")

ARLINGTON, Va.--(BUSINESS WIRE)--E*TRADE Financial Corporation (NASDAQ: ETFC) today announced results from the most recent wave of StreetWise, the E*TRADE quarterly tracking study of experienced investors. Results show retirement trends among Gen Z and Millennial investors amid the COVID-19 crisis:

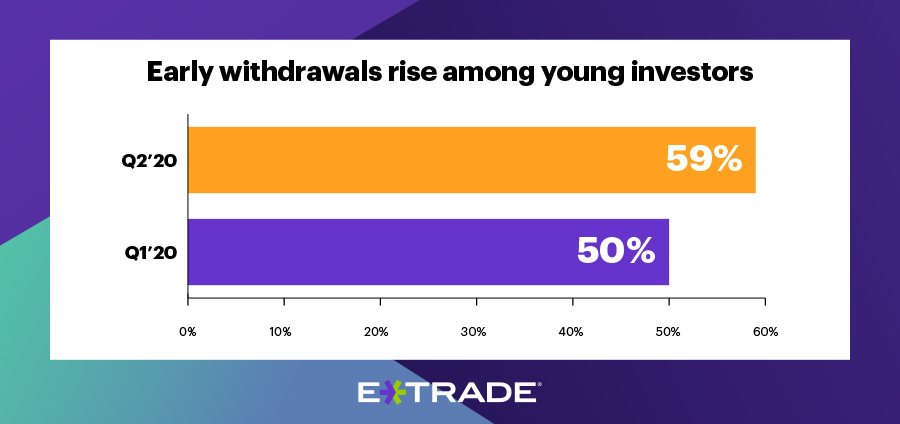

- They’re significantly more likely to take an early withdrawal. Nearly three out of five young investors (59%) said they have withdrawn early from their retirement accounts, compared to just one-third of the total population (33%). Since last quarter, early retirement withdrawals among young investors shot up nine percentage points.

- And they’re worried retirement funds may run dry. More than half of investors under 34 (51%) are worried about their lack of retirement savings, compared to almost one third of the total population (32%). In fact, not having enough saved for retirement became young investors’ #1 worry this quarter, outpacing concern over loss of a loved one.

- Barriers to retirement loom large. Among young investors, the top barrier to saving for retirement is housing costs (67%), followed by education (64%) and health care costs (62%), compared to 44%, 34%, and 47% of the total population, respectively.

“Young investors have a barrage of financial obligations—whether it’s paying down student debt or a mortgage, saving for retirement, or helping care for their parents,” said Mike Loewengart, Managing Director of Investment Strategy at E*TRADE Financial. “The recent health crisis has only magnified these issues, forcing some Millennial and Gen Z investors to tap their retirement funds for relief. It’s important for young investors to remember that they have a significant benefit their older counterparts do not—time. Making consistent contributions today, no matter how small, can make an impact over the long term.”

Mr. Loewengart offered additional retirement planning and long-term investing tips for young investors:

- Kickstart retirement contributions. Consider enrolling in your company’s retirement plan and taking advantage of matching contributions, if they are offered. If an employer-sponsored plan is not available, explore other tax-advantaged accounts like IRAs. Young investors have a long financial future ahead of them—by saving early, they can reap the potential benefits of compounding interest and grow their nest egg.

- Consider automatic investing. One way to build good financial habits is to set up automatic deposits into a retirement account. While you cannot control the market or your investing returns, you can control how much you add to your account. By enabling automatic investing, you can also reduce risk in your portfolio through dollar-cost averaging—potentially benefiting from the inevitable ups and downs of the market.

- Volatility is normal—don’t lose sight of your goals. As frightening as downturns can be, history has shown the market bounces back. Consumers who remain invested in the market and committed to their portfolio are best positioned to benefit in the long run. On the other hand, those who move to the sidelines and turn to cash could lose out on potential returns and lock in current losses.

E*TRADE aims to enhance the financial independence of traders and investors through a powerful digital offering and professional guidance. To learn more about E*TRADE’s trading and investing platforms and tools, visit etrade.com.

For useful trading and investing insights from E*TRADE, follow the company on Twitter, @ETRADE.

Automatic Investing and dollar-cost averaging do not ensure a profit or protect against loss in declining markets. Investors should consider their financial ability to continue their purchases through periods of low price levels.

About the Survey

This wave of the survey was conducted from April 1 to April 8 of 2020 among an online US sample of 940 self-directed active investors who manage at least $10,000 in an online brokerage account. The survey has a margin of error of ±3.20 percent at the 95 percent confidence level. It was fielded and administered by Dynata. The panel is broken into thirds of active (trade more than once a week), swing (trade less than once a week but more than once a month), and passive (trade less than once a month). The panel is 60% male and 40% female, with an even distribution across online brokerages, geographic regions, and age bands. The <34 data set is comprised of 255 investors between the ages of 18 and 34.

About E*TRADE Financial and Important Notices

E*TRADE Financial and its subsidiaries provide financial services including brokerage and banking products and services to retail customers. Securities products and services, including mutual funds and ETFs, are offered by E*TRADE Securities LLC (Member FINRA/SIPC). Commodity futures and options on futures products and services are offered by E*TRADE Futures LLC (Member NFA). Managed Account Solutions are offered through E*TRADE Capital Management, LLC, a Registered Investment Adviser. Bank products and services are offered by E*TRADE Bank, and RIA custody solutions are offered by E*TRADE Savings Bank, both of which are national federal savings banks (Members FDIC). More information is available at www.etrade.com.

The information provided herein is for general informational purposes only and should not be considered investment advice. Past performance does not guarantee future results.

E*TRADE Financial, E*TRADE, and the E*TRADE logo are trademarks or registered trademarks of E*TRADE Financial Corporation. ETFC-G

© 2020 E*TRADE Financial Corporation. All rights reserved.

E*TRADE Financial Corporation engages Dynata to program, field, and tabulate the study. Dynata provides digital research data and has locations in the Americas, Europe, the Middle East and Asia-Pacific. For more information, please go to www.dynata.com.

Referenced Data

Have you ever taken out money from an IRA or 401(k) before the age of 59.5? |

||||

|

Q1 Total |

Q1

|

Q2

|

Q2

|

Yes |

33% |

50% |

33% |

59% |

How often, if at all, do you worry about each of the following? |

|||

|

Q2

|

Q1

|

Q2

|

Not having enough saved for retirement |

32% |

38% |

51% |

Loss of a loved one |

33% |

40% |

47% |

Loss of a job |

24% |

35% |

43% |

Personal relationship issues |

24% |

37% |

42% |

Not understanding how to invest smartly |

23% |

37% |

42% |

Physical injury |

22% |

33% |

38% |

When it comes to your personal ability to save for retirement, how much of a barrier is each of the following? |

||

|

Q2

|

Q2

|

Rent or mortgage |

44% |

67% |

Education costs or paying down student loans |

34% |

64% |

Health care costs |

47% |

62% |

Living expenses like food or utilities |

41% |

60% |

Retail shopping and/or eating at restaurants |

33% |

58% |

Wanting to live for today |

37% |

55% |

Having an older child live with you |

27% |

53% |

Childcare |

25% |

50% |

Having a parent live with you |

27% |

49% |

Gen Z and Millennials (young investors) are defined as age 18–34 years old