reports its full-year and fourth-quarter 2018 results. (Graphic: Business Wire)")

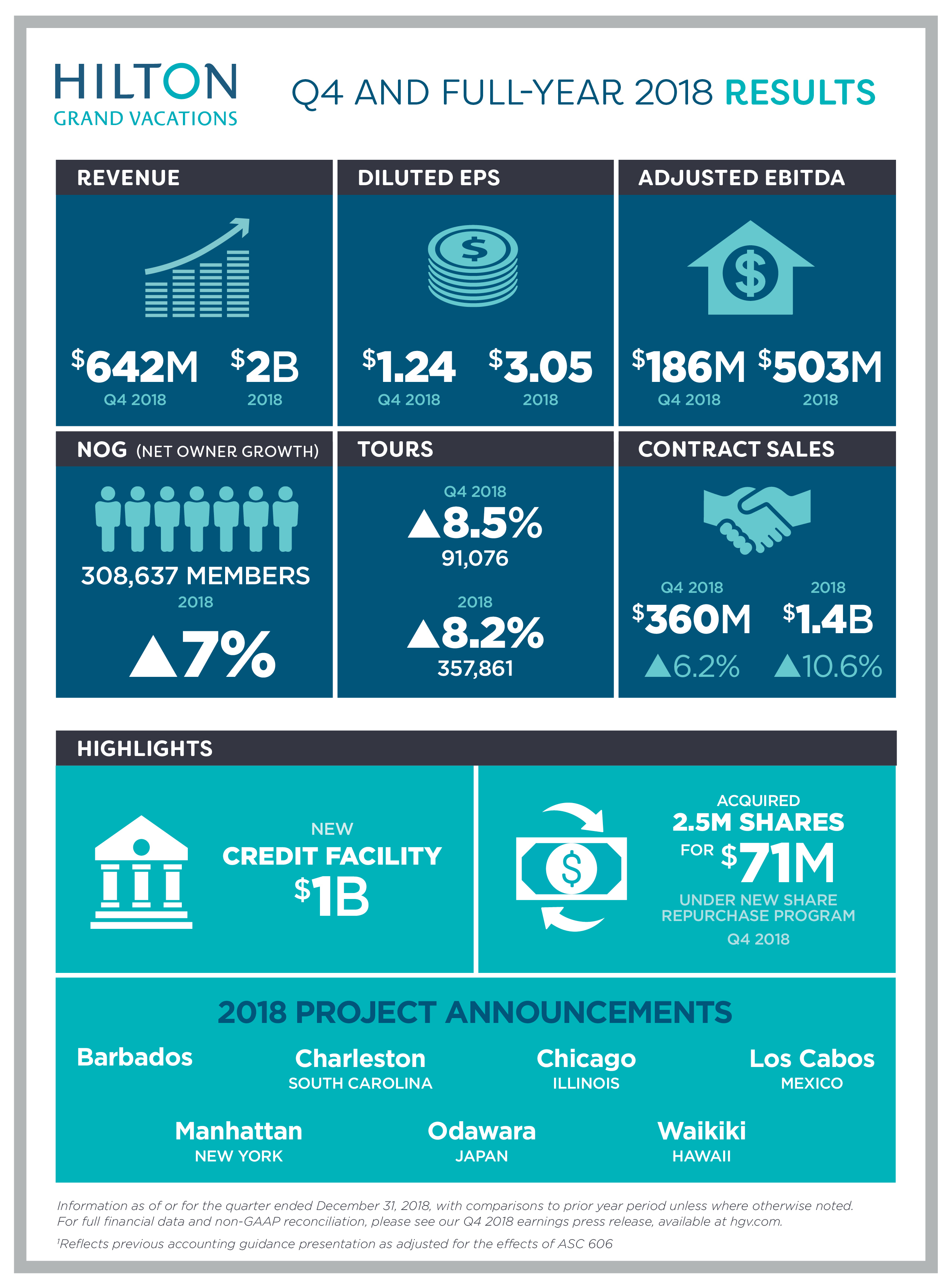

ORLANDO, Fla.--(BUSINESS WIRE)--Hilton Grand Vacations Inc. (NYSE:HGV) (“HGV” or “the Company”) today reports its full-year and fourth-quarter 2018 results. Highlights include:

KEY HIGHLIGHTS

Full-Year 2018 Results

- Total revenues were $2.0 billion, net income was $298 million and diluted EPS was $3.05.

- Adjusted EBITDA was $503 million, which was at the high end of guidance. Adjusted EBITDA includes a $79 million net benefit from recognitions related to sales that occurred prior to 2018.

- Contract sales increased 10.6 percent and Net Owner Growth (NOG) was 7.0 percent.

- Adjusted free cash flow was ($44) million.

- Increased credit facility to $1 billion and announced $200 million share repurchase authorization.

- Repurchased 2.5 million shares for $71 million under the new authorization at an average price of $28.62.

Outlook

- Increasing diluted EPS guidance to $2.74 to $2.89 from $2.68 to $2.84 to reflect fourth quarter 2018 share repurchases.

- Net income is projected to be between $260 million and $275 million.

- Adjusted EBITDA is projected to be between $450 million and $470 million.

- Contract sales are projected to increase 9.0 to 11.0 percent.

- Adjusted free cash flow is projected to be between $60 million and $120 million.

- 2019 outlook assumes no construction-related deferrals, recognitions or additional share repurchases.

Overview – Full-Year 2018

“2018 was a remarkable year as we saw 7 percent NOG growth and double-digit contract sales and Adjusted EBITDA growth,” says Mark Wang, president and CEO, Hilton Grand Vacations. “More importantly, we successfully put in place a pipeline of high-return projects in high-demand markets to accelerate our growth in 2019 and beyond. With our recent project announcement, Maui joins Japan, Charleston, Cabo, Chicago and Barbados on the roster of exciting new destinations we’ve announced over the past 15 months. We believe our strong 2018 results and the long-term outlook we shared at our recent Investor Day demonstrate HGV’s ability to continue our momentum and drive long-term value for our shareholders.”

For the year ended Dec. 31, 2018, total revenues were $2.0 billion compared to $1.7 billion for the year ended Dec. 31, 2017. Diluted EPS was $3.05 for the year ended Dec. 31, 2018, compared to $3.28 for the year ended Dec. 31, 2017. Net income and Adjusted EBITDA was $298 million and $503 million, respectively, for the year ended Dec. 31, 2018, compared to $327 million and $395 million, respectively, for the year ended Dec. 31, 2017.

Net income and Adjusted EBITDA for the year ended Dec. 31, 2018, included a $79 million net benefit from recognitions related to sales at The Residences property that occurred prior to 2018 that were deferred until the second quarter of 2018 when construction of that project was completed.

Net income for the year ended Dec. 31, 2017, included a deferred income tax benefit of $129 million, which was mostly attributable to a benefit of $132 million for the quarter ended Dec. 31, 2017, related to the one-time re-measurement of net deferred income taxes under the new U.S. federal income tax rate provided by the Tax Cuts and Jobs Act of 2017.

Segment Highlights – Full Year 2018

Real Estate Sales and Financing

For the year ended Dec. 31, 2018, Real Estate Sales and Financing segment revenues were $1.5 billion, an increase of 18.0 percent compared to the year ended Dec. 31, 2017. Real Estate Sales and Financing segment Adjusted EBITDA and Adjusted EBITDA margin was $447 million and 30.6 percent, respectively, for the year ended Dec. 31, 2018, compared to $359 million and 29.0 percent, respectively, for the year ended Dec. 31, 2017.

Results for the year ended Dec. 31, 2018, included a $79 million net benefit from recognitions related to sales at The Residences property that occurred prior to 2018 that were deferred until the second quarter of 2018 when construction of that project was completed.

For the year ended Dec. 31, 2018, contract sales increased 10.6 percent to $1.4 billion compared to the year ended Dec. 31, 2017. Fee-for-service contract sales represented 55.0 percent of contract sales for the year ended Dec. 31, 2018, compared to 54.4 percent for the prior year. For the year ended Dec. 31, 2018, tours increased 8.2 percent to 357,861 and VPG increased 2.4 percent to $3,743 compared to the prior year.

Financing revenues were $158 million for the year ended Dec. 31, 2018, an increase of 7.5 percent compared to the prior year.

The weighted average FICO score of new loans made to U.S. and Canadian borrowers at the time of origination increased to 749 for the year ended Dec. 31, 2018, from 743 for the year ended Dec. 31, 2017.

For the year ended Dec. 31, 2018, 65.8 percent of HGV’s sales were to customers who financed part of their purchase.

As of Dec. 31, 2018, gross timeshare financing receivables were $1.3 billion with a weighted average interest rate of 12.3 percent and a weighted average remaining term of 7.8 years. As of Dec. 31, 2018, 93.2 percent of HGV’s financing receivables were current, compared to 94.6 percent as of Dec. 31, 2017.

Resort Operations and Club Management

For the year ended Dec. 31, 2018, Resort Operations and Club Management segment revenues were $422 million, an increase of 15.0 percent compared to the year ended Dec. 31, 2017. Resort Operations and Club Management segment Adjusted EBITDA and Adjusted EBITDA margin was $245 million and 58.1 percent, respectively, for the year ended Dec. 31, 2018, compared to $204 million and 55.6 percent, respectively, for the year ended Dec. 31, 2017.

Overview – Fourth Quarter 2018

For the quarter ended Dec. 31, 2018, diluted EPS was $1.24 compared to $1.83 for the quarter ended Dec. 31, 2017. Net income and Adjusted EBITDA was $120 million and $186 million, respectively, for the quarter ended Dec. 31, 2018, compared to $183 million and $101 million, respectively, for the quarter ended Dec. 31, 2017. Total revenues for the quarter ended Dec. 31, 2018, were $642 million compared to $447 million for the quarter ended Dec. 31, 2017.

Net income and Adjusted EBITDA for the quarter ended Dec. 31, 2018, included an $81 million net benefit from recognitions related to sales at the Ocean Tower property that occurred during the first nine months of 2018 that were deferred until the fourth quarter of 2018 when construction of that phase of the project was completed.

As noted, results for the quarter ended Dec. 31, 2017, included a deferred income tax benefit of $132 million.

Segment Highlights – Fourth Quarter 2018

Real Estate Sales and Financing

For the quarter ended Dec. 31, 2018, Real Estate Sales and Financing segment revenues were $495 million, an increase of 53.3 percent compared to the quarter ended Dec. 31, 2017. Real Estate Sales and Financing segment Adjusted EBITDA and Adjusted EBITDA margin was $173 million and 34.9 percent, respectively, for the quarter ended Dec. 31, 2018, compared to $96 million and 29.7 percent, respectively, for the quarter ended Dec. 31, 2017.

Results for the quarter ended Dec. 31, 2018, included an $81 million net benefit from recognitions related to sales at the Ocean Tower property that occurred during the first nine months of 2018 that were deferred until the fourth quarter of 2018 when construction of that phase of the project was completed.

Contract sales for the quarter ended Dec. 31, 2018, increased 6.2 percent to $360 million compared to the quarter ended Dec. 31, 2017. Fee-for-service contract sales represented 56.1 percent of contract sales for the quarter ended Dec. 31, 2018, compared to 54.9 percent for the quarter ended Dec. 31, 2017. For the quarter ended Dec. 31, 2018, compared to the quarter ended Dec. 31, 2017, tours increased 8.5 percent to 91,076 and VPG decreased 2.0 percent to $3,775.

Financing revenues were $41 million for the quarter ended Dec. 31, 2018, an increase of 7.9 percent compared to the quarter ended Dec. 31, 2017.

Resort Operations and Club Management

For the quarter ended Dec. 31, 2018, Resort Operations and Club Management segment revenue was $118 million, an increase of 21.6 percent compared to the quarter ended Dec. 31, 2017. Resort Operations and Club Management segment Adjusted EBITDA and Adjusted EBITDA margin was $66 million and 55.9 percent, respectively, for the quarter ended Dec. 31, 2018, compared to $51 million and 52.6 percent, respectively, for the quarter ended Dec. 31, 2017.

Inventory

The estimated contract sales value of HGV’s total pipeline is approximately $9.9 billion at current pricing, which represents approximately 7.0 years of sales at the current trailing 12-month sales pace.

The total pipeline includes approximately 1.4 years of sales relating to inventory that is currently available for sale at open or soon-to-open projects. The remaining 5.6 years of sales is inventory at new or existing projects that will become available for sale in the future upon registration, delivery or construction.

Owned inventory represents 76 percent of HGV’s total pipeline. Approximately 13 percent of the owned inventory pipeline is currently available for sale.

Fee-for-service inventory represents 24 percent of HGV’s total pipeline. Approximately 40 percent of the fee-for-service inventory pipeline is currently available for sale.

With 32 percent of the pipeline consisting of just-in-time inventory and 24 percent consisting of fee-for-service inventory, capital-efficient inventory represents 56 percent of HGV’s total pipeline.

Balance Sheet and Liquidity

Total cash and cash equivalents was $180 million as of Dec. 31, 2018, including $72 million of restricted cash.

As of Dec. 31, 2018, HGV had $604 million of corporate debt, net outstanding with a weighted average interest rate of 5.2 percent and $759 million of non-recourse debt, net outstanding with a weighted average interest rate of 3.1 percent.

Free cash flow was ($222) million for the year ended Dec. 31, 2018, compared to $309 million in the prior period. Adjusted free cash flow was ($44) million for the year ended Dec. 31, 2018, compared to $200 million in the prior period.

In November, the Company increased its credit facility to $1 billion from $400 million, including the expansion of its revolver to $800 million from $200 million and refinanced and increased its existing term loan to $200 million. The new facility includes incrementally better pricing than the previous facility and provides HGV greater flexibility to pursue its capital deployment strategies. As of Dec. 31, 2018, there was $684 million of available capacity on the revolver.

Share Repurchase Program

On Nov. 28, 2018, the Company announced that its board of directors approved a $200 million share repurchase program. Under the program, repurchases may be carried out through open-market purchases, block trades or other transactions subject to customary restrictions.

Under the new authorization, during the fourth quarter, the Company repurchased 2.5 million shares for $71 million at an average price of $28.62. This was the maximum amount permitted given daily trading volume restrictions and the number of non-blackout trading days available during the quarter.

Subsequent Event

Subsequent to the fourth quarter, HGV announced that it will develop its first property on the Hawaiian island of Maui. Maui Bay Villas by Hilton Grand Vacations will be HGV’s 10th property in Hawaii. The multi-phase, 388-unit project is located on a 27-acre site on the island’s southwestern coast with 740 feet of oceanfront. The resort will offer a selection of one-, two- and three-bedroom suites across a resort-style campus comprised of a dozen one- to four-story buildings. The initial project phase, which is scheduled for completion in early 2021, includes 131 units within four buildings and all supporting buildings and improvements. Planned amenities include a clubhouse with restaurant, keiki club, fitness center, grab-and-go market, “super pool” with pool bar, oceanfront beach club and over 15 acres of open-lawn recreational space. Sales are anticipated to begin in early 2020. The development costs for this project were included in the 2019-2021 inventory spending guidance the Company provided at its Investor Day on Dec. 4, 2018.

Total Construction Deferrals and/or Recognitions Included in Results Reported Under Accounting Standards Codification Topic 606 (“ASC 606”)

The Company’s Adjusted EBITDA as reported under ASC 606 includes construction-related recognitions and deferrals of revenues and related expenses as detailed in Table T-1. Under ASC 606, the Company defers revenues and related expenses pertaining to sales at projects that occur during periods when that project is under construction until the period when construction is completed.

HGV deferred revenues and expense related to sales made at Ocean Tower for the first three quarters of 2018 and recognized them in the fourth quarter of 2018 when construction was completed on this project. Likewise, HGV deferred revenues and expense related to sales made at The Residences in the first quarter of 2018 and recognized them in the second quarter of 2018 when construction was completed on this project. These deferrals and recognitions of sales made in 2018 offset and there was no net financial impact in 2018.

The $79 million net recognition impact for 2018 relates to the recognition of revenues and expenses related to sales made at The Residences prior to 2018 that were recognized in the second quarter of 2018 when construction was completed. A portion of these pre-2018 sales had been partially recognized in prior periods under the previous accounting guidance, but as part of the adoption of ASC 606 on Jan. 1, 2018, those recognitions were reversed with a cumulative adjustment to retained earnings.

| T-1 | ||||||||||||||||||

| Total Construction Recognitions (Deferrals) | ||||||||||||||||||

| 2018 | ||||||||||||||||||

|

First Quarter |

Second Quarter |

Third Quarter |

Fourth Quarter |

Full Year |

||||||||||||||

| Net income | $ | 30 | $ | 107 | $ | 41 | $ | 120 | $ | 298 | ||||||||

| Interest expense | 7 | 8 | 7 | 8 | 30 | |||||||||||||

| Income tax expense | 10 | 39 | 15 | 41 | 105 | |||||||||||||

| Depreciation and amortization | 8 | 8 | 9 | 11 | 36 | |||||||||||||

|

Interest expense and depreciation and amortization included in equity in earnings from unconsolidated affiliates |

1 | 1 | 1 | 1 | 4 | |||||||||||||

| EBITDA | 56 | 163 | 73 | 181 | 473 | |||||||||||||

| Other (gain) loss, net | 1 | (1 | ) | 1 | — | 1 | ||||||||||||

| Share-based compensation expense | 3 | 5 | 5 | 3 | 16 | |||||||||||||

| Other adjustment items | 2 | 8 | 1 | 2 | 13 | |||||||||||||

| Adjusted EBITDA | $ | 62 | $ | 175 | $ | 80 | $ | 186 | $ | 503 | ||||||||

|

NET CONSTRUCTION DEFERRAL ACTIVITY |

||||||||||||||||||

| Sales of VOI, net | $ | (66 | ) | $ | 91 | $ | (45 | ) | $ | 153 | $ | 133 | ||||||

| Cost of VOI sales | (21 | ) | 20 | (13 | ) | 50 | 36 | |||||||||||

| Sales, marketing, general and administrative expense | (8 | ) | 11 | (7 | ) | 22 | 18 | |||||||||||

| Net construction recognitions (deferrals) | $ | (37 | ) | $ | 60 | $ | (25 | ) | $ | 81 | $ | 79 | ||||||

Comparison of Reported Results Under ASC 606 Compared to Previous Accounting Guidance

The following discussion relates to the reconciliation of HGV’s financial results as reported under the current accounting guidance ASC 606 and the “previous accounting guidance,” ASC 605 as presented in tables T-16 through T-21. Throughout 2018, to assist in the transition from ASC 605 to ASC 606, HGV has been reconciling its reported 2018 results to ASC 605. Beginning in 2019, HGV will no longer present this reconciliation.

Under ASC 606, recognitions of previously deferred revenues and expenses increased reported revenue, net income and Adjusted EBITDA for the year and quarter ended Dec. 31, 2018, compared to ASC 605. Under 605, total revenues, net income and Adjusted EBITDA were $1.9 billion, $247 million and $435 million, respectively, for the year ended Dec. 31, 2018, and $513 million, $66 million and $114 million, respectively, for the quarter ended Dec. 31, 2018.

Table T-2 shows that construction-related recognitions increased HGV’s 2018 reported financial results under ASC 606 by $67 million compared to ASC 605. This reflects the recognition of revenues and expenses related to sales made and deferred at The Residences prior to 2018 that deferred through a cumulative adjustment to retained earnings on Jan. 1, 2018, and subsequently recognized in the second quarter of 2018 when construction was completed on this project. Table T-2 also reflects offsetting deferrals and recognitions related to sales made during 2018 at The Residences and Ocean Tower that have no full-year financial impact.

The $12 million variance between the $79 million full-year recognitions shown in Table T-1 and the $67 million full-year recognitions shown in Table T-2 relates to timing differences in how recognitions are treated between ASC 606 and ASC 605. The $67 million represents deferrals that would have been recognized prior to 2018 under ASC 605 based on the percentage of completion approach. As such, they are removed from the 2018 results as part of the reconciliation to ASC 605. The remaining $12 million of deferrals is not removed from the reconciliation because it would have been recognized in 2018 under both ASC 606 and ASC 605 based on percentage of completion.

| T-2 | |||||||||||||||||

| Construction-Related Recognitions (Deferrals) Included in Bridge by Quarter | |||||||||||||||||

| Between “As Reported” Results under ASC 606 and Previous Accounting Guidance | |||||||||||||||||

| 2018 | |||||||||||||||||

|

First |

Second |

Third |

Fourth |

Full |

|||||||||||||

| Sales of VOIs, net (1) | $ | (59 | ) | $ | 87 | $ | (58 | ) | $ | 142 | $ | 112 | |||||

| Cost of VOI sales(1) | (18 | ) | 20 | (18 | ) | 46 | 30 | ||||||||||

| Sales, marketing, general and administrative expense(1) | (8 | ) | 11 | (8 | ) | 20 | 15 | ||||||||||

| Net construction recognitions (deferrals) | $ | (33 | ) | $ | 56 | $ | (32 | ) | $ | 76 | $ | 67 | |||||

| Number of projects in sales and under construction | 2 | 1 | 1 | — | N/A | ||||||||||||

|

____________________ |

||

| (1) | Amounts represent increases (decreases) from current accounting guidance to previous accounting guidance. | |

In addition to construction deferral recognitions, other minor accounting provisions of ASC 606 had a small impact on HGV’s 2018 results. Table T-3 details the construction deferral recognitions and other minor accounting provisions contained in the reconciliation in Table T-19 between the $503 million of 2018 Adjusted EBITDA as reported under ASC 606 and the $435 million as reported under ASC 605.

| T-3 | ||||||||||||

| Construction Deferrals and Other Items Detail in Bridge | ||||||||||||

| Between “As Reported” Results under ASC 606 and Previous Accounting Guidance | ||||||||||||

| Year Ended December 31, 2018 | ||||||||||||

| ($ in millions) |

Construction |

Other(2) |

Total Effect of |

|||||||||

| Sales of VOIs, net | $ | (112 | ) | $ | — | $ | (112 | ) | ||||

| Sales, marketing, brand and other fees | — | 16 | 16 | |||||||||

| Resort and club management | — | 1 | 1 | |||||||||

| Total revenues | (112 | ) | 17 | (95 | ) | |||||||

| Cost of VOI sales | (30 | ) | — | (30 | ) | |||||||

| Sales and marketing | (15 | ) | 16 | 1 | ||||||||

| Depreciation and amortization | — | 2 | 2 | |||||||||

| Income before income taxes | (67 | ) | (1 | ) | (68 | ) | ||||||

| Income tax benefit | 17 | — | 17 | |||||||||

| Net income | $ | (50 | ) | $ | (1 | ) | $ | (51 | ) | |||

| Net income | $ | (50 | ) | $ | (1 | ) | $ | (51 | ) | |||

| Add back: | ||||||||||||

| Depreciation and amortization | — | 2 | 2 | |||||||||

| Income tax benefit | (17 | ) | — | (17 | ) | |||||||

| EBITDA | (67 | ) | 1 | (66 | ) | |||||||

| Other adjustment items | — | (2 | ) | (2 | ) | |||||||

| Adjusted EBITDA | $ | (67 | ) | $ | (1 | ) | $ | (68 | ) | |||

|

____________________ |

||

| (1) | During periods of construction, we defer revenues and certain related direct expenses from the sales of VOIs until construction is completed. | |

| (2) | Includes the following changes under ASC 606 compared to the previous accounting guidance: (i) revenue for certain sales incentives is now presented on a net basis as a decrease to both sales, marketing, brand and other fees and sales and marketing expense rather than on a gross basis; (ii) expected breakage revenue from advanced deposits on prepaid vacation packages is recognized ratably as packages are redeemed rather than upon expiration; and (iii) key money amortization is presented as a reduction to sales, marketing, brand and other fees rather than as amortization expense. | |

Conference Call

Hilton Grand Vacations will host a conference call on Feb. 28, 2019, at 11 a.m. (EST) to discuss fourth-quarter results. Participants may listen to the live webcast by logging onto the Hilton Grand Vacations’ Investor Relations website at http://investors.hgv.com/events-and-presentations. A replay and transcript of the webcast will be available on HGV’s Investor Relations website within 24 hours after the live event.

Alternatively, participants may listen to the live call by dialing 1-888-312-3049 in the U.S. or +1-323-794-2112 internationally. Please use conference ID# 7540297. Participants are encouraged to dial into the call or link to the webcast at least 20 minutes prior to the scheduled start time. In the event of audio difficulties during the call on the toll-free number, participants are advised that accessing the call using the +1-323-794-2112 dial-in number may bypass the source of the audio difficulties.

A telephone replay will be available for seven days following the call. To access the telephone replay, dial 1-888-203-1112 in the U.S. or +1-719-457-0820 internationally and use conference ID# 7540297.

Forward-Looking Statements

This press release contains forward-looking statements within the meaning of Section 27A of the Securities Act of 1933, as amended and Section 21E of the Securities Exchange Act of 1934, as amended. Forward-looking statements convey management’s expectations as to the future of HGV, and are based on management’s beliefs, expectations, assumptions and such plans, estimates, projections and other information available to management at the time HGV makes such statements. Forward-looking statements include all statements that are not historical facts and may be identified by terminology such as the words “outlook,” “believe,” “expect,” “potential,” “goal,” “continues,” “may,” “will,” “should,” “could,” “seeks,” “approximately,” “projects,” predicts,” “intends,” “plans,” “estimates,” “anticipates” “future,” “guidance,” “target,” or the negative version of these words or other comparable words. The forward-looking statements contained in this press release include statements related to HGV’s revenues, earnings, taxes, cash flow and related financial and operating measures, and expectations with respect to future operating, financial and business performance, and other anticipated future events and expectations that are not historical facts.

HGV cautions you that its forward-looking statements involve known and unknown risks, uncertainties and other factors, which may cause the actual results, performance or achievements of HGV to be materially different from the future results, business performance or achievements expressed or implied by its forward-looking statements. HGV’s forward-looking statements are not guarantees of future performance, and you should not place undue reliance on such statements in this press release. Factors that could cause HGV’s actual results to differ materially from those contemplated by its forward-looking statements include risks associated with: the inherent business, financial and operating risks of the timeshare industry, including limited underwriting standards due to the real-time nature of industry sales practices, and the intense competition associated with the industry; HGV’s ability successfully market and sell VOIs; HGV’s development and other activities to source inventory for VOI sales; significant increases in defaults on HGV’s vacation ownership mortgage receivables; the ability of managed homeowner associations to collect sufficient maintenance fees; general volatility in the economy and/or the financial and credit markets; adverse economic or market conditions and trends in the tourism and hospitality industry, which may impact the purchasing and vacationing decisions of consumers; actions of HGV or the occurrence of other events that could cause a breach under or termination of the HGV’s license agreement with Hilton that could affect or terminate our access to the Hilton brands and programs, or actions of Hilton that affect the reputation of the licensed marks or Hilton’s programs; economic and operational uncertainties related to HGV’s expanding global operations, including our ability to manage the outcome and timing of such operations and compliance with anti-corruption, data privacy and other applicable laws and regulations affecting our international operations; the effects of foreign currency exchange; changes in tax rates and exposure to additional tax liabilities; the impact of future changes in legislation, regulations or accounting pronouncements; HGV’s acquisitions, joint ventures, and strategic alliances that may not result in expected benefits, including the termination of material fee-for-service agreements; our dependence on third-party development activities to secure just-in-time inventory; HGV’s use of social media platforms; cyber-attacks, security vulnerabilities, and information technology system failures resulting in disclosure of personal data, company data loss, system outages or disruptions of online services, which could lead to reduced revenue, increased costs, liability claims, harm to user engagement, and harm to HGV’s reputation or competitive position; the impact of claims against HGV that may result in adverse outcomes, including regulatory proceedings or litigation; HGV’s credit facilities, indenture and other debt agreements and instruments, including variable interest rates, operating and financial restrictions, our ability to make scheduled payments, and our ability to refinance our debt on acceptable terms; the continued service and availability of key executives and employees; and catastrophic events or geo-political conditions including war, terrorist activity, political strife or natural disasters that may disrupt HGV’s operations in key vacation destinations. Any one or more of the foregoing factors could adversely impact HGV’s operations, revenue, operating margins, financial condition and/or credit rating.

For additional information regarding factors that could cause HGV’s actual results to differ materially from those expressed or implied in the forward-looking statements in this press release, please see the risk factors discussed in “Part I—Item 1A. Risk Factors” of HGV’s Annual Report on Form 10-K for the fiscal year ended Dec. 31, 2018 and those described from time to time other periodic reports that we file with the U.S. Securities and Exchange Commission. There may be other risks and uncertainties that we are unable to predict at this time or that we currently do not expect to have a material adverse effect on our business. Except for HGV’s ongoing obligations to disclose material information under the federal securities laws, we undertake no obligation to publicly update or review any forward-looking statement, whether as a result of new information, future developments, changes in management’s expectations, or otherwise.

Non-GAAP Financial Measures

The Company refers to certain non-GAAP financial measures in this press release, including EBITDA, Adjusted EBITDA, Adjusted EBITDA margins, free cash flow and adjusted free cash flow. Please see the tables in this press release and “Definitions” for additional information and reconciliations of such non-GAAP financial measures.

About Hilton Grand Vacations Inc.

