PARIS--(BUSINESS WIRE)--Despite a slight deceleration, Asia-Pacific maintained its No. 1 spot in both high net worth individual (HNWI)1 population and wealth, and is on target to surpass US$40 trillion in HNWI wealth by 2025, according to the 2017 Asia-Pacific Wealth Report (APWR) released today by Capgemini. Although Asia-Pacific (excluding Japan) HNWI investments held by wealth managers grew an extraordinary 33 percent in 2016, overall satisfaction with wealth managers remained muted as HNWIs sought holistic value beyond investment returns.

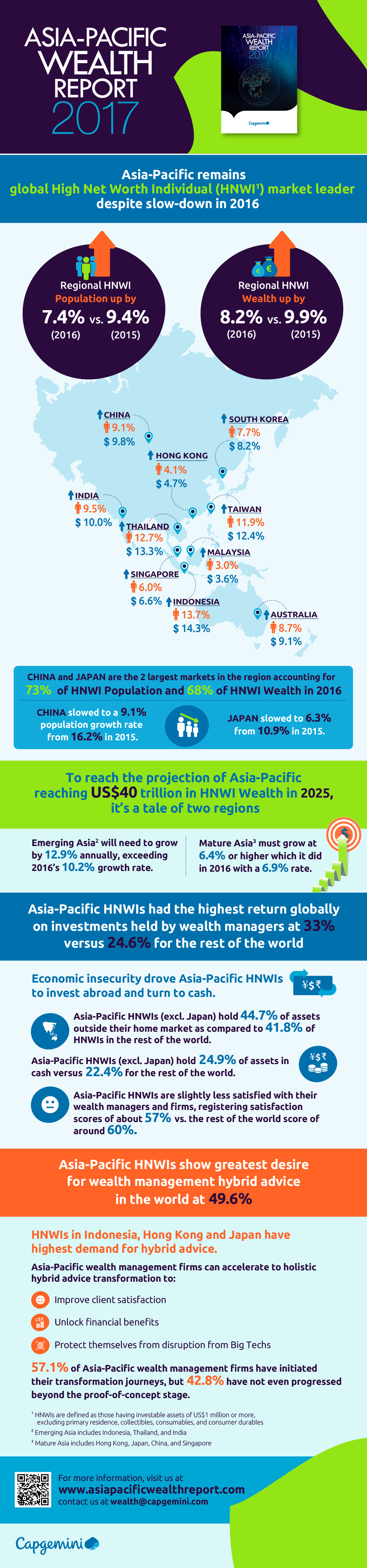

Outperforming all other regions, Asia-Pacific remains the global leader in HNWI population and wealth, but its pace slowed slightly in 2016 with population and wealth increasing 7.4 percent and 8.2 percent, respectively, down from 9.4 percent and 9.9 percent in 2015.

Previously, China and Japan have powered Asia-Pacific HNWI population growth, but their 2016 slowdown affected the region overall. China came in as the 33rd fastest-growing market globally, up just 9.1 percent compared with 16.2 percent in 2015. Japan was the 41st fastest-growing market in 2016, growing 6.3 percent compared with 10.9 percent in 2015. The slowdown is significant, because China and Japan are the two largest markets in the region, together accounting for 73 percent of the Asia-Pacific HNWI population and 68 percent of HNWI financial wealth in 2016.

Only the United States added more HNWIs (337,000) than Japan (171,000) and China (95,000) in 2016, but Asia-Pacific leads North America by 360,000 HNWIs and US$863 billion in HNWI financial wealth.

Anirban Bose, Head of Global Banking and Capital Markets at Capgemini said, “We project that Asia-Pacific will surpass US$40 trillion in HNWI wealth by 2025 if Emerging Asia2 capitalizes on its tremendous potential to grow at 12.9 percent annually – exceeding the 10.2 percent rate of 2016 – and if Mature Asia3 grows at 6.4 percent or higher, which it accomplished in 2016 at 6.9 percent.”

The average Asia-Pacific (excluding Japan) wealth manager-held HNWI portfolio had a return of 33 percent in 2016, well above the 24.6 percent increase for HNWIs in the rest of the world. This robust performance helped drive highly-liquid assets, such as equities, to a five-year high, although cash allocations increased as well. HNWI allocations to equities and cash increased significantly year over year, up 4.4 percentage points and 4.3 percentage points, respectively, and was the highest annual rise in the last five years.

Opportunity exists for improvement in customer satisfaction

However, Asia-Pacific HNWI overall satisfaction was somewhat muted, as fee transparency and overall value delivered by wealth managers were top concerns. Asia-Pacific HNWIs showed a high Net Promoter Score® 4 (31.4), but this encouraging metric masks underlying problems in specific markets. Negative scores in Japan (−51.3), Hong Kong (−19.8), Singapore (−11.0), and Malaysia (−14.4) may become worrisome for the industry. Younger Asia-Pacific HNWIs are far more likely to recommend their wealth service providers than older individuals, with an NPS® of 32.0 for the ‘under 40s’ HNWIs, and an NPS® of 1.0 for HNWIs aged 60 and above. The majority of HNWI wealth in the region is believed to remain with first- and second-generation wealth creators, therefore lower Net Promoter Scores among older individuals may become an issue, especially in emerging markets.

Offshore investment higher for Asia-Pacific HNWIs

Asia-Pacific (excluding Japan) HNWIs hold 44.7 percent of assets outside their home market as compared to 41.8 percent of HNWIs in the rest of the world. Hong Kong has by far the most internationally-minded HNWIs, although HNWIs from all markets within the region hold at least one-third of their financial wealth abroad.

Asia-Pacific HNWIs prefer a variety of offshore destinations, