. Natixis Investment Managers’ affiliated investment management firms include AEW; AlphaSimplex Group; DNCA Investments;3 Dorval Asset Management; Flexstone Partners; Gateway Investment Advisers; Harris Associates; Investors Mutual Limited; Loomis, Sayles & Company; Mirova; MV Credit; Naxicap Partners; Ossiam; Ostrum Asset Management; Seventure Partners; Thematics Asset Management; Vauban Infrastructure Partners; Vaughan Nelson Investment Management; and WCM Investment Management. Additionally, investment solutions are offered through Natixis Investment Managers Solutions and Natixis Advisors, LLC. Not all offerings are available in all jurisdictions. For additional information, please visit Natixis Investment Managers’ website at im.natixis.com | LinkedIn: linkedin.com/company/natixis-investment-managers.

Natixis Investment Managers’ distribution and service groups include Natixis Distribution, LLC, a limited purpose broker-dealer and the distributor of various U.S. registered investment companies for which advisory services are provided by affiliated firms of Natixis Investment Managers, Natixis Investment Managers S.A. (Luxembourg), Natixis Investment Managers International (France), and their affiliated distribution and service entities in Europe and Asia.

1 Cerulli Quantitative Update: Global Markets 2022 ranked Natixis Investment Managers as the 18th largest asset manager in the world based on assets under management as of December 31, 2021. |

2 Assets under management (“AUM”) of current affiliated entities measured as of September 30, 2022 are $1,072.9 billion (€1,095.4 billion). AUM, as reported, may include notional assets, assets serviced, gross assets, assets of minority-owned affiliated entities and other types of non-regulatory AUM |

5461861.1.1