")

BOSTON--(BUSINESS WIRE)--What’s the level of anxiety among American retirement savers as a result of increasing interest rates, rising inflation and the ongoing impact of the pandemic? Understandably high. In fact, according to recent Fidelity Investments® research2, more than half of American workers indicate they are “extremely or very concerned” about the health and stability of the economy—and as a result, nearly 1 in 5 (19%) say they have adjusted their retirement strategy and are taking a more conservative approach to their retirement savings.

And the reality? Fidelity Investments, one of the country’s leading workplace benefits providers3 and America’s No. 1 IRA provider4, today released its Q2 2022 analysis of savings behaviors and account balances for more than 35 million IRA, 401(k), and 403(b) retirement accounts, and although average account balances have decreased -- not surprising, given the stock market’s decline in Q2 -- there was also good news to be found. The drop in average balances was below the S&P's decline of 16.1% for Q2 2022 and below Q1 2020, the last period with significant market volatility. In addition, retirement savers continue to look long-term, as total 401(k) savings rates still hovered at record levels, the number of IRAs on Fidelity’s platform continued to increase and the percentage of employees with 401(k) loans remained low for the fifth consecutive quarter.

“Although many Americans are understandably concerned about the economy, record-high inflation and markets at this time, it’s encouraging to see the prevailing emotion has been to stay calm and focused on one’s retirement objectives,” said Kevin Barry, president of Workplace Investing at Fidelity Investments. “Saving for retirement is a goal that is decades in the making, and there will naturally be many twists and turns. However, the best action savers can take to help achieve success is to consistently save and invest.”

Findings from Fidelity’s Q2 2022 analysis include:

- Average retirement account balances decreased, but less than the market decline5 in Q2—and less than the last major period of market volatility. The average IRA balance6 was $110,800 in Q2, a 17.9% decrease from Q2 2021 and a 12.8% decrease from last quarter. The average 401(k) balance7 dropped to $103,800 in the quarter, down 20% from a year ago and 15% from Q1 2022. The average 403(b) account balance8 decreased to $93,300, down 18% from a year ago and a decrease of 13% from last quarter. However, all these declines were less than the last period of major market volatility, Q1 2020, taking place at the very start of the pandemic, when the average 401(k) balance decreased by 19% and IRA balances decreased by 14%.

Average Retirement Account Balances |

||||

|

|

|

|

|

|

Q2 2022 |

Q1 2022 |

Q2 2021 |

Q2 2012 |

IRA |

$110,800 |

$127,100 |

$134,900 |

$73,200 |

401(k) |

$103,800 |

$121,700 |

$129,300 |

$73,300 |

403(b) |

$93,300 |

$107,600 |

$113,300 |

$56,800 |

- Gen Z 401(k) savers heavily invested in target date funds experienced smallest declines. Interestingly, among Gen Z1 savers, who are heavily invested in target date funds, the average account balance dropped by only 8% from last quarter. As of Q2, 85% of Gen Z savers have all of their 401(k) savings in a target date fund. The use of target date funds as a default option continues to increase in popularity, with a 93.2% plan sponsor adaptation rate in Q2 2022, up from 88.1% in Q2 2017, just five years ago.

- Significant growth occurred in IRA6 accounts, especially among Gen Z and Millennials1. The total number of Fidelity IRA accounts continues to climb, reaching 12.8 million, a 10.6% increase over Q2 of last year. Younger generations continue to lead the way, with the number of accounts for Gen Z increasing by 87% when compared to Q2 2021 and the number of Millennial accounts increasing by 24%. Account growth for females—who make up 45% of total IRA accounts—saw a year-over-year increase of 92% for Gen Z and 24% for Millennials. These accounts continue to be active, with the number of contributing accounts year to date increasing 4.1% over Q2 2021 and in particular, the number of Millennial Roth IRA accounts with a contribution up 7.8% year to date.

- Total 401(k) savings rates continue to hover at record levels. Despite the market volatility of the past two quarters, 401(k) plans continue to see steady contributions from both individuals and their employers. The total savings rate for the second quarter, which reflects a combination of employee and employee 401(k) contributions, continues the positive momentum achieved in the first quarter, with a 13.9% contribution rate, just below Fidelity's suggested savings rate of 15%. Men continued to save at higher rates than women (14.7% vs. 13.7%), while pre-retiree Boomers saved at the highest levels (16.6%), although even Gen Z participants saved in the double digits (10%).