Hilton Grand Vacations Inc. (NYSE:HGV) is recognized as a leading global timeshare company. With headquarters in Orlando, Florida, Hilton Grand Vacations develops, markets and operates a system of brand-name, high-quality vacation ownership resorts in select vacation destinations. The Company also manages and operates two innovative club membership programs: Hilton Grand Vacations Club® and The Hilton Club®, providing exclusive exchange, leisure travel and reservation services for more than 305,000 club members. For more information, visit www.hgv.com and www.hiltongrandvacations.com.

|

HILTON GRAND VACATIONS INC. |

|

DEFINITIONS |

EBITDA and Adjusted EBITDA

EBITDA, presented herein, is a financial measure that is not recognized under U.S. GAAP that reflects net income (loss), before interest expense (excluding non-recourse debt), a provision for income taxes and depreciation and amortization.

Adjusted EBITDA, presented herein, is calculated as EBITDA, as previously defined, further adjusted to exclude certain items, including, but not limited to, gains, losses and expenses in connection with: (i) asset dispositions; (ii) foreign currency transactions; (iii) debt restructurings/retirements; (iv) non-cash impairment losses; (v) reorganization costs, including severance and relocation costs; (vi) share-based and certain other compensation expenses; (vii) costs related to the spin-off; and (viii) other items.

EBITDA and Adjusted EBITDA are not recognized terms under U.S. GAAP and should not be considered as alternatives to net income (loss) or other measures of financial performance or liquidity derived in accordance with U.S. GAAP. In addition, our definitions of EBITDA and Adjusted EBITDA may not be comparable to similarly titled measures of other companies.

HGV believes that EBITDA and Adjusted EBITDA provide useful information to investors about us and our financial condition and results of operations for the following reasons: (i) EBITDA and Adjusted EBITDA are among the measures used by our management team to evaluate our operating performance and make day-to-day operating decisions; and (ii) EBITDA and Adjusted EBITDA are frequently used by securities analysts, investors and other interested parties as a common performance measure to compare results or estimate valuations across companies in our industry. EBITDA and Adjusted EBITDA have limitations as analytical tools and should not be considered either in isolation or as a substitute for net income (loss), cash flow or other methods of analyzing our results as reported under U.S. GAAP. Some of these limitations are:

- EBITDA and Adjusted EBITDA do not reflect changes in, or cash requirements for, our working capital needs;

- EBITDA and Adjusted EBITDA do not reflect our interest expense (excluding interest expense on non-recourse debt), or the cash requirements necessary to service interest or principal payments on our indebtedness;

- EBITDA and Adjusted EBITDA do not reflect our tax expense or the cash requirements to pay our taxes;

- EBITDA and Adjusted EBITDA do not reflect historical cash expenditures or future requirements for capital expenditures or contractual commitments;

- EBITDA and Adjusted EBITDA do not reflect the effect on earnings or changes resulting from matters that we consider not to be indicative of our future operations;

- EBITDA and Adjusted EBITDA do not reflect any cash requirements for future replacements of assets that are being depreciated and amortized;

- EBITDA and Adjusted EBITDA may be calculated differently from other companies in our industry limiting their usefulness as comparative measures.

Because of these limitations, EBITDA and Adjusted EBITDA should not be considered as discretionary cash available to us to reinvest in the growth of our business or as measures of cash that will be available to us to meet our obligations.

Real Estate Metrics

Contract sales represents the total amount of VOI products under purchase agreements signed during the period where HGV has received a down payment of at least 10 percent of the contract price. Contract sales is not a recognized term under U.S. GAAP and should not be considered in isolation or as an alternative to Sales of VOIs, net or any other comparable operating measure derived in accordance with U.S. GAAP. Contract sales differ from revenues from the Sales of VOIs, net that HGV reports in its consolidated statements of operations due to the requirements for revenue recognition as described in Note 2: Basis of Presentation and Summary of Significant Accounting Policies in the Company’s audited consolidated financial statements, as well as adjustments for incentives and other administrative fee revenues. HGV considers contract sales to be an important operating measure because it reflects the pace of sales in HGV’s business.

Developed Inventory refers to VOI inventory source from projects the Company develops.

Fee-for-Service Inventory refers to VOI inventory HGV sells and manages on behalf of first-party developers.

Just-in-Time Inventory refers to VOI inventory primarily sourced in transactions that are designed to closely correlate the timing of the acquisition with HGV’s sale of that inventory to purchasers.

NOG or Net Owner Growth represents the year-over-year change in membership.

Real estate margin represents sales revenue less the cost of VOI sales and sales and marketing costs, net of marketing revenue. Real estate margin percentage is calculated by dividing real estate margin by sales revenue. HGV considers this to be an important operating measure because it measures the efficiency of the Company’s sales and marketing spending and management of inventory costs.

Sales revenue represents sale of VOIs, net and commissions and brand fees earned from the sale of fee-for-service intervals.

Tour flow represents the number of sales presentations given at HGV’s sales centers during the period.

Volume per guest (“VPG”) represents the sales attributable to tours at HGV’s sales locations and is calculated by dividing Contract sales, excluding telesales, by tour flow. The Company considers VPG to be an important operating measure because it measures the effectiveness of HGV’s sales process, combining the average transaction price with closing rate.

Free cash flow represents cash from operating activities adjusted for share-based compensation, less non-inventory capital spending.

Adjusted free cash flow represents free cash flow less non-recourse debt activities, net.

Resort and Club Management and Rental Metrics

Transient rate represents the total rental room revenue for transient guests divided by total number of transient room nights sold in a given period and excludes room rentals associated with marketing programs, owner usage and the redemption of Club Bonus Points.

| HILTON GRAND VACATIONS INC. | |||

| FINANCIAL TABLES | |||

| CONSOLIDATED BALANCE SHEETS | T-4 | ||

| CONSOLIDATED STATEMENTS OF OPERATIONS | T-5 | ||

| CONSOLIDATED STATEMENTS OF CASH FLOWS | T-6 | ||

| FREE CASH FLOWS RECONCILIATION | T-7 | ||

| SEGMENT REVENUE RECONCILIATION | T-8 | ||

| SEGMENT EBITDA AND ADJUSTED EBITDA TO NET INCOME | T-9 | ||

| REAL ESTATE SALES MARGIN DETAIL SCHEDULE | T-10 | ||

| FINANCING MARGIN DETAIL SCHEDULE | T-11 | ||

| RESORT AND CLUB MARGIN DETAIL SCHEDULE | T-12 | ||

| RENTAL AND ANCILLARY MARGIN DETAIL SCHEDULE | T-13 | ||

| REAL ESTATE SALES AND FINANCING SEGMENT ADJUSTED EBITDA | T-14 | ||

| RESORT AND CLUB MANAGEMENT SEGMENT ADJUSTED EBITDA | T-15 | ||

| EFFECTS OF NEW ACCOUNTING STANDARD | |||

| CONSOLIDATED STATEMENTS OF OPERATIONS – THREE MONTHS ENDED DECEMBER 31, 2018 | T-16 | ||

| CONSOLIDATED STATEMENTS OF OPERATIONS – YEAR ENDED DECEMBER 31, 2018 | T-17 | ||

| SEGMENT EBITDA AND ADJUSTED EBITDA TO NET INCOME – THREE MONTHS ENDED DECEMBER 31, 2018 | T-18 | ||

| SEGMENT EBITDA AND ADJUSTED EBITDA TO NET INCOME – YEAR ENDED DECEMBER 31, 2018 | T-19 | ||

| REAL ESTATE MARGIN – THREE MONTHS ENDED DECEMBER 31, 2018 | T-20 | ||

| REAL ESTATE MARGIN – YEAR ENDED DECEMBER 31, 2018 |

T-21 |

||

| FORWARD-YEAR ADJUSTED EBITDA RECONCILIATION | T-22 | ||

| T-4 | |||||||

| HILTON GRAND VACATIONS INC. | |||||||

| CONSOLIDATED BALANCE SHEETS | |||||||

| (in millions, except share data) | |||||||

| December 31, | |||||||

| 2018 | 2017 | ||||||

| ASSETS | |||||||

| Cash and cash equivalents | $ | 108 | $ | 246 | |||

| Restricted cash | 72 | 51 | |||||

| Accounts receivable, net | 153 | 112 | |||||

| Timeshare financing receivables, net | 1,120 | 1,071 | |||||

| Inventory | 527 | 509 | |||||

| Property and equipment, net | 559 | 238 | |||||

| Investments in unconsolidated affiliates | 38 | 41 | |||||

| Intangible assets, net | 81 | 72 | |||||

| Other assets | 95 | 44 | |||||

| TOTAL ASSETS | $ | 2,753 | $ | 2,384 | |||

| LIABILITIES AND EQUITY | |||||||

| Liabilities: | |||||||

| Accounts payable, accrued expenses and other | $ | 324 | $ | 339 | |||

| Advanced deposits | 101 | 104 | |||||

| Debt, net | 604 | 482 | |||||

| Non-recourse debt, net | 759 | 583 | |||||

| Deferred revenues | 95 | 109 | |||||

| Deferred income tax liabilities | 254 | 249 | |||||

| Total liabilities | 2,137 | 1,866 | |||||

| Commitments and Contingencies | |||||||

| Equity: | |||||||

|

Preferred stock, $0.01 par value; 300,000,000 authorized shares, none issued or outstanding as of December 31, 2018 and 2017 |

— | — | |||||

|

Common stock, $0.01 par value; 3,000,000,000 authorized shares, 94,558,086 and 99,136,304 issued and outstanding as of December 31, 2018 and 2017, respectively |

