")

SAN FRANCISCO--(BUSINESS WIRE)--Voce Capital Management LLC (“Voce”), the beneficial owner of approximately 5.8% of the shares of Argo Group International Holdings, Ltd. (NYSE:ARGO) (“Argo” or the “Company”), today announced that it has nominated four highly-qualified, independent candidates for election to the Board of Directors at the Company’s 2019 Annual Meeting.

Voce issued the following letter to Argo stockholders in connection with the nominations:

February 25, 2019

Dear Fellow Shareholders of Argo Group International Holdings, Ltd.:

Voce Capital Management LLC (“Voce”) is the beneficial owner of more than 1.9 million shares of Argo Group International Holdings, Ltd. (NYSE: ARGO) (“Argo” or the “Company”), representing approximately 5.8% of its shares outstanding and making us the Company’s fourth-largest shareholder.

We have spent a year researching and analyzing Argo. This has included meetings with the Company, fellow shareholders, members of the investment community as well as many leaders within the specialty insurance industry. We’ve compared Argo’s performance, over more than a decade, with its peers and against its own stated goals. Based on our analysis, we strongly believe the following:

- The only pathway for Argo to create sustainable, long-term shareholder value is through a dramatic improvement in its return on equity (“ROE”);

- Argo will never be able to meaningfully enhance its ROE with its current strategy and expense structure;

- Argo’s corporate expenses are not only shockingly high – they are also shockingly inappropriate, including extravagant perquisites, personal use of corporate property such as Company-owned aircraft and housing, gross misallocations of capital on wasteful items and frivolous vanity sponsorships, and an overall spendthrift culture that misdirects Company assets to support the lifestyle and hobbies of the Company’s CEO at the expense of shareholders;

- As a result of its lack of independence, dearth of relevant experience and misalignment with shareholders, Argo’s Board of Directors (the “Board”) is directly responsible for this waste of corporate assets and must be held accountable for it; and

- Voce is committed to pursuing changes at Argo that will maximize value for all shareholders, starting with the nomination today of four highly-qualified, independent Director candidates.

Argo’s White Whale

The ultimate measure of any company’s financial success is the return it generates on the capital that shareholders have entrusted to it. ROE is also the single most predicative determinant of how public insurance companies are valued, as the market assigns a premium (or discount) to shareholders’ equity to arrive at a stock price. Unlike other industries that incorporate a wide variety of valuation techniques, such as multiples of revenues or EBITDA and discounted cash flow analyses, insurance companies are almost exclusively valued simply as a multiple of book value. Price-to-book, or P/BV as it’s known, is how this is expressed. As one would expect, companies with a higher ROE tend to garner a higher P/BV multiple.

Argo trades at a significant P/BV discount to its key peers. Argo’s current multiple of P/BV is approximately 1.3x, compared to its group of self-selected “proxy peers,” which trade at an average of 2.0x P/BV. This isn’t an anomaly, as Argo has long traded at a valuation discount to this group precisely because its profitability, and therefore its ROE, has usually been comparatively, and unacceptably, low.

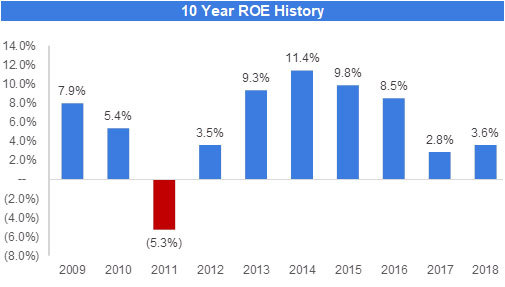

For more than a decade, Argo has talked about its desire to enhance its ROE, but has very little to show for it. Argo’s 2018 ROE was a dismal 3.6%. As seen in Figure 1, Argo has only posted a double-digit ROE once in the past decade.

Over that period, Argo has averaged an ROE of less than 6%. At these levels, Argo does not even cover its cost of capital. Argo also trails its peers significantly, which have averaged an ROE of almost 11%.

While Argo has offered endless ROE excuses – ranging from interest rates to its business mix – and has shifted the goalposts many times, the cold hard truth is that over a very long period of time it has come up woefully short on the most important benchmark. Moreover, the various initiatives it has promoted to remediate this, such as whittling its expenses (the same thing it says it plans to do now), have failed to materialize. Its peers, who face the same industry headwinds, have fared much better than Argo through superior operational discipline, which is why so many of them trade at higher P/BV multiples.

Can’t Get There from Here

The best insurance operators have the highest ROEs for a simple reason: All other things equal, the lower the expenses the better the underwriting results and therefore the higher the profits. Argo’s costs to acquire premium (essentially the commissions it pays to the brokers who bring clients to Argo) reflect industry norms and offer little opportunity for savings. Its loss experience is competitive, demonstrating solid risk selection, pricing and reserve development. This is what makes Argo’s core property and casualty business, particularly in the U.S., such an attractive asset. Where Argo falls significantly short is in the “Other Underwriting Expense” (“OUE”) category, where all other operating and corporate expenses reside. Again, using Argo’s proxy peers, its OUE is almost 350 basis points worse than these peers over the past 10 years. What’s so disappointing about Argo’s long-term struggles in this area is that expenses are much more controllable by management than insured claims.

Why then has Argo been unable to tackle its expenses in a meaningful way? Why is its OUE consistently such an outlier? After a little sleuthing, it turns out the answer is, well, elementary. On the LinkedIn page of Argo’s CEO, Mark E. Watson III, his first post reads: “My son once asked me: ‘What do you really do? Because I don’t think I get it. My sisters tell me all you do is talk to people all day long.’” We’ve got the same question, actually.

Mr. Watson’s ubiquitous online and social media presence provides some insight into his motivations and aspirations, as well as how and where he spends his time. His tastes in art, architecture, racing, yachting and luxury travel, among other things, are well documented, and he appears to be quite the bon vivant. We in no way begrudge Mr. Watson, or any executive, the right to allocate his personal time or money in pursuit of private passions. But we’re deeply concerned that Mr. Watson’s hobbies, pet projects and the cult of personality he apparently wishes to create for himself have commandeered and corrupted Argo’s priorities. We believe that Argo’s corporate assets – including Mr. Watson’s professional time, the Company’s focus and its capital – are being grossly misspent and misdirected, in furtherance of Mr. Watson’s personal agenda at shareholders’ expense.

Edifice Complex

Mr. Watson’s penchant for dramatic and expensive real estate has cost shareholders dearly. According to reports, when Argo renovated its San Antonio office space, formerly the headquarters for behemoth AT&T, Mr. Watson was “the design-conscious maestro” who oversaw every detail of the project.1 He viewed it as “a ‘blank canvas’” to showcase his creativity and display the corporate art collection acquired at his behest. “I think it reflects who we are,” Mr. Watson boasted.2 Argo’s website (and YouTube channel) are home to scores of professionally produced, slick videos showcasing Mr. Watson’s many passions, including a series called “On the Ground” trumpeting the cushy digs and prestigious office locations that Argo occupies around the world. From “San Antonio,” one of the executives says on camera “if you think about some of the neat things about the San Antonio office it is the array of artwork that we have in the office.” Another staffer chimes in, “there’s so much artwork, and there’s so much beauty about how our office is constructed.”

Why does a small company like Argo even have an art collection? Wouldn’t prints from www.art.com cover the walls just as well? Here we begin to see how Mr. Watson’s personal aspirations seem to have set Argo’s corporate agenda. According to media reports, Mr. Watson curates the Argo art collection himself and makes dedicated journeys out-of-state to acquire new pieces.3 Is this how the CEO of a small public company should be spending his time or shareholder resources?

In New York City, Argo recently constructed a multi-level facility in a historical building in downtown Manhattan’s “Meatpacking” district, amid some of the world’s most expensive retail space. According to another “On the Ground” feature in Argo’s video oeuvre, the NYC headquarters are “really kinda nestled in this cool neighborhood of technology and art and food.” One of the employees who works there adds, “It’s a really interesting and trendy place, especially for an insurance company.” Yes it is. “‘Argo was one that shocked the market,’ said Paul Amrich, vice chairman of real-estate services firm CBRE Group Inc., and part of the team representing the building owners in the Argo deal. ‘They were like, “Wait, insurance in the Meatpacking District?”’”4 In order to count as its neighbors some of the most chic luxury brands in the world, Argo is paying $100 per square foot for the 48,000 square foot facility, serving as the anchor tenant and committing to a 15-year lease.5 The Company even lobbied the NYC Landmarks Preservation Commission to slap the Argo logo on the building’s roof.

Once again, Mr. Watson appears to have squandered not only a significant amount of shareholder capital but his own valuable time as CEO on this folly. The head of the architecture firm that assisted Mr. Watson in creating his NYC masterpiece had this to say: “Argo executives could’ve just renewed their lease and taken another 10,000 square feet down the block. But Mark’s not about the safe bet.” Certainly not when he’s betting with shareholders’ money. According to Interior Design magazine, Mr. Watson was once again “intimately involved in the office’s design from before the space even had functional floors.”6 As the lead designer, Mr. Watson appears to have not overlooked a single detail, such as “mobile ottomans, generous armchairs, and golden drum tables, and simple circular pendant fixtures [which] bring to mind a more perfect version of the warm halo of streetlights”; special “LED downlights that cast a soft brightness . . . more often used in museums on ancient texts”; and designer furniture, such as Arne Jacobsen Swan chairs, Isamu Noguchi tables and “a commodious gray sectional sofa by Francesco Rota and enveloping Hayon Studio lounge chairs, some upholstered in an Argo-blue polyester. . . .” Mr. Watson should have higher priorities for his time and attention.

Across the pond, Argo occupies 33,000 square feet of premium office space (with its own private entrance) at One Fen Court, in pricey Central London just down the street from Lloyd’s. Its neighbors are much larger, global insurance entities such as Willis, Swiss Re, Standard Life, Aon and Tokio Marine, to name a few, that cater to the types of clientele who might actually notice or care where their insurer is located. Incredibly, Mr. Watson continues to complain of the low returns available from underwriting in London while at the same time sinking enormous sums of shareholder capital into ostentatious quarters there.