- The majority of retirement savers did not make changes to their asset allocation. Only 5.0% of 401(k) and 403(b) savers made a change to the asset allocation in the second quarter, slightly lower than the 5.3% that made a change in Q1 and consistent with the number of individuals who made a change to their allocation in Q2 2021. Of the savers making a change this past quarter, 85% only made one, and the top change involved shifting savings to more conservative investments (38%).

- Outstanding 401(k) loans and average loan amounts continued to decline. The percentage of 401(k) savers initiating a new loan continues to remain low, with only 2.4% of participants initiating a loan in Q2. In addition, the percentage of participants with a loan outstanding also moved downward, dropping to 16.7% for Q2 2022—which is a significant drop compared to 18.9% in Q2 2020 at the start of the pandemic.

Staying Committed to Saving Can Pay Off in the Long Run with Retirement Savings

Although the current level of uncertainty may raise questions about the wisdom of taking a “stay the course” approach toward retirement savings, there are strong reasons to suggest this remains the best approach. For example, when markets rebound, they tend to do so quickly, especially if the market avoids going into a recession, as many experts continue to suggest. In fact, during the month of July 2022, the S&P increased by 9.1%, enjoying its best month since 20209.

“When it comes to the markets, we often observe that sharp drops are quickly followed by a corresponding rise,” said Barry. “This pattern occurred with the last period of market volatility in 2020, where that first quarter decline was followed by a double digit rebound across retirement account balances -- and by the end of 2020, retirement balances had reached record highs. This speaks to the importance of looking long-term and not over-reacting, so you are able to take advantage of any market peaks.”

