")

LONDON--(BUSINESS WIRE)--Canadian manufacturers recorded robust rises in output, new orders and employment during July, thereby signalling another marked improvement in overall business conditions across the sector. However, the latest survey also signalled a steep and accelerated rise in prices charged by manufacturing firms, which was widely linked to the impact of U.S. trade tariffs on steel and aluminium. At the same time, strong demand for raw materials and transportation bottlenecks led to a survey-record lengthening of delivery times from suppliers.

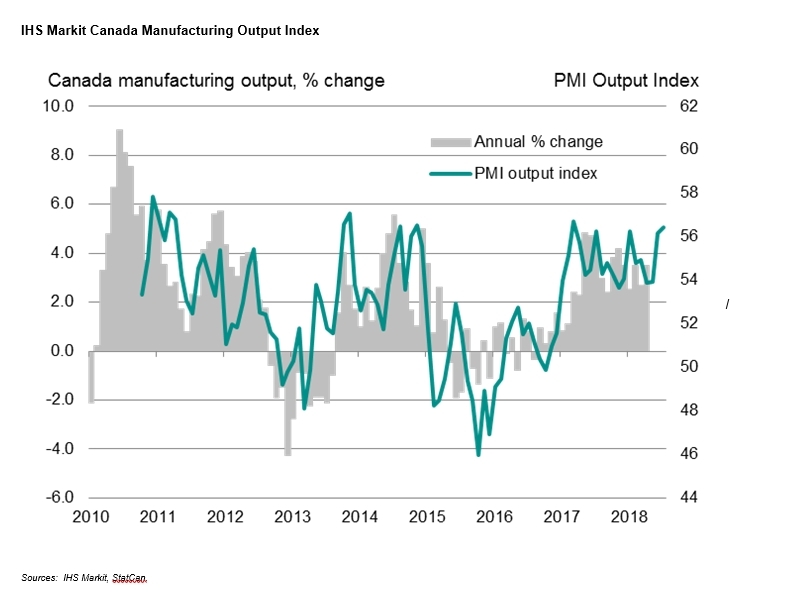

At 56.9 in July, the seasonally adjusted IHS Markit Canada Manufacturing Purchasing Managers’ Index® (PMI™) fell only slightly from June’s survey-record high of 57.1 and remained indicative of a strong improvement in overall business conditions. The headline index was supported by the fastest rise in production volumes since March 2017, which partially offset softer rates of new business growth and job creation compared to the previous month.

Strong output growth was linked to robust order books and ongoing efforts to boost operating capacity across the manufacturing sector. Higher levels of production have been recorded in each month since November 2016.

July data pointed to a robust increase in new work received by manufacturing firms, with the rate of expansion only slightly softer than June’s four-and-a-half year peak. The slowdown partly reflected a weaker contribution from export order growth, which was the least marked since March. Survey respondents noted that rising transport costs and, in some cases, output price increases related to trade tariffs had acted as a headwind to export sales growth.

Manufacturers are upbeat about the outlook for production levels at their plants in the next 12 months. The degree of positive sentiment eased fractionally since June, but remained broadly in line with the average so far in 2018. Resilient business confidence and another solid rise in backlogs of work underpinned sustained employment growth in July.

Intense supply chain pressures continued in July, as highlighted by the greatest lengthening of lead-times from vendors since the survey began in October 2010. Manufacturers again sought to compensate for worsening supplier performance by boosting their stocks of inputs.

Input cost pressures eased only slightly from the seven-year peak seen in June. Survey respondents mainly cited the inflationary impact of trade tariffs for metal products, alongside rising fuel prices. Surcharges for raw materials were passed on to clients in July, with factory price inflation accelerating to a survey-record high.

Regional highlights:

- Robust upturn in manufacturing conditions seen across all regions, led by Quebec

- Quebec experienced the greatest lengthening of suppliers’ delivery times in July

- Manufacturers in Alberta & BC recorded the sharpest rise in average cost burdens, as well as the greatest degree of inventory building

Comment:

Christian Buhagiar, President and CEO, SCMA

“The manufacturing sector continued to perform strongly during July, with growth proving resilient against a backdrop of intense supply chain pressures and escalating concerns about global trade.

“Output volumes expanded at the fastest pace for almost a year-and-a-half, supported by strong order books and successful efforts to rebuild production capacity in response to rising client demand.

“While domestic sales remained the main growth impetus in July, the latest survey indicated another solid upturn in new export orders.