Man Overboard

Mr. Watson’s passion for yachting and racing is legendary. On his personal website, www.mewiii.com, for example, he rhapsodizes himself as “a sailor, runner, climber and car racing enthusiast.” Is it just a coincidence that Argo’s corporate identity and sponsorship dollars are all directed to the same activities?7 For example, Argo paid to sponsor the Vestas 11th Hour Racing team in a 45,000 nautical mile global boat race. As that event describes itself, “the Volvo Ocean Race is an obsession, and many of the world's best sailors have dedicated years, even decades of their lives trying to win it. . . . Over four decades it has kept an almost mythical hold” over many sailors.8 Apparently so. After having Argo endow the Vestas boat and crew, Mr. Watson himself flew to Spain to participate in the race onboard the boat with the crew. Argo also bankrolled the Swedish Artemis Racing team’s entry into the America’s Cup. And every year, Argo is the title sponsor for the Argo Gold Cup, a sailing match at the posh Royal Bermuda Yacht Club, where Mr. Watson is a member (no Company disclosure exists as to who pays the membership dues). Argo also funds a Formula E race car team, GEOX DRAGON; in December 2018, Argo agreed to a multi-year extension of the race car sponsorship.9 Just within the past year, Mr. Watson personally attended the team’s races in Mexico City (February 16, 2019), Marrakesh (January 12, 2019), New York City (July 14, 2018) and Rome (April 14, 2018) to cheer them on (and pose for pictures with the team and then tweet about his participation).

The Company’s efforts to rationalize these expenditures of shareholder capital are laughable.10 Exotic race cars and yachts have nothing to do with the rather humdrum business of selling insurance to small and midsize companies. In response to our requests, Argo has refused to provide any details on the cost of these endorsements, nor has it been willing to quantify their value. However, there’s one clear beneficiary of Argo’s magnanimity: Mr. Watson, who splashes himself prominently all over the media related to these promotions. He’s personally quoted in nearly every press release, and the recipients of this largesse often credit “Mark” for his vision and generosity. Despite being ostensibly a corporate marketing opportunity, rarely are other Argo executives featured. It’s seemingly all about Mr. Watson, as he routinely inserts himself into the events as a player rather than a corporate sponsor, donning the gear, boarding the boats and jumping into the pit. He shamelessly mugs for all manner of cringe-worthy photo-ops while basking in the glow of the individual attention these shareholder-financed subsidies bring to him personally.

The Company’s charitable activities also seem to dovetail with Mr. Watson’s personal passions. There are more donations to sailing groups than we can count, such as Endeavour Community Sailing and the Bermuda Sloop Foundation.11 Or consider the Andrew Simpson Sailing Foundation (“ASSF”), whose mission is to “give thousands of young people the chance to enjoy the life-changing challenges of sailing”; after getting Argo to sponsor it, Mr. Watson made a personal appearance in Toulon, France to host “a group of local youth sailors” for an ASSF event, and get his picture taken with them aboard Artemis’ racing boat (which Argo also pays for).12 He made a trip to New York City ostensibly to bestow a small prize to a group of “local high school robotics teams” in Brooklyn; but just coincidentally got to attend the ePrix race while there. (Ironically, the $10,000 check he handed out to the kids was less than half of the corporate expense incurred in flying Mr. Watson to the event.) We question the wisdom of Mr. Watson’s penchant for personally attending all manner of charitable events, no matter how modest in scale or importance, allocating valuable CEO time in the endless pursuit of adulation and fodder for his Twitter feed.

And in a similar vein, Mr. Watson’s taste in expensive art has naturally become Argo’s, too. Mr. Watson is a Trustee of the San Antonio Museum of Art, but Argo’s generous corporate gifts to the museum have exceeded his meager personal donations in some years by a ratio as large as 25:1.13

Oh! What a Tangled Web We Weave…

Mr. Watson’s personal website, www.mewiii.com, is also rather revealing and provides further confirmation that there is no demarcation between Mr. Watson’s personal activities and those he directs Argo to do. The website is basically one gigantic self-paean – “Entrepreneur, Competitor and Philanthropist,” as he describes himself and organizes the content – with glossy pics of him in action, hamming it up as the center of attention at various Argo-funded events, just as he does on Argo’s official website. Argo’s corporate logos and property are everywhere on his personal website, because virtually all of the activities featured there appear to be funded or paid for by the Company. Take philanthropy, for example. Upon close inspection, one will recognize the photos – they’re nearly all drawn from Argo’s corporate website. The charities listed on his personal “Philanthropist” page are actually recipients of Argo funding, despite Mr. Watson taking personal credit for it.

Perhaps most disturbing, on the “contact” page of Mr. Watson’s personal website, visitors who have “a question or want to schedule an interview with Mark” are directed to “contact David Snowden at david.snowden@argogroupus.com.” Mr. Snowden is Argo’s Senior Vice President of Corporate Communications, not Mr. Watson’s personal publicist. Mr. Watson also has a companion site, www.mewiii.net, which was registered on the same date – February 8, 2010. Despite being his personal websites, both domains are owned by Argo, and identify an Argo employee who is a web developer at the Company, as the keeper of the sites. How many more Argo employees spend some or all of their time supporting Mr. Watson’s personal image and brand, including his personal websites, hyperactive Twitter feed, detailed LinkedIn posts (e.g., “Books That Inspire Me: Volumes 1-5”) and producing the extensive library of video interviews of him on the corporate website and YouTube channel?

Using corporate employees and resources to conduct personal business is a violation of law, NYSE regulations and Argo’s own Code of Conduct & Business Ethics. The latter, which ironically tasks Mr. Watson himself with principal responsibility for implementing and executing the Code, speaks directly to our concerns. For example: “Key functionaries and employees shall protect the Company’s assets and ensure their efficient use. Theft, carelessness, and waste have a direct impact on the Company’s profitability. All Company assets are to be used for legitimate Company purposes.” And more broadly: “A ‘conflict of interest’ exists when a person’s private interest in any way interferes, (or might appear to interfere), with the business interests of the Company, its shareholders and its policyholders. . . . Conflicts of interest may also arise when a key functionary or employee, or a member of his or her family, receives improper personal benefits as a result of his or her position in the Company or any of its affiliates. . . .”

Housing Project

Despite paying him several million dollars per year, Argo’s shareholders have long borne Mr. Watson’s personal living expenses, particularly his housing. In 2007, after Argo bought Bermuda-based PXRE and re-domiciled there, Mr. Watson was granted a $1,5000,000 “relocation” allowance and an additional $1,400,000 bonus for his “agreement to Argo Group’s request that he and his family move to Bermuda.”14 Shareholders could have reasonably expected that after a $2,900,000 relocation payment Mr. Watson could have covered his own nut in Bermuda.

Yet in his 2007 Employment Agreement, the Board inexplicably gave him an additional $360,000 annual housing allowance and a $40,000 “home leave allowance”; including the tax “gross up” payment he was also given for these benefits, the total came to $574,676 in 2008 (and $681,598 in 2009 and $653,326 in 2010). That’s right: The same Agreement with the $2,900,000 windfall granted him well more than half a million dollars in additional housing benefits each year – on top of his $1,000,000 base salary and a whole suite of other benefits and perquisites. While his Bermuda housing and travel benefits have bounced around, they’ve averaged $268,902 per year over the past decade. He mysteriously continues to receive these gratuitous benefits despite the fact that his current Employment Agreement (November 2018) no longer provides for them.15

What are these princely Bermuda housing payments possibly for? We’ve discovered that Argo has a long-term lease on “The Jungle,” a 1.7 acre waterfront compound and villa that serves as Mr. Watson’s private home when he’s in Bermuda. Local real estate agents describe The Jungle as an “ultra-exclusive” and “exquisite property and magnificent house” with a swimming pool, lush grounds and a private boat dock. It’s in the tony Tucker’s Town enclave in St. George’s Parish, Bermuda, where Mr. Watson lives next door to billionaire Michael Bloomberg (his other neighbors include Silvio Berlusconi and H. Ross Perot).16

Mr. Watson also receives a similar benefit for “unreimbursed personal use of corporate housing in New York,” on top of the aforementioned housing and travel benefits, to the tune of $60,000 in 2017. As noted earlier, despite the fact that Argo refers to its New York City headquarters as an office, one thing it doesn’t mention is the 2,800 square foot glass penthouse apartment it constructed as part of the renovation and which we believe Mr. Watson lives in when he’s in town.17 While it appears that Mr. Watson is having small amounts of income imputed to him from his exclusive use of these corporate owned homes, the larger questions remain: Why are Argo shareholders footing the bill for any of the CEO’s living expenses? Who accepted responsibility on the Company’s behalf to provide Mr. Watson with private homes around the world in the first place? How is it an appropriate allocation of shareholder capital for Argo to own or lease such lavish properties, which presumably sit empty on many days when Mr. Watson is not in residence?

The Mile-High Club

The “corporate aircraft program,” as it is obliquely described in the sole reference to it in Argo’s public filings, is perhaps the most egregious example of the misuse of corporate assets. For a relatively small company, Argo has a fleet of three corporate jets. It has fractional ownership of two corporate planes, one of which is a Bombardier Global 5000, which can seat up to 16 passengers in three cabins, has a galley large enough to prepare five-course meals and can fly between any two points on the globe with a maximum of one stop. The second jet is a rather modest plane (by Argo standards) which seats only 10.18 Yet Argo also owns a Gulfstream V aircraft. Shareholders can be forgiven for not being aware of the existence of the Gulfstream jet, since Argo has allowed a private company to purchase it, under a different name, while nonetheless making it available to Argo on an exclusive basis (i.e., it is not fractional ownership but rather is only flown by Argo). Despite being a substantial off-balance sheet liability, Argo has never disclosed any details of its corporate aircraft program, including the terms of the various leases, in its SEC filings.

A “G-5,” as this particular Gulfstream model is known to the cognoscenti, is one of the most luxurious and prestigious status symbols among the global jet set. It typically requires four crew members to operate (two pilots and two flight attendants) and can seat up to 19 passengers (and sleep up to 8). There’s simply no justification for this extravagance. Argo operates in major business and financial hubs – such as New York, London, Dubai, Sao Paolo, Singapore and Bermuda – that are well-served by abundant commercial travel options. And even if there were occasional trips requiring teams of executives to travel together or at odd hours, surely one of the two fractional jet programs that Argo purchases would be more than adequate.

In one interview, Mr. Watson said: “People often ask: ‘Where do you spend most of your time?’ My short answer is, ‘In the air.’”19 Er, roger that. Based on publicly-available flight logs, the G-5 is in constant motion, crisscrossing the globe at a dizzying pace. Over the past three calendar years alone, the G-5 has logged more than 584 flights and 1,484 hours of flight time. That’s an average of 195 flights per year – a staggering tally considering there are approximately 250 business days per year. Based on this usage, we estimate the variable annual operating costs of the G-5 alone are as high as $2,100,000.20 In addition, the fixed costs to maintain a crew and aircraft of this type (including hangar, insurance, depreciation, training and other miscellaneous expenses) are estimated to exceed $600,000 per year, bringing the total cost of Argo’s G-5 to almost $3,000,000 per year.

Even if Argo’s G-5 were being used exclusively for business purposes, the expense for a company of Argos’ size to carry such an aircraft would be completely unjustified. But unfortunately, Argo’s G-5 is not just being used for business purposes. We believe the G-5 is Mr. Watson’s personal chariot, whisking him and his entourage around the world in pursuit of his kaleidoscope of hobbies and interests, which sometimes includes Argo business, but often doesn’t. For example, over the past three years alone, the G-5:

- Has traveled to or from North Kingstown, Rhode Island 56 times and to or from Providence, Rhode Island an additional 18 times; these airports serve nearby Newport, where Mr. Watson has a home and an active community and social presence, making these 74 flights personal commuting expenses (according to his most-recent Employment Agreement, Mr. Watson’s principal place of business with the company is Bermuda);21

- Shuttled him from San Antonio (where he also resides, despite having been paid to relocate to Bermuda) to Bermuda and then returned him home to San Antonio 37 times (these would also be personal commuting expenses for the same reason);

- Frequently ferries him to luxury or vacation destinations in the Mediterranean (Toulon and Sardinia), the Caribbean (Jamaica, The Bahamas, Anguilla, St. Maarten, Marco Island), Mexico (Ixtapa, Merida and 6 trips to Puerto Vallarta), skiing (5 trips to Aspen), Santa Barbara and Sonoma, and other sybaritic destinations;

- Chauffeured him to France 11 times, which Mr. Watson seems particularly fond of, despite Argo’s miniscule business there, as he’s visited Paris, Provence, Saint-Malo and other destinations (and this total excludes the annual Nice-Monte Carlo industry conference);

- Conveyed him from San Antonio to the Art Basel Expo in Miami Beach from November 29-December 2, 2016, and then back home to San Antonio afterwards;22

- Dropped him at the various sporting events around the world that Argo sponsors, where he typically will participate, pose for pictures with the players and then populate his Twitter feed and personal website; and

- Schlepped him to South Florida 23 times, mostly to Miami and surrounding areas, where his 52-foot yacht, “Spookie,” is harbored and frequently races.

Bear in mind: The foregoing is just a three-year summary for one of Argo’s three private jets.

It also appears that the Watsons owe the G-5 – and Argo shareholders – a big “thank you” for making possible some fantastic family travel experiences. For example, during the 2017 Christmas holidays, the G-5 took the entire family to India on what most ordinary people would consider the trip of a lifetime. Their journey began in San Antonio on December 14, 2017. After stopping in Bermuda and New York City, the G-5 headed to Copenhagen for the weekend. From Denmark it flew to the exotic Malabar Coast of India. They arrived in Kerala on Monday, December 18, spending three days there until the G-5 took them to Udaipur where they remained until Christmas Eve. While in Udaipur they had the “great honor to visit the Shambhu Niwas Palace,” according to Mr. Watson’s tweet, where they were hosted by the custodian of the ancient house of Mewar, Arvind Singh Mewar. (They likely hit it off famously, as Mr. Mewar is renowned for his love of patrician pastimes and private planes.) The Watson clan then journeyed on to Jaipur in Northern India, until December 31, when they departed for Amsterdam. After ringing in the New Year there, they began winging their way back to San Antonio on Wednesday, January 3, 2018.

San Antonio, We Have a Problem

There are a multitude of securities, tax and other rules and regulations governing compensation and benefits, especially executive use of corporate air travel. They are stringent and clear, and the consequences for violating them are severe.

The SEC has detailed disclosure requirements around executive perquisites, given the potential for abuse. Regulation S-K requires disclosure of executive perquisites and benefits that exceed $10,000 in aggregate, and personal use of Company aircraft is explicitly defined as a perquisite within the category of “other compensation” that must be disclosed.23 Argo appears to understand this, because it discloses many of Mr. Watson’s other benefits, such as his life insurance, financial planning and various housing allowances. Yet its treatment of his personal air travel, and its questionable disclosures around it, raises a host of extremely serious issues. For starters, Argo’s policy of not charging employees anything when family members travel with them – not even the Standard Industry Fare Level rates set by the Department of Transportation – is out of step with best practices and is especially concerning given the frequency of Mr. Watson’s travel, including internationally, with family members in tow.

Moreover, Argo has never disclosed any reimbursement by Mr. Watson to the Company for personal use of the G-5 nor imputed any income to him for it. We invite Argo to explain if it considers Mr. Watson’s recent 1,500 flights and 500 hours per year in the air to be exclusively for business purposes and, if so, how that is remotely possible in light of the facts chronicled above.

Inadequate or inaccurate disclosure of compensation and benefits can constitute violations of the proxy solicitation and periodic reporting provisions of the Securities Exchange Act. Failing to properly distinguish personal from business travel also raises questions about internal controls, which can have Sarbanes-Oxley implications. The Commission routinely brings enforcement actions against individuals and companies that it believes have not properly overseen or disclosed executive perquisites (including corporate aircraft), and has imposed substantial penalties on companies whose perquisite disclosures are inadequate.24 Corporate directors who sign the 10-K, which incorporates by reference the disclosures in the Proxy Statement, are also responsible (and potentially liable) for false or incomplete disclosures in this area.25

And it doesn’t stop there. Internal Revenue Code Section 274 disallows corporate deductions for “entertainment, amusement, or recreation” by corporate executives and specifically forbids corporate deductions for personal air travel by executives and officers. As such, any personal use of aircraft cannot be deducted by Argo (and must be categorized as a “fringe benefit” and imputed to Mr. Watson as ordinary income), including “deadhead” costs (empty flight segments caused by the need to re-position aircraft after personal use).26 The Code specifies that the entire deduction for all aircraft expense is forfeited by the Company under such circumstances, not just the variable or incremental cost.

The Bermuda Triangle

Management teams have wide discretion in the day-to-day affairs of a company, and deservedly so. But the independent Directors of any company also play an essential, critical role. Precisely because of the broad latitude afforded to management, a Board must provide effective oversight to ensure that agency issues – which are a risk any time management of an asset is separated from its ownership, as is typical in a corporation – do not compromise the best interests of shareholders.

There’s no more vivid illustration of the potential for conflicts of interest between corporate managers and shareholder owners than compensation generally and executive perquisites in particular. The gray area between business and personal expenses has historically tempted some executives to abuse the trust placed in them by misusing corporate assets for personal gain or pleasure. In light of what we see as the wildly inappropriate use of corporate assets at Argo, and the risks they pose to the Company and the Directors including in their individual capacities, one can only wonder why the purportedly independent Board has stood idly by and allowed this to happen. But therein lies the crux of so many of Argo’s governance failures: Argo’s Board is very far from independent, having long ago been captured by its imperial CEO.

Lack of Independence. We believe the independence of Argo’s Board has been compromised in part by its excessive tenures. The average service of the 10 independent Directors exceeds 12 years. Four of the independents are over 70 years old (two exceed 75) and this core group of old-timers has an average Board tenure of almost 20 years each. Let’s start with the Chairman, Gary Woods, who is 75 and has spent 19 years on the Board. John Power has been hanging on for 19 years, Hector De Leon for 16 years and this will be Mural Josephson’s 15th year on Argo’s Board. Or consider Francis Sedgwick Browne, aged 76, who will celebrate his platinum anniversary (20th) in 2019. After two decades, what incremental contributions can reasonably be expected from these gentlemen? Unfortunately, there doesn’t seem to be any concept of planned retirement on Argo’s Board: The most recent Argo Director to depart only did so after passing away last year, at the age of 80.

It’s not just the Board’s lengthy tenures but also its lack of pluralism that raises serious concerns. The aforementioned fossils are not only the Board’s elders but also its power brokers, controlling all of the Board’s key committees. Mr. Woods is the Board’s Chairman, but he also sits on four other committees (more than any other Director), and just for good measure is also the Chairman of the Nominating Committee; Mr. Browne is the former Vice-Chairman of the Board and the Chairman of the Risk and Capital Committee; Mr. Power runs the Comp Committee; and Mr. Josephson heads Audit. Messrs. De Leon and Woods comprise the Executive Committee, along with Mr. Watson. While the Board will likely tout its recent Director appointments, each of them were allowed only one committee assignment and none chairs a committee.

We also note how incestuous Argo is. One name to remember is Titan Holdings, Inc. (“Titan”), an insurance company run by Mr. Watson’s father (Mark Edmund Watson, Jr.). CEO Watson (that is, Mark Edmund Watson III) was added to the Board of Titan in 1992 when he was just a lad of 27 years. Messrs. De Leon and Woods were also his father’s Titan Directors (although Mr. Wood’s Argo biography omits that interesting tidbit), making them more like Mr. Watson’s uncles than his bosses. Mr. Tonelli is also not exactly an outsider: He spent five years working closely with Argo’s CFO, Mr. Bullock, in the financial institutions group at Bear Stearns & Co., Inc. CFO Bullock himself, while not a Director, is also part of the clique; he previously served as Argo’s investment banker while at the Bear.

Misalignment. The independent Directors collectively own very little of its stock, amounting to less than one-half of one percent (0.5%) of the Company’s shares outstanding. This is particularly pathetic given the extraordinarily long tenures of these Directors. Seven of the ten independent Directors haven’t purchased a single share of stock in the open market in at least the past ten years. As a result, almost 85% of their holdings have been granted to them rather than bought through a conscious investment decision. What’s worse, every Director (other than the recent appointees who have little or no vested stock yet to sell) has been a net seller of Argo shares, in meaningful amounts and in aggregate over half of their gross stock holdings. And even more concerning, every independent Director (again, excluding the ones with no stock yet to sell) has sold Argo stock within the past fifteen months. Mr. Watson himself has been a prolific seller of stock, dumping over 620,000 shares in the past ten years. While Mr. Watson was shedding Argo stock as recently as November of last year, Voce was in the open market buying it.

Argo also allows its officers and Directors to pledge their shares in order to use them for other purposes. This is a terrible policy from a governance standpoint, and can lead to significant damage to shareholders in times of financial stress, when insiders must sell holdings to meet collateral obligations as the share price is falling. (Just ask shareholders of Valeant, Chesapeake Energy and eToys, for example, how they fared when their CEOs had to meet margin calls on stock they had pledged.) Argo fails to net the pledged holdings against the reported insider beneficial ownership despite the fact that the pledged amounts are often material. There’s no disclosure of Mr. Watson’s pledges of Argo stock prior to 2012, but we do know that since then his pledges have averaged 13% of his holdings (and sometimes exceeded 20%).

Inexperience. The composition of Argo’s Board also reveals some glaring deficiencies. Four of Argo’s Directors are attorneys. Argo already has its own General Counsel and presumably avails itself of the best external legal advice that shareholder money can buy; why pick four lawyers as Directors? Three of the Directors are accountants by training, another valuable skill but one in seeming over-abundance on Argo’s Board. Another Director is a retired strategy consultant and two more are investment bankers. For such a large group, what’s so striking is that there are no Chiefs on the Board, only Indians. Professional service providers tend not to be decision makers or principals, but rather agents who have spent their careers peddling advice to, and currying favor with, CEOs just like Mr. Watson. These are not typically the kind of individuals who rock the boat (or in Argo’s case, the yacht), which is likely the reason they were selected.

Chimeric Engagement

The foregoing analysis pertains to the Board as it existed on February 4, 2019, the first public disclosure of our involvement. Other than the required filing of our Schedule 13D, until now we’ve made no public comment of any kind about our investment in Argo, conducting all communications privately.

We tried on three separate occasions to meet with management and received no response to any of our formal requests. It was only after significant back and forth, including our disclosure to management that we owned almost 5% of the Company, that it relented and agreed to talk with us earlier this month. As a follow up to our management discussion, we had scheduled a meeting with the Board for this Wednesday, February 27, 2019 in New York City (Argo chose the location), the purpose of which was to privately discuss the concerns we have about Argo’s corporate governance and which comprise the gravamen of this letter. Rather than even wait to hear what we had to say, Argo unilaterally expanded its already bloated Board to 13 members (the maximum allowed by its charter) and stuffed it with two more hand-selected Directors ahead of meeting with us (without any communication with us before or even after, despite us having extended that courtesy to the Company previously).

As further evidence of the Board’s gamesmanship, the Director appointments lack customary public disclosure of which classes the new Directors have joined – critical information for a company with a “staggered” Board such as Argo’s (particularly for appointments being made just two weeks prior the Company’s advance notification deadline for shareholder Director nominations). Argo’s sudden and reactive changes, in the middle of our conversation with it, neither impress us nor alter our grave concerns regarding the Board’s fitness and integrity. To the contrary, the shotgun Board appointments further illustrate its entrenchment and hostility toward the interests of shareholders.

Righting the Ship

The corporate responsibility page of Argo’s flashy website includes the following statement:

At Argo Group, we are committed to upholding the highest standards of corporate governance and ethical conduct. Our Board of Directors provides oversight of the company’s affairs and continuously looks for ways to improve and build upon Argo Group’s strong corporate governance practices. Argo Group is dedicated to ensuring that our accounting and reporting systems operate with integrity and that our financial results accurately and fairly reflect the results of our operations. We strive to consistently provide financial information that is objective, transparent, timely and relevant. Abiding by these principles is vital to securing trust and respect from our shareholders, customers, employees and business partners.

As this letter makes clear, we believe the only sentence in the Company’s statement that is true is the final one. But precisely because of the importance of the constituencies identified at the end of the passage – shareholders, customers, employees and business partners – we intend to make a constructive impact at Argo.

Our plan to help Argo reach its full potential begins with substantial, immediate reform of its Board. This must include the election of Directors nominated by shareholders, not management, and who bring the independence, experience and alignment with shareholders to faithfully execute their duties. Therefore today we are formally nominating four outstanding, independent Director candidates for election to the Board of Argo at the 2019 Annual Meeting. We look forward to presenting our slate of Nominees to our fellow shareholders and helping Argo chart a course of sustainable long-term value creation.27

Respectfully yours,

VOCE CAPITAL MANAGEMENT LLC

By: ___________________________________

J. Daniel Plants

Chief Investment Officer

About Voce Capital Management LLC

Voce Capital Management LLC is a fundamental value-oriented, research-driven investment adviser founded in 2011 by J. Daniel Plants. The San Francisco-based firm is 100% employee-owned.

Additional Information and Where to Find It

Voce Catalyst Partners LP, Voce Capital Management LLC, Voce Capital LLC, and J. Daniel Plants, (collectively, the “Participants”) intend to file with the Securities and Exchange Commission (the “SEC”) a definitive proxy statement and accompanying form of proxy to be used in connection with the solicitation of proxies from the members of Argo Group International Holdings, Ltd. (the “Company”). All members of the Company are advised to read the definitive proxy statement and other documents related to the solicitation of proxies by the Participants when they become available, as they will contain important information, including additional information related to the Participants and information about the Participants' director nominees. The definitive proxy statement and an accompanying proxy card will be furnished to some or all of the Company’s stockholders and will be, along with other relevant documents, available at no charge on the SEC website at http://www.sec.gov/.

Cautionary Statement Regarding Forward-Looking Statements

All statements contained in this press release that are not clearly historical in nature or that necessarily depend on future events are "forward-looking statements," which are not guarantees of future performance or results, and the words "anticipate," "believe," "expect," "potential," "could," "opportunity," "estimate," "plan," and similar expressions are generally intended to identify forward-looking statements. The projected results and statements contained in this press release that are not historical facts are based on current expectations, speak only as of the date of this press release and involve risks that may cause the actual results to be materially different. In light of the significant uncertainties inherent in the forward-looking statements, the inclusion of such information should not be regarded as a representation as to future results. Voce disclaims any obligation to update the information herein and reserves the right to change any of its opinions expressed herein at any time as it deems appropriate. Voce has not sought or obtained consent from any third party to use any statements or information indicated herein as having been obtained or derived from statements made or published by third parties.

| 1 |

“Argo Group, CEO Mark Watson Anchor Downtown Business,” Rivard Report, December 5, 2016. |

| 2 |

“Corporate Collections Show Art Can Be Good Business,” Rivard Report, July 10, 2017. |

| 3 |

“Argo Group, CEO Mark Watson Anchor Downtown Business,” Rivard Report, December 5, 2016. |

| 4 |

“Manhattan’s Cool Tech Neighborhoods Come of Age,” The Wall Street Journal, July 2, 2017. |

| 5 |

“Insurance Company to Anchor New Meatpacking District Building,” Crain’s New York Business, March 5, 2017. The Company’s former offices, at the corner of Bleecker and Houston Streets in Manhattan’s SoHo neighborhood, were apparently no longer adequate. |

| 6 |

“At Insurance Company Argo Group’s New York Office, TPG Proves Good Design Is the Best Policy,” Interior Design, November 8, 2018. |

| 7 | Argo Group’s logo and branding are nautically-themed. It has a splashy website of high-resolution images, on-location videos from all over the world and many on-camera interviews with Mr. Watson. We believe the expense to create and maintain a substantial web presence resembling a consumer-facing marketing company is unwarranted and wasteful for a B2B entity such as Argo. |

| 8 |

See www.theoceanrace.com. |

| 9 |

Argo has previously sponsored other racing teams, such as Team Aguri, stretching back at least a decade. See Mark E. Watson III, “What We’ve Learned About Recruiting by Watching Artemis Racing.” (Link). |

| 10 | For example: “We celebrate the risk-takers who challenge themselves and change the world.” The same could be said by sponsoring foreign service volunteers or a local charity that collects roadside litter. |

| 11 |

“Foundation Backs Youth Sailing Group,” The Royal Gazette, February 16, 2019 (Link); “Argo Foundation Donates to Sloop Programme,” The Royal Gazette, October 22, 2018 (Link). |

| 12 |

“Argo Group Unites With Artemis Racing and ASSF to Support the Future of Sailing,” Sept. 15, 2016 (Link). |

| 13 |

See San Antonio Museum of Art, 2017-18 Annual Report, pp. 47-49. |

| 14 |

Executive Employment Agreement dated August 17, 2007, Sections 3(f) and (g) (Link). |

| 15 |

Executive Employment Agreement dated November 5, 2018 (Link). |

| 16 |

“Bermuda’s World Business Leaders and Their Locally-Registered Companies,” Bermuda Online (Link). |

| 17 |

“Insurance Company to Anchor New Meatpacking District Building,” Crain’s New York Business, March 5, 2017. |

| 18 | It’s an Embraer EMB-505, known as the “Phenom 300.” |

| 19 |

“Business as an Adventure,” Leader’s Edge, November 2012. |

| 20 | Based on an hourly variable rate of $4,230. |

| 21 | Mr. Watson is a member of the Board of Trustees of IYRS School of Technology & Trades in Newport and a former Trustee of the Preservation Society of Newport County. |

| 22 |

See “Everything You Need to Know About All 24 Art Fairs at Art Basel in Miami Beach,” Artnet News, November 22, 2016. This is the corporate art buying boondoggle referred to in the Rivard News story at footnote 1, supra: “Recently, Watson traveled to Florida to add to the impressive collection at Art Basel Miami Beach, a major contemporary art show.” Id. |

| 23 |

See generally 17 CFR Part 229 Section 402. |

| 24 |

See, e.g., SEC v. John D. Schiller, Jr., Civil Action No. 4:18-cv-02433 (S.D. Tex.) (2018); In the Matter of MDC Partners, Inc. (2017); SEC v. Andrew M. Miller, Civil Action No. 3:15-cv-1461-YGR (LB) (N.D. Cal.) (2016). |

| 25 |

See, e.g., In the Matter of W.R. Grace & Co., Administrative Proceeding File No. 3-9460 (1997). Although the issuer settled the matter and paid a fine related to its inadequate disclosure of executive benefits, the SEC issued a related Report of Investigation, Release No. 39157 (September 30, 1997) specifically to address what it deemed the failures of the officers and directors: “The Commission is issuing this Report of Investigation to emphasize the affirmative responsibilities of corporate officers and directors to ensure that the shareholders whom they serve receive accurate and complete disclosure of information required by the proxy solicitation and periodic reporting provisions of the federal securities laws. Officers and directors who review, approve, or sign their company's proxy statements or periodic reports must take steps to ensure the accuracy and completeness of the statements contained therein, especially as they concern those matters within their particular knowledge or expertise. To fulfill this responsibility, officers and directors must be vigilant in exercising their authority throughout the disclosure process.” |

| 26 | 26 CFR § 1.61-21(a). |

| 27 | The views expressed in this letter are solely those of Voce and no other person; none of the Nominees played any part in the drafting of this letter. |