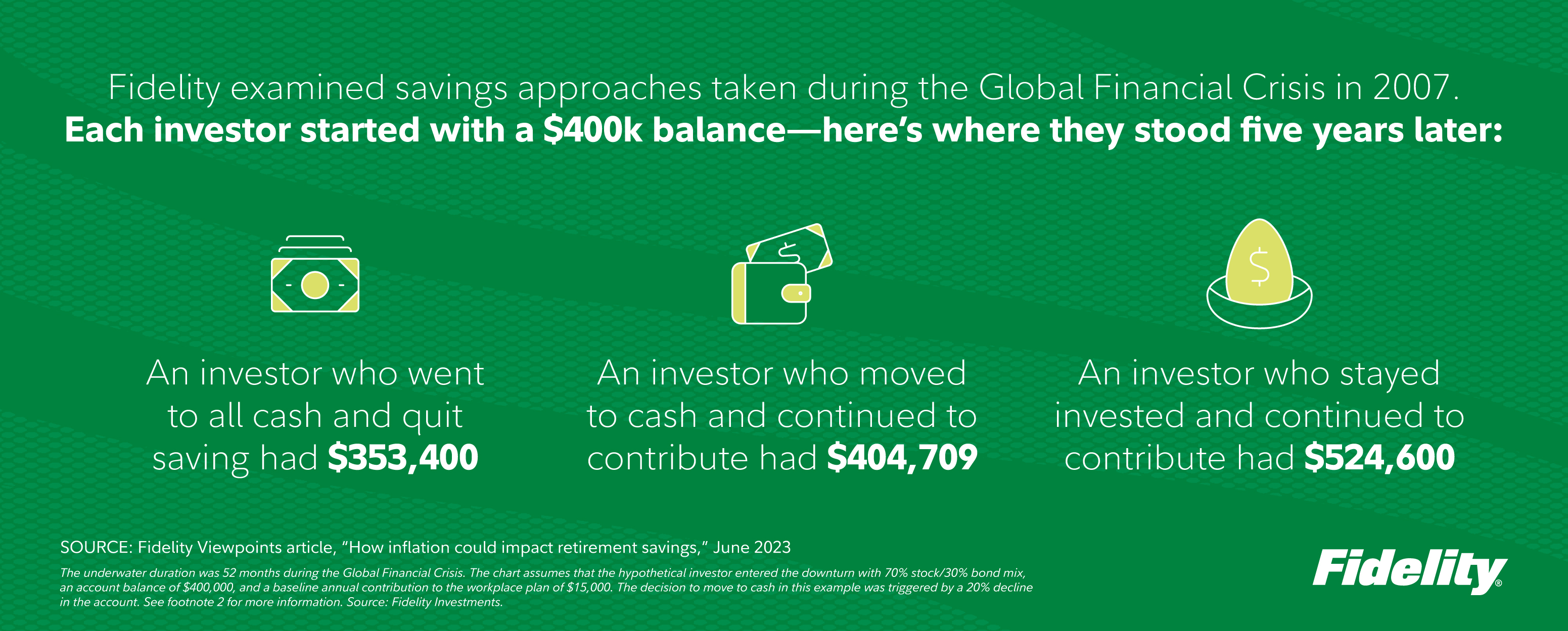

Another important reason is that staying invested and making steady contributions is actually one way to help savings recover from a downturn. To demonstrate what this means in real life, Fidelity recently examined three different savings approaches a 401(k) investor could have taken with their savings during the Global Financial Crisis of 2007-2009. Each investor started out with $400,000 in 2007—and Fidelity tracked how those savings performed as of February 2012:

For additional information on Fidelity’s Q2 2022 analysis, click here to access Fidelity’s “Building Financial Futures” overview, which provides additional details and insight on retirement trends and data.

About Fidelity Investments

Fidelity's mission is to inspire better futures and deliver better outcomes for the customers and businesses we serve. With assets under administration of $9 .9 trillion, including discretionary assets of $3. 7 trillion as of June 30, 2022, we focus on meeting the unique needs of a diverse set of customers. Privately held for over 75 years, Fidelity employs more than 58,000 associates who are focused on the long-term success of our customers. For more information about Fidelity Investments, visit www.fidelity.com/aboutfidelity/our-company.

Keep in mind that investing involves risk. The value of your investment will fluctuate over time, and you may gain or lose money.

Past performance is no guarantee of future results.

The S&P 500® Index is a market capitalization-weighted index of 500 common stocks chosen for market size, liquidity, and industry group representation to represent US equity.

Target Date Funds are an asset mix of stocks, bonds and other investments that automatically becomes more conservative as the fund approaches its target retirement date and beyond. Principal invested is not guaranteed.

Fidelity Brokerage Services LLC, Member NYSE, SIPC

900 Salem Street, Smithfield, RI 02917

Fidelity Distributors Company LLC,

500 Salem Street, Smithfield, RI 02917

National Financial Services LLC, Member NYSE, SIPC,

245 Summer Street, Boston, MA 02110

1042902.1.0

© 2022 FMR LLC. All rights reserved

Follow us on Twitter @FidelityNews

Visit About Fidelity and our online newsroom

Subscribe to emailed news from Fidelity

________________________

1 Generations as defined by Pew Research: Gen Z (born 1997-2012), Millennials (1981-1996), Gen X (1965-1980) and Boomers (1946-1964).

2 Fidelity Investments Q2 Participant Well-being survey, conducted by Ipsos, surveyed 1,100 adults between April 18-26, 2022.

3 Based on PLANSPONSOR Magazine's "2021 Recordkeeping Survey," June 2021 and "Plan Administration Guide, Part 1" which offers insight into the provider marketplace for defined benefit (DB), stock plan and health savings account (HSA) administration, May 2018.

4 Based on Cerulli Associates’ “Top-10 IRA Providers by AUA, 4Q 2019 – 4Q 2021.”

5 Based on S&P performance from April 1 - June 31, 2022.

6 Fidelity business analysis of 12.8 million IRA accounts as of June 30, 2022.

7 Analysis based on 24,000 corporate defined contribution plans and 21.7 million participants as of June 30, 2022. These figures include the advisor-sold market but exclude the tax-exempt market. Excluded from the behavioral statistics are non-qualified defined contribution plans and plans for Fidelity’s own employees.

8 Based on Fidelity analysis of 10,260 Tax-exempt plans and 7.6 million plan participants as of June 30, 2022. Considers average balance across all active plans for 5.7M unique individuals employed in tax-exempt market.

9 SOURCE: The S&P 500 had its best month since November 2020. - The New York Times (nytimes.com)