NEW YORK--(BUSINESS WIRE)--Shortly after each medical appointment, your health plan sends out an Explanation of Benefits (EOB) that is supposed to clarify how costs for services are split between you and your insurer.

But the EOB isn’t as enlightening as some insurers might hope it to be. It’s often difficult to parse out what was paid, what was reduced due to provider contracts and – more importantly – what part of the cost is your responsibility.

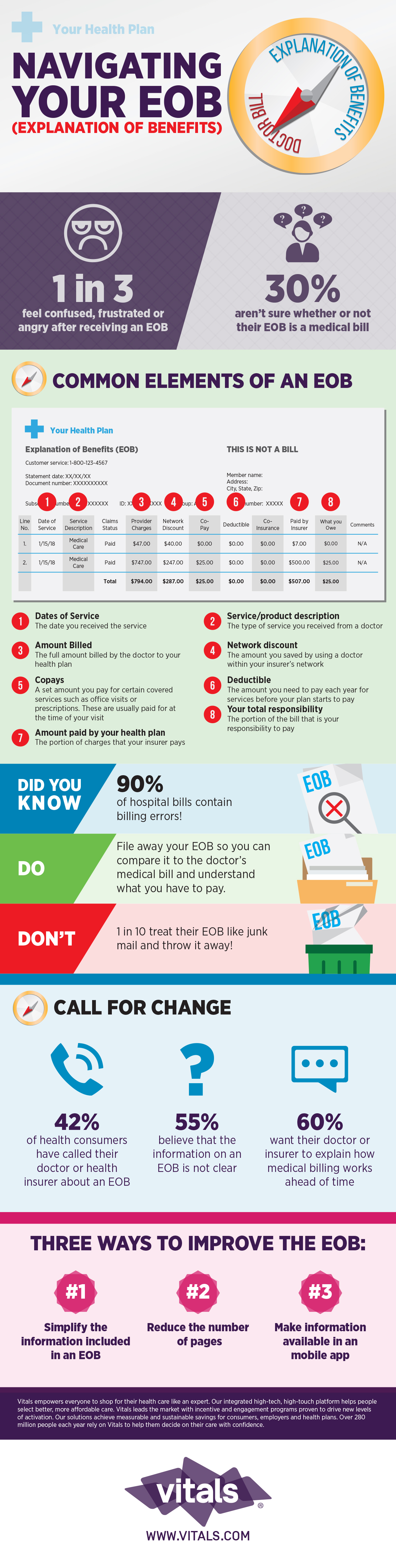

Now, a survey from Vitals finds that about 1 in 3 health care consumers feel either confused, frustrated or downright angry after receiving an EOB. Most people who’ve called their health plan or doctor about an EOB said they didn’t know what amount was paid by their health plan and what amount was their responsibility.

Surprisingly, despite EOBs being referred to as the “THIS IS NOT A BILL” letter (the words splayed across the top of the mailer), almost 30 percent of consumers still weren’t sure if their EOB is a medical bill.

Part of the confusion stems from the fact that there are no industry standards with regards to what information a patient should receive in their EOB. Some include procedure names, some include procedure codes, some don’t include any at all.

The lack of standardization makes it hard for consumers to dispute or even clarify bills when comparing them to their EOB. And it creates an environment where consumers become apathetic, rather than engage in their health care. Indeed, one out of 10 surveyed said they treat their EOB like junk mail – and just throw it out.

That’s a bad move, considering a group of auditors hired by insurance companies found errors in over 90 percent of the hospital bills they examined. An audit by Equifax found that hospital bills that totaled more than $10,000 contained an average error of $1,300. That money often comes out of consumer’s pocket!

With consumers on the hook for more of their health care, they need to be educated about how to navigate medical costs – both before and after a medical event. At the same time, the industry needs to become more consumer-centric, as well. Sixty-percent of consumers agreed or strongly agreed that they wished their doctor or insurance company would explain how medical billing works.

“Contrary to popular belief, high-deductibles and health savings accounts (HSAs) alone won’t create empowered health care consumers or functional health care marketplaces,” said Mitch Rothschild, Founder and Chairman of Vitals. “Stakeholders across the health care ecosystem need to innovate, remove friction points and design products and processes that are easy-to-use, convenient and value-priced.”

According to the survey, incumbents can start by simplifying the information included in that document. Young adults would like to see their EOBs emailed or available in a mobile app.

Indeed, there’s increased pressure to create better consumer experiences based on recent industry headlines. With 83 percent of Americans living within 10 miles of a CVS and 50 percent of households subscribed to Amazon Prime, traditional health care providers need to rethink their consumer touchpoints –including EOBs – to retain customers.

Vitals enterprise solutions, which include the VitalsChoice transparency platform and Vitals SmartShopper incentive and engagement program, help consumers find high-quality, lower-cost care through web-based tools and concierge-style services. Vitals partners with health plans and employers to engage and incentivize consumers to shop for health care and ultimately reduce costs for all.

About Vitals

Vitals empowers everyone to shop for their health care like an expert. Our integrated high-tech, high-touch platform helps people select better, more affordable care. Vitals leads the market with incentive and engagement programs proven to drive new levels of activation. Our solutions achieve measurable and sustainable savings for consumers, employers and health plans. Over 280 million people each year rely on Vitals to help them decide on their care with confidence.