1 | 1 | |||||

| Additional paid-in capital | 174 | 162 | |||||

| Accumulated retained earnings | 441 | 355 | |||||

| Total equity | 616 | 518 | |||||

| TOTAL LIABILITIES AND EQUITY | $ | 2,753 | $ | 2,384 | |||

| T-5 | ||||||||||||||||

| HILTON GRAND VACATIONS INC. | ||||||||||||||||

| CONSOLIDATED STATEMENTS OF OPERATIONS | ||||||||||||||||

| (in millions, except share data) | ||||||||||||||||

|

Three Months Ended |

Year Ended December 31, |

|||||||||||||||

| 2018 | 2017 | 2018 | 2017 | |||||||||||||

| Revenues | ||||||||||||||||

| Sales of VOIs, net | $ | 307 | $ | 142 | $ | 734 | $ | 548 | ||||||||

| Sales, marketing, brand and other fees | 147 | 143 | 570 | 544 | ||||||||||||

| Financing | 41 | 38 | 158 | 147 | ||||||||||||

| Resort and club management | 56 | 50 | 172 | 158 | ||||||||||||

| Rental and ancillary services | 54 | 41 | 218 | 179 | ||||||||||||

| Cost reimbursements | 37 | 33 | 147 | 135 | ||||||||||||

| Total revenues | 642 | 447 | 1,999 | 1,711 | ||||||||||||

| Expenses | ||||||||||||||||

| Cost of VOI sales | 101 | 41 | 210 | 148 | ||||||||||||

| Sales and marketing | 200 | 171 | 728 | 663 | ||||||||||||

| Financing | 14 | 11 | 49 | 43 | ||||||||||||

| Resort and club management | 14 | 11 | 47 | 43 | ||||||||||||

| Rental and ancillary services | 38 | 34 | 133 | 122 | ||||||||||||

| General and administrative | 33 | 29 | 117 | 104 | ||||||||||||

| Depreciation and amortization | 11 | 8 | 36 | 29 | ||||||||||||

| License fee expense | 25 | 22 | 98 | 87 | ||||||||||||

| Cost reimbursements | 37 | 33 | 147 | 135 | ||||||||||||

| Total operating expenses | 473 | 360 | 1,565 | 1,374 | ||||||||||||

| Interest expense | (8 | ) | (6 | ) | (30 | ) | (27 | ) | ||||||||

| Equity in earnings from unconsolidated affiliates | — | — | — | 1 | ||||||||||||

| Other loss, net | — | (1 | ) | (1 | ) | — | ||||||||||

| Income before income taxes | 161 | 80 | 403 | 311 | ||||||||||||

| Income tax (expense) benefit | (41 | ) | 103 | (105 | ) | 16 | ||||||||||

| Net income | $ | 120 | $ | 183 | $ | 298 | $ | 327 | ||||||||

| Earnings per share: | ||||||||||||||||

| Basic | $ | 1.25 | $ | 1.85 | $ | 3.07 | $ | 3.30 | ||||||||

| Diluted | $ | 1.24 | $ | 1.83 | $ | 3.05 | $ | 3.28 | ||||||||

| T-6 | ||||||||||||||||

| HILTON GRAND VACATIONS INC. | ||||||||||||||||

| CONSOLIDATED STATEMENTS OF CASH FLOWS | ||||||||||||||||

| (in millions) | ||||||||||||||||

|

Three Months Ended |

Year Ended December 31, |

|||||||||||||||

| 2018 | 2017 | 2018 | 2017 | |||||||||||||

| Operating Activities | ||||||||||||||||

| Net income | $ | 120 | $ | 183 | $ | 298 | $ | 327 | ||||||||

| Adjustments to reconcile net income to net cash provided by (used in) operating activities: | ||||||||||||||||

| Depreciation and amortization | 11 | 8 | 36 | 29 | ||||||||||||

| Amortization of cost to obtain a contract | 2 | — | 2 | — | ||||||||||||

| Amortization of deferred financing costs and other | 1 | 1 | 5 | 5 | ||||||||||||

| Provision for loan losses | 19 | 13 | 69 | 58 | ||||||||||||

| Other loss, net | — | 1 | 1 | — | ||||||||||||

| Share-based compensation | 3 | 2 | 16 | 15 | ||||||||||||

| Deferred income tax expense (benefit) | 41 | (124 | ) | 20 | (129 | ) | ||||||||||

| Equity in earnings from unconsolidated affiliates | — | — | — | (1 | ) | |||||||||||

| Distributions received from unconsolidated affiliates | — | — | 2 | — | ||||||||||||

| Net changes in assets and liabilities: | ||||||||||||||||

| Accounts receivable, net | (2 | ) | (7 | ) | (41 | ) | 12 | |||||||||

| Timeshare financing receivables, net | (35 | ) | (28 | ) | (118 | ) | (103 | ) | ||||||||

| Inventory | 31 | 9 | 16 | 47 | ||||||||||||

| Purchase of real estate for future conversion to inventory | — | — | (299 | ) | — | |||||||||||

| Other assets | 30 | 7 | (31 | ) | (4 | ) | ||||||||||

| Accounts payable, accrued expenses and other | (9 | ) | (1 | ) | (24 | ) | 95 | |||||||||

| Advanced deposits | 1 | 2 | 14 | 1 | ||||||||||||

| Deferred revenues | (168 | ) | (10 | ) | (126 | ) | 3 | |||||||||

| Other | 1 | 1 | 1 | 1 | ||||||||||||

| Net cash provided by (used in) operating activities | 46 | 57 | (159 | ) | 356 | |||||||||||

| Investing Activities | ||||||||||||||||

| Capital expenditures for property and equipment | (15 | ) | (10 | ) | (44 | ) | (35 | ) | ||||||||

| Software capitalization costs | (7 | ) | — | (19 | ) | (12 | ) | |||||||||

| Return of investment from unconsolidated affiliates | — | — | 11 | — | ||||||||||||

| Investment in unconsolidated affiliates | (5 | ) | — | (10 | ) | (40 | ) | |||||||||

| Net cash used in investing activities | (27 | ) | (10 | ) | (62 | ) | (87 | ) | ||||||||

| Financing Activities | ||||||||||||||||

| Issuance of debt | 315 | — | 530 | — | ||||||||||||

| Issuance of non-recourse debt | — | — | 663 | 350 | ||||||||||||

| Repurchase and retirement of common stock | (71 | ) | — | (183 | ) | — | ||||||||||

| Repayment of debt | (240 | ) | (3 | ) | (408 | ) | (10 | ) | ||||||||

| Repayment of non-recourse debt | (49 | ) | (31 | ) | (485 | ) | (459 | ) | ||||||||

| Debt issuance costs | (6 | ) | — | (12 | ) | (5 | ) | |||||||||

| Proceeds from stock options exercises | — | — | — | 1 | ||||||||||||

| Payment of withholding taxes on vesting of restricted stock units | — | — | (4 | ) | — | |||||||||||

| Capital contribution | — | — | 3 | — | ||||||||||||

| Net cash (used in) provided by financing activities | (51 | ) | (34 | ) | 104 | (123 | ) | |||||||||

| Net increase (decrease) in cash, cash equivalents and restricted cash | (32 | ) | 13 | (117 | ) | 146 | ||||||||||

| Cash, cash equivalents and restricted cash, beginning of period | 212 | 284 | 297 | 151 | ||||||||||||

| Cash, cash equivalents and restricted cash, end of period | $ | 180 | $ | 297 | $ | 180 | $ | 297 | ||||||||

| T-7 | ||||||||||||||||

| HILTON GRAND VACATIONS INC. | ||||||||||||||||

| FREE CASH FLOWS RECONCILIATION | ||||||||||||||||

| (in millions) | ||||||||||||||||

|

Three Months Ended |

Year Ended December 31, | |||||||||||||||

| 2018 | 2017 | 2018 | 2017 | |||||||||||||

| Cash Flow provided by (used in) operations | $ | 46 | $ | 57 | $ | (159 | ) | $ | 356 | |||||||

| Capital expenditures for property and equipment | (15 | ) | (10 | ) | (44 | ) | (35 | ) | ||||||||

| Software capitalization costs | (7 | ) | — | (19 | ) | (12 | ) | |||||||||

| Free Cash Flow | 24 | 47 | (222 | ) | 309 | |||||||||||

| Non-recourse debt activity, net | (49 | ) | (31 | ) | 178 | (109 | ) | |||||||||

| Adjusted Free Cash Flow | $ | (25 | ) | $ | 16 | $ | (44 | ) | $ | 200 | ||||||

| T-8 | ||||||||||||||||

| HILTON GRAND VACATIONS INC. | ||||||||||||||||

| SEGMENT REVENUE RECONCILIATION | ||||||||||||||||

| (in millions) | ||||||||||||||||

|

Three Months Ended December 31, |

Year Ended December 31, | |||||||||||||||

| 2018 | 2017 | 2018 | 2017 | |||||||||||||

| Revenues: | ||||||||||||||||

| Real estate sales and financing | $ | 495 | $ | 323 | $ | 1,462 | $ | 1,239 | ||||||||

| Resort operations and club management | 118 | 97 | 422 | 367 | ||||||||||||

| Segment revenues | 613 | 420 | 1,884 | 1,606 | ||||||||||||

| Cost reimbursements | 37 | 33 | 147 | 135 | ||||||||||||

| Intersegment eliminations | (8 | ) | (6 | ) | (32 | ) | (30 | ) | ||||||||

| Total revenues | $ | 642 | $ | 447 | $ | 1,999 | $ | 1,711 | ||||||||

| T-9 | ||||||||||||||||

| HILTON GRAND VACATIONS INC. | ||||||||||||||||

| SEGMENT EBITDA AND ADJUSTED EBITDA TO NET INCOME | ||||||||||||||||

| (in millions) | ||||||||||||||||

|

Three Months Ended |

Year Ended December 31, |

|||||||||||||||

| 2018 | 2017 | 2018 | 2017 | |||||||||||||

| Net Income | $ | 120 | $ | 183 | $ | 298 | $ | 327 | ||||||||

| Interest expense | 8 | 6 | 30 | 27 | ||||||||||||

| Income tax expense (benefit) | 41 | (103 | ) | 105 | (16 | ) | ||||||||||

| Depreciation and amortization | 11 | 8 | 36 | 29 | ||||||||||||

|

Interest expense, depreciation and amortization included in equity in earnings from unconsolidated affiliates |

1 | 1 | 4 | 3 | ||||||||||||

| EBITDA | 181 | 95 | 473 | 370 | ||||||||||||

| Other loss, net | — | 1 | 1 | — | ||||||||||||

| Share-based compensation expense | 3 | 2 | 16 | 15 | ||||||||||||

| Other adjustment items (1) | 2 | 3 | 13 | 10 | ||||||||||||

| Adjusted EBITDA | $ | 186 | $ | 101 | $ | 503 | $ | 395 | ||||||||

| Adjusted EBITDA: | ||||||||||||||||

| Real estate sales and financing (2) | $ | 173 | $ | 96 | $ | 447 | $ | 359 | ||||||||

| Resort operations and club management (2) | 66 | 51 | 245 | 204 | ||||||||||||

| Segment Adjusted EBITDA | 239 | 147 | 692 | 563 | ||||||||||||

| Adjustments: | ||||||||||||||||

| Adjusted EBITDA from unconsolidated affiliates | 1 | 1 | 4 | 4 | ||||||||||||

| License fee expense | (25 | ) | (22 | ) | (98 | ) | (87 | ) | ||||||||

| General and administrative (3) | (29 | ) | (25 | ) | (95 | ) | (85 | ) | ||||||||

| Adjusted EBITDA | $ | 186 | $ | 101 | $ | 503 | $ | 395 | ||||||||

| Adjusted EBITDA margin % | 29.0 | % | 22.6 | % | 25.2 | % | 23.1 | % | ||||||||

| EBITDA margin % | 28.2 | % | 21.3 | % | 23.7 | % | 21.6 | % | ||||||||

|

__________________ |

||

| (1) | Includes costs associated with the spin-off transaction of $2 million and $3 million for the three months ended Dec. 31, 2018 and 2017, respectively, and $11 million and $8 million for the years ended Dec. 31, 2018 and 2017, respectively. | |

| (2) | Includes intersegment eliminations, share-based compensation attributable to the segment and other adjustments. | |

| (3) | Excludes share-based compensation and other adjustment items. | |

| T-10 | ||||||||||||||||

| HILTON GRAND VACATIONS INC. | ||||||||||||||||

| REAL ESTATE SALES MARGIN DETAIL SCHEDULE | ||||||||||||||||

| (in millions, except Tour Flow and VPG) | ||||||||||||||||

|

Three Months Ended |

Year Ended December 31, | |||||||||||||||

| 2018 | 2017 | 2018 | 2017 | |||||||||||||

| Contract sales | $ | 360 | $ | 339 | $ | 1,410 | $ | 1,275 | ||||||||

| Tour flow | 91,076 | 83,910 | 357,861 | 330,775 | ||||||||||||

| VPG | $ | 3,775 | $ | 3,854 | $ | 3,743 | $ | 3,657 | ||||||||

| Owned contract sales mix | 43.9 | % | 45.1 | % | 45.0 | % | 45.6 | % | ||||||||

| Fee-for-service contract sales mix | 56.1 | % | 54.9 | % | 55.0 | % | 54.4 | % | ||||||||

| Sales of VOIs, net | $ | 307 | $ | 142 | $ | 734 | $ | 548 | ||||||||

| Adjustments: | ||||||||||||||||

| Fee-for-service sales (1) | 202 | 186 | 776 | 694 | ||||||||||||

| Loan loss provision | 19 | 13 | 69 | 58 | ||||||||||||

| Reportability and other: | ||||||||||||||||

| Deferrals of Sales of VOIs under construction(2) | (153 | ) | 1 | (133 | ) | 5 | ||||||||||

| Fee-for-service sale upgrades, net | (23 | ) | (13 | ) | (63 | ) | (52 | ) | ||||||||

| Other (3) | 8 | 10 | 27 | 22 | ||||||||||||

| Contract sales | $ | 360 | $ | 339 | $ | 1,410 | $ | 1,275 | ||||||||

| Sales of VOIs, net | $ | 307 | $ | 142 | $ | 734 | $ | 548 | ||||||||

| Sales, marketing, brand and other fees | 147 | 143 | 570 | 544 | ||||||||||||

| Less: | ||||||||||||||||

| Marketing revenue and other fees | 32 | 36 | 123 | 145 | ||||||||||||

| Sales revenue | 422 | 249 | 1,181 | 947 | ||||||||||||

| Less: | ||||||||||||||||

| Cost of VOI sales | 101 | 41 | 210 | 148 | ||||||||||||

| Sales and marketing expense, net (4) | 162 | 128 | 575 | 492 | ||||||||||||

| Real estate margin | $ | 159 | $ | 80 | $ | 396 | $ | 307 | ||||||||

| Real estate margin percentage | 37.7 | % | 32.1 | % | 33.5 | % | 32.4 | % | ||||||||

|

__________________ |

||

| (1) | Represents contract sales from fee-for-service properties on which the Company earns commissions and brand fees. | |

| (2) | Includes $112 million cumulative effect of applying ASC 606 for the year ended Dec. 31, 2018. | |

| (3) | Includes adjustments for revenue recognition, including amounts in rescission and sales incentives. | |

| (4) | Includes revenue recognized through our marketing programs for existing owners and prospective first-time buyers and revenue associated with sales incentives and document compliance. | |

| T-11 | ||||||||||||||||

| HILTON GRAND VACATIONS INC. | ||||||||||||||||

| FINANCING MARGIN DETAIL SCHEDULE | ||||||||||||||||

| (in millions) | ||||||||||||||||

|

Three Months Ended |

Year Ended December 31, | |||||||||||||||

| 2018 | 2017 | 2018 | 2017 | |||||||||||||

| Interest income | $ | 37 | $ | 35 | $ | 140 | $ | 132 | ||||||||

| Other financing revenue | 4 | 3 | 18 | 15 | ||||||||||||

| Financing revenue | 41 | 38 | 158 | 147 | ||||||||||||

| Consumer financing interest expense | 8 | 4 | 24 | 20 | ||||||||||||

| Other financing expense | 6 | 7 | 25 | 23 | ||||||||||||

| Financing expense | 14 | 11 | 49 | 43 | ||||||||||||

| Financing margin | $ | 27 | $ | 27 | $ | 109 | $ | 104 | ||||||||

| Financing margin percentage | 65.9 | % | 71.1 | % | 69.0 | % | 70.7 | % | ||||||||

| T-12 | ||||||||||||||||

| HILTON GRAND VACATIONS INC. | ||||||||||||||||

| RESORT AND CLUB MARGIN DETAIL SCHEDULE | ||||||||||||||||

| (in millions, except for Members and Net Owner Growth) | ||||||||||||||||

|

Three Months Ended |

Year Ended December 31, | |||||||||||||||

| 2018 | 2017 | 2018 | 2017 | |||||||||||||

| Members | 308,637 | 288,391 | ||||||||||||||

| Net Owner Growth (NOG) (1) | 20,246 | 19,272 | ||||||||||||||

| Net Owner Growth % (NOG%) | 7.0 | % | 7.2 | % | ||||||||||||

| Club management revenue | $ | 41 | $ | 36 | $ | 112 | $ | 99 | ||||||||

| Resort management revenue | 15 | 14 | 60 | 59 | ||||||||||||

| Resort and club management revenues | 56 | 50 | 172 | 158 | ||||||||||||

| Club management expense | 10 | 7 | 29 | 25 | ||||||||||||

| Resort management expense | 4 | 4 | 18 | 18 | ||||||||||||

| Resort and club management expenses | 14 | 11 | 47 | 43 | ||||||||||||

| Resort and club management margin | $ | 42 | $ | 39 | $ | 125 | $ | 115 | ||||||||

| Resort and club management margin percentage | 75.0 | % | 78.0 | % | 72.7 | % | 72.8 | % | ||||||||

|

__________________ |

||

| (1) | Net Owner Growth over the last twelve months. | |

| T-13 | ||||||||||||||||

| HILTON GRAND VACATIONS INC. | ||||||||||||||||

| RENTAL AND ANCILLARY MARGIN DETAIL SCHEDULE | ||||||||||||||||

| (in millions) | ||||||||||||||||

|

Three Months Ended |

Year Ended December 31, | |||||||||||||||

| 2018 | 2017 | 2018 | 2017 | |||||||||||||

| Rental revenues | $ | 47 | $ | 36 | $ | 191 | $ | 156 | ||||||||

| Ancillary services revenues | 7 | 5 | 27 | 23 | ||||||||||||

| Rental and ancillary services revenues | 54 | 41 | 218 | 179 | ||||||||||||

| Rental expenses | 32 | 30 | 110 | 103 | ||||||||||||

| Ancillary services expense | 6 | 4 | 23 | 19 | ||||||||||||

| Rental and ancillary services expenses | 38 | 34 | 133 | 122 | ||||||||||||

| Rental and ancillary services margin | $ | 16 | $ | 7 | $ | 85 | $ | 57 | ||||||||

| Rental and ancillary services margin percentage | 29.6 | % | 17.1 | % | 39.0 | % | 31.8 | % | ||||||||

| T-14 | ||||||||||||||||

| HILTON GRAND VACATIONS INC. | ||||||||||||||||

| REAL ESTATE SALES AND FINANCING SEGMENT ADJUSTED EBITDA | ||||||||||||||||

| (in millions) | ||||||||||||||||

| Three Months Ended | Year Ended | |||||||||||||||

| December 31, | December 31, | |||||||||||||||

| 2018 | 2017 | 2018 | 2017 | |||||||||||||

| Sales of VOIs, net | $ | 307 | $ | 142 | $ | 734 | $ | 548 | ||||||||

| Sales, marketing, brand and other fees | 147 | 143 | 570 | 544 | ||||||||||||

| Financing | 41 | 38 | 158 | 147 | ||||||||||||

| Real estate sales and financing segment revenues | 495 | 323 | 1,462 | 1,239 | ||||||||||||

| Cost of VOI sales | (101 | ) | (41 | ) | (210 | ) | (148 | ) | ||||||||

| Sales and marketing | (200 | ) | (171 | ) | (728 | ) | (663 | ) | ||||||||

| Financing | (14 | ) | (11 | ) | (49 | ) | (43 | ) | ||||||||

| Marketing package sales | (7 | ) | (6 | ) | (31 | ) | (29 | ) | ||||||||

| Model unit rental | (1 | ) | — | (1 | ) | (1 | ) | |||||||||

| Share-based compensation | 1 | — | 3 | 2 | ||||||||||||

| Other adjustment items | — | 2 | 1 | 2 | ||||||||||||

| Real estate sales and financing segment Adjusted EBITDA | $ | 173 | $ | 96 | $ | 447 | $ | 359 | ||||||||

| Real estate sales and financing segment Adjusted EBITDA margin percentage | 34.9 | % | 29.7 | % | 30.6 | % | 29.0 | % | ||||||||

| T-15 | ||||||||||||||||

| HILTON GRAND VACATIONS INC. | ||||||||||||||||

| RESORT AND CLUB MANAGEMENT SEGMENT ADJUSTED EBITDA | ||||||||||||||||

| (in millions) | ||||||||||||||||

| Three Months Ended | Year Ended | |||||||||||||||

| December 31, | December 31, | |||||||||||||||

| 2018 | 2017 | 2018 | 2017 | |||||||||||||

| Resort and club management | $ | 56 | $ | 50 | $ | 172 | $ | 158 | ||||||||

| Rental and ancillary services | 54 | 41 | 218 | 179 | ||||||||||||

| Marketing package sales | 7 | 6 | 31 | 29 | ||||||||||||

| Model unit rental | 1 | — | 1 | 1 | ||||||||||||

| Resort and club management segment revenue | 118 | 97 | 422 | 367 | ||||||||||||

| Resort and club management | (14 | ) | (11 | ) | (47 | ) | (43 | ) | ||||||||

| Rental and ancillary services | (38 | ) | (34 | ) | (133 | ) | (122 | ) | ||||||||

| Share-based compensation expense | — | (1 | ) | 2 | 2 | |||||||||||

| Other adjustment items | — | — | 1 | — | ||||||||||||

| Resort and club segment Adjusted EBITDA | $ | 66 | $ | 51 | $ | 245 | $ | 204 | ||||||||

| Resort and club management segment Adjusted EBITDA margin percentage | 55.9 | % | 52.6 | % | 58.1 | % | 55.6 | % | ||||||||

|

Supplemental Information on the Adoption of ASC 606 |

| The following tables provide supplemental information on our consolidated statement of operations, Adjusted EBITDA and real estate margin for the three months and year ended Dec. 31, 2018, compared to the previous accounting guidance. |

| T-16 | ||||||||||||||||

| HILTON GRAND VACATIONS INC. | ||||||||||||||||

| NEW ACCOUNTING STANDARD ADOPTION – EFFECT ON THE THREE MONTHS ENDED DECEMBER 31, 2018 | ||||||||||||||||

| CONSOLIDATED STATEMENTS OF OPERATIONS | ||||||||||||||||

| (in millions, except per share amounts) | ||||||||||||||||

| Three Months Ended December 31, 2018 | ||||||||||||||||

| As Reported |

Effects of |

Previous |

Three |

|||||||||||||

| Revenues | ||||||||||||||||

| Sales of VOIs, net | $ | 307 | $ | (142 | ) | $ | 165 | $ | 142 | |||||||

| Sales, marketing, brand and other fees | 147 | 12 | 159 | 143 | ||||||||||||

| Financing | 41 | — | 41 | 38 | ||||||||||||

| Resort and club management | 56 | 1 | 57 | 50 | ||||||||||||

| Rental and ancillary services | 54 | — | 54 | 41 | ||||||||||||

| Cost reimbursements | 37 | — | 37 | 33 | ||||||||||||

| Total revenues | 642 | (129 | ) | 513 | 447 | |||||||||||

| Expenses | ||||||||||||||||

| Cost of VOI sales | 101 | (46 | ) | 55 | 41 | |||||||||||

| Sales and marketing | 200 | (13 | ) | 187 | 171 | |||||||||||

| Financing | 14 | — | 14 | 11 | ||||||||||||

| Resort and club management | 14 | — | 14 | 11 | ||||||||||||

| Rental and ancillary services | 38 | — | 38 | 34 | ||||||||||||

| General and administrative | 33 | — | 33 | 29 | ||||||||||||

| Depreciation and amortization | 11 | 2 | 13 | 8 | ||||||||||||

| License fee expense | 25 | — | 25 | 22 | ||||||||||||

| Cost reimbursements | 37 | — | 37 | 33 | ||||||||||||

| Total operating expenses | 473 | (57 | ) | 416 | 360 | |||||||||||

| Interest expense | (8 | ) | — | (8 | ) | (6 | ) | |||||||||

| Other loss, net | — | — | — | (1 | ) | |||||||||||

| Income before income taxes | 161 | (72 | ) | 89 | 80 | |||||||||||

| Income tax (expense) benefit | (41 | ) | 18 | (23 | ) | 103 | ||||||||||

| Net income | $ | 120 | $ | (54 | ) | $ | 66 | $ | 183 | |||||||

| Earnings per share: | ||||||||||||||||

| Basic | $ | 1.25 | $ | (0.56 | ) | $ | 0.69 | $ | 1.85 | |||||||

| Diluted | $ | 1.24 | $ | (0.55 | ) | $ | 0.69 | $ | 1.83 | |||||||

| T-17 | ||||||||||||||||||||

| HILTON GRAND VACATIONS INC. | ||||||||||||||||||||

| NEW ACCOUNTING STANDARD ADOPTION – EFFECT ON THE YEAR ENDED DECEMBER 31, 2018 | ||||||||||||||||||||

| CONSOLIDATED STATEMENTS OF OPERATIONS | ||||||||||||||||||||

| (in millions, except per share amounts) | ||||||||||||||||||||

| Year Ended December 31, 2018 | ||||||||||||||||||||

| As Reported |

Effects of ASC 606 |

Previous

Accounting Guidance |

Year Ended December 31, 2017 |

|||||||||||||||||

| Revenues | ||||||||||||||||||||

| Sales of VOIs, net | $ | 734 | $ | (112 | ) | $ | 622 | $ | 548 | |||||||||||

| Sales, marketing, brand and other fees | 570 | 16 | 586 | 544 | ||||||||||||||||

| Financing | 158 | — | 158 | 147 | ||||||||||||||||

| Resort and club management | 172 | 1 | 173 | 158 | ||||||||||||||||

| Rental and ancillary services | 218 | — | 218 | 179 | ||||||||||||||||

| Cost reimbursements | 147 | — | 147 | 135 | ||||||||||||||||

| Total revenues | 1,999 | (95 | ) | 1,904 | 1,711 | |||||||||||||||

| Expenses | ||||||||||||||||||||

| Cost of VOI sales | 210 | (30 | ) | 180 | 148 | |||||||||||||||

| Sales and marketing | 728 | 1 | 729 | 663 | ||||||||||||||||

| Financing | 49 | — | 49 | 43 | ||||||||||||||||

| Resort and club management | 47 | — | 47 | 43 | ||||||||||||||||

| Rental and ancillary services | 133 | — | 133 | 122 | ||||||||||||||||

| General and administrative | 117 | — | 117 | 104 | ||||||||||||||||

| Depreciation and amortization | 36 | 2 | 38 | 29 | ||||||||||||||||

| License fee expense | 98 | — | 98 | 87 | ||||||||||||||||

| Cost reimbursements | 147 | — | 147 | 135 | ||||||||||||||||

| Total operating expenses | 1,565 | (27 | ) | 1,538 | 1,374 | |||||||||||||||

| Interest expense | (30 | ) | — | (30 | ) | (27 | ) | |||||||||||||

| Equity in earnings from unconsolidated affiliates | — | — | — | 1 | ||||||||||||||||

| Other loss, net | (1 | ) | — | (1 | ) | — | ||||||||||||||

| Income before income taxes | 403 | (68 | ) | 335 | 311 | |||||||||||||||

| Income tax (expense) benefit | (105 | ) | 17 | (88 | ) | 16 | ||||||||||||||

| Net income | $ | 298 | $ | (51 | ) | $ | 247 | $ | 327 | |||||||||||

| Earnings per share: | ||||||||||||||||||||

| Basic | $ | 3.07 | $ | (0.53 | ) | $ | 2.54 | $ | 3.30 | |||||||||||

| Diluted | $ | 3.05 | $ | (0.53 | ) | $ | 2.52 | $ | 3.28 | |||||||||||

| T-18 | ||||||||||||||||||||

| HILTON GRAND VACATIONS INC. | ||||||||||||||||||||

| NEW ACCOUNTING STANDARD ADOPTION – EFFECT ON THE THREE MONTHS ENDED DECEMBER 31, 2018 | ||||||||||||||||||||

| SEGMENT EBITDA AND ADJUSTED EBITDA TO NET INCOME | ||||||||||||||||||||

| (in millions) | ||||||||||||||||||||

| Three Months Ended December 31, 2018 | ||||||||||||||||||||

| As Reported |

Effects of ASC 606 |

Previous Accounting Guidance |

Three Months Ended December 31, 2017 |

|||||||||||||||||

| Net Income | $ | 120 | $ | (54 | ) | $ | 66 | $ | 183 | |||||||||||

| Interest expense | 8 | — | 8 | 6 | ||||||||||||||||

| Income tax expense (benefit) | 41 | (18 | ) | 23 | (103 | ) | ||||||||||||||

| Depreciation and amortization | 11 | 2 | 13 | 8 | ||||||||||||||||

|

Interest expense, depreciation and amortization included in equity from unconsolidated affiliates |