“Delivery times for raw materials lengthened to the greatest extent for over seven-and-a-half years, reflecting shortages of freight capacity and forward purchasing ahead of U.S. trade tariffs.

“Surcharges on steel and aluminum products placed upward pressure on manufacturing costs, alongside the sharpest rise in prices at the factory gate since the survey began in 2010.”

Note to Editors:

The IHS Markit Canada Manufacturing PMI™ Report is based on data compiled from monthly replies to questionnaires sent to purchasing executives in over 400 industrial companies. The panel is stratified by company workforce size and by Standard Industrial Classification (SIC) group, based on industry contribution to Canada GDP.

Survey responses reflect the change, if any, in the current month compared to the previous month based on data collected mid-month. For each of the indicators the ‘Report’ shows the percentage reporting each response, the net difference between the number of higher/better responses and lower/worse responses, and the ‘diffusion’ index. This index is the sum of the positive responses plus a half of those responding ‘the same’.

Diffusion indexes have the properties of leading indicators and are convenient summary measures showing the prevailing direction of change. An index reading above 50 indicates an overall increase in that variable, below 50 an overall decrease. The IHS Markit Canada Manufacturing Purchasing Managers’ Index® (PMI™) is a composite index based on five of the individual indexes with the following weights: New Orders - 0.3, Output - 0.25, Employment - 0.2, Suppliers’ Delivery Times - 0.15, Stock of Items Purchased - 0.1, with the Delivery Times Index inverted so that it moves in a comparable direction.

The Purchasing Managers’ Index (PMI) survey methodology has developed an outstanding reputation for providing the most up-to-date possible indication of what is really happening in the private sector economy by tracking variables such as sales, employment, inventories and prices. The indices are widely used by businesses, governments and economic analysts in financial institutions to help better understand business conditions and guide corporate and investment strategy. In particular, central banks in many countries (including the European Central Bank) use the data to help make interest rate decisions. PMI surveys are the first indicators of economic conditions published each month and are therefore available well ahead of comparable data produced by government bodies.

IHS Markit does not revise underlying survey data after first publication, but seasonal adjustment factors may be revised from time to time as appropriate which will affect the seasonally adjusted data series. Historical data relating to the underlying (unadjusted) numbers, first published seasonally adjusted series and subsequently revised data are available to subscribers from IHS Markit. Please contact economics@ihsmarkit.com.

About Supply Chain Management Association

The Supply Chain Management Association (SCMA) is Canada’s largest association for supply chain management professionals. We represent 7,500 members as well as the wider profession working in roles that cover sourcing, procurement, logistics, inventory, and contract management. SCMA sets the standards for excellence and ethics, and is the principal source of professional development and accreditation in supply chain management in Canada. www.scma.com.

About IHS Markit (www.ihsmarkit.com)

IHS Markit (Nasdaq: INFO) is a world leader in critical information, analytics and solutions for the major industries and markets that drive economies worldwide. The company delivers next-generation information, analytics and solutions to customers in business, finance and government, improving their operational efficiency and providing deep insights that lead to well-informed, confident decisions. IHS Markit has more than 50,000 business and government customers, including 80 percent of the Fortune Global 500 and the world’s leading financial institutions.

IHS Markit is a registered trademark of IHS Markit Ltd and/or its affiliates. All other company and product names may be trademarks of their respective owners © 2018 IHS Markit Ltd. All rights reserved.

About PMI

Purchasing Managers’ Index® (PMI™) surveys are now available for over 40 countries and also for key regions including the eurozone. They are the most closely-watched business surveys in the world, favoured by central banks, financial markets and business decision makers for their ability to provide up-to-date, accurate and often unique monthly indicators of economic trends. To learn more go to www.ihsmarkit.com/product/pmi.

The intellectual property rights to the IHS Markit Canada Manufacturing PMI™ provided herein are owned by or licensed to IHS Markit. Any unauthorised use, including but not limited to copying, distributing, transmitting or otherwise of any data appearing is not permitted without IHS Markit’s prior consent. IHS Markit shall not have any liability, duty or obligation for or relating to the content or information (“data”) contained herein, any errors, inaccuracies, omissions or delays in the data, or for any actions taken in reliance thereon. In no event shall IHS Markit be liable for any special, incidental, or consequential damages, arising out of the use of the data. Purchasing Managers' Index® and PMI™ are either registered trade marks of Markit Economics Limited or licensed to Markit Economics Limited. IHS Markit is a registered trademark of IHS Markit Ltd and/or its affiliates.