1 | — | 1 | 1 | ||||||||||||||||

| EBITDA | 181 | (70 | ) | 111 | 95 | |||||||||||||||

| Other loss, net | — | — | — | 1 | ||||||||||||||||

| Share-based compensation expense | 3 | — | 3 | 2 | ||||||||||||||||

| Other adjustment items (1) | 2 | (2 | ) | — | 3 | |||||||||||||||

| Adjusted EBITDA | $ | 186 | $ | (72 | ) | $ | 114 | $ | 101 | |||||||||||

| Adjusted EBITDA: | ||||||||||||||||||||

| Real estate sales and financing (2) | $ | 173 | $ | (72 | ) | $ | 101 | $ | 96 | |||||||||||

| Resort operations and club management (2) | 66 | — | 66 | 51 | ||||||||||||||||

| Segment Adjusted EBITDA | 239 | (72 | ) | 167 | 147 | |||||||||||||||

| Adjustments: | ||||||||||||||||||||

| Adjusted EBITDA from unconsolidated affiliates | 1 | — | 1 | 1 | ||||||||||||||||

| License fee expense | (25 | ) | — | (25 | ) | (22 | ) | |||||||||||||

| General and administrative (3) | (29 | ) | — | (29 | ) | (25 | ) | |||||||||||||

| Adjusted EBITDA | $ | 186 | $ | (72 | ) | $ | 114 | $ | 101 | |||||||||||

| Adjusted EBITDA margin % | 29.0 | % | 55.8 | % | 22.2 | % | 22.6 | % | ||||||||||||

| EBITDA margin % | 28.2 |

% |

54.3 | % | 21.6 | % | 21.3 | % | ||||||||||||

| _____________________ | ||

|

(1) |

For three months ended Dec. 31, 2018 and 2017, amounts include $2 million and $3 million, respectively, of costs associated with the spin-off transaction. | |

|

(2) |

Includes intersegment eliminations, share-based compensation attributable to the segment and other adjustments. | |

|

(3) |

Excludes share-based compensation and other adjustment items. | |

| T-19 | ||||||||||||||||||||

| HILTON GRAND VACATIONS INC. | ||||||||||||||||||||

| NEW ACCOUNTING STANDARD ADOPTION – EFFECT ON THE YEAR ENDED DECEMBER 31, 2018 | ||||||||||||||||||||

| SEGMENT EBITDA AND ADJUSTED EBITDA TO NET INCOME | ||||||||||||||||||||

| (in millions) | ||||||||||||||||||||

| Year Ended December 31, 2018 | ||||||||||||||||||||

| As Reported |

Effects of ASC 606 |

Previous Accounting Guidance |

Year Ended December 31, 2017 |

|||||||||||||||||

| Net Income | $ | 298 | $ | (51 | ) | $ | 247 | $ | 327 | |||||||||||

| Interest expense | 30 | — | 30 | 27 | ||||||||||||||||

| Income tax expense (benefit) | 105 | (17 | ) | 88 | (16 | ) | ||||||||||||||

| Depreciation and amortization | 36 | 2 | 38 | 29 | ||||||||||||||||

|

Interest expense, depreciation and amortization included in equity in losses from unconsolidated affiliates |

4 | — | 4 | 3 | ||||||||||||||||

| EBITDA | 473 | (66 | ) | 407 | 370 | |||||||||||||||

| Other loss, net | 1 | — | 1 | — | ||||||||||||||||

| Share-based compensation expense | 16 | — | 16 | 15 | ||||||||||||||||

| Other adjustment items (1) | 13 | (2 | ) | 11 | 10 | |||||||||||||||

| Adjusted EBITDA | $ | 503 | $ | (68 | ) | $ | 435 | $ | 395 | |||||||||||

| Adjusted EBITDA: | ||||||||||||||||||||

| Real estate sales and financing (2) | $ | 447 | $ | (68 | ) | $ | 379 | $ | 359 | |||||||||||

| Resort operations and club management (2) | 245 | — | 245 | 204 | ||||||||||||||||

| Segment Adjusted EBITDA | 692 | (68 | ) | 624 | 563 | |||||||||||||||

| Adjustments: | ||||||||||||||||||||

| Adjusted EBITDA from unconsolidated affiliates | 4 | — | 4 | 4 | ||||||||||||||||

| License fee expense | (98 | ) | — | (98 | ) | (87 | ) | |||||||||||||

| General and administrative (3) | (95 | ) | — | (95 | ) | (85 | ) | |||||||||||||

| Adjusted EBITDA | $ | 503 | $ | (68 | ) | $ | 435 | $ | 395 | |||||||||||

| Adjusted EBITDA margin % | 25.2 | % | 71.6 | % | 22.8 | % | 23.1 | % | ||||||||||||

| EBITDA margin % | 23.7 | % | 69.5 | % | 21.4 | % | 21.6 | % | ||||||||||||

| _____________________ | ||

|

(1) |

For the years ended Dec. 31, 2018 and 2017, amounts include $11 million and $8 million, respectively, of costs associated with the spin-off transaction. | |

|

(2) |

Includes intersegment eliminations, share-based compensation attributable to the segment and other adjustments. | |

|

(3) |

Excludes share-based compensation and other adjustment items. | |

| T-20 | ||||||||||||||||||||

| HILTON GRAND VACATIONS INC. | ||||||||||||||||||||

| NEW ACCOUNTING STANDARD ADOPTION – EFFECT ON THE THREE MONTHS ENDED DECEMBER 31, 2018 | ||||||||||||||||||||

| REAL ESTATE MARGIN | ||||||||||||||||||||

| (in millions) | ||||||||||||||||||||

| Three Months Ended December 31, 2018 | ||||||||||||||||||||

| As Reported |

Effect of

ASC 606 |

Previous Accounting Guidance |

Three Months Ended December 31, 2017 |

|||||||||||||||||

| Sales of VOIs, net | $ | 307 | $ | (142 | ) | $ | 165 | $ | 142 | |||||||||||

| Sales, marketing, brand and other fees | 147 | 12 | 159 | 143 | ||||||||||||||||

| Less: | ||||||||||||||||||||

| Marketing revenue and other fees | 32 | 7 | 39 | 36 | ||||||||||||||||

| Sales revenue | 422 | (137 | ) | 285 | 249 | |||||||||||||||

| Less: | ||||||||||||||||||||

| Cost of VOI sales | 101 | (46 | ) | 55 | 41 | |||||||||||||||

| Sales and marketing expense, net | 162 | (20 | ) | 142 | 128 | |||||||||||||||

| Real estate margin | $ | 159 | $ | (71 | ) | $ | 88 | $ | 80 | |||||||||||

| Real estate margin percentage | 37.7 | % | 51.8 | % | 30.9 | % | 32.1 | % | ||||||||||||

| T-21 | ||||||||||||||||||||

| HILTON GRAND VACATIONS INC. | ||||||||||||||||||||

| NEW ACCOUNTING STANDARD ADOPTION – EFFECT ON THE YEAR ENDED DECEMBER 31, 2018 | ||||||||||||||||||||

| REAL ESTATE MARGIN | ||||||||||||||||||||

| (in millions) | ||||||||||||||||||||

| Year Ended December 31, 2018 | ||||||||||||||||||||

| As Reported |

Effect of

ASC 606 |

Previous Accounting Guidance |

Year Ended December 31, 2017 |

|||||||||||||||||

| Sales of VOIs, net | $ | 734 | $ | (112 | ) | $ | 622 | $ | 548 | |||||||||||

| Sales, marketing, brand and other fees | 570 | 16 | 586 | 544 | ||||||||||||||||

| Less: | ||||||||||||||||||||

| Marketing revenue and other fees | 123 | 16 | 139 | 145 | ||||||||||||||||

| Sales revenue | 1,181 | (112 | ) | 1,069 | 947 | |||||||||||||||

| Less: | ||||||||||||||||||||

| Cost of VOI sales | 210 | (30 | ) | 180 | 148 | |||||||||||||||

| Sales and marketing expense, net | 575 | (15 | ) | 560 | 492 | |||||||||||||||

| Real estate margin | $ | 396 | $ | (67 | ) | $ | 329 | $ | 307 | |||||||||||

| Real estate margin percentage | 33.5 | % | 59.8 | % | 30.8 | % | 32.4 | % | ||||||||||||

| T-22 | ||||||||||

| HILTON GRAND VACATIONS INC. | ||||||||||

| FORWARD-YEAR ADJUSTED EBITDA RECONCILIATION | ||||||||||

| (in millions, except share data) | ||||||||||

|

2019(1)

Low Case |

2019(1)

High Case |

|||||||||

| Contract Sales | 9.0 | % | 11.0 | % | ||||||

| Fee-for-service as % of contract sales | 48 | % | 54 | % | ||||||

| Net Income | $ | 260 | $ | 275 | ||||||

| Income tax expense | 97 | 103 | ||||||||

| Pre-tax income | 357 | 378 | ||||||||

| Interest expense | 30 | 27 | ||||||||

| Depreciation and amortization | 42 | 39 | ||||||||

|

Interest expense and depreciation and amortization included in equity in earnings from unconsolidated affiliates |

1 | 2 | ||||||||

| EBITDA | 430 | 446 | ||||||||

| Share-based compensation expense | 18 | 20 | ||||||||

| Other adjustment items | 2 | 4 | ||||||||

| Adjusted EBITDA | $ | 450 | $ | 470 | ||||||

| Diluted shares | 95 | 95 | ||||||||

| Earnings per share - diluted | $ | 2.74 | $ | 2.89 | ||||||

| Cash flow from operating activities | $ | 75 | $ | 115 | ||||||

| Non-inventory capex | (60 | ) | (50 | ) | ||||||

| Free Cash Flow | 15 | 65 | ||||||||

| Net proceeds from securitization activity | 45 | 55 | ||||||||

| Adjusted Free Cash Flow | $ | 60 | $ | 120 | ||||||

| _____________________ | ||

|

(1) |

2019 Guidance assumes no full-year impact from construction-related revenues or expenses deferrals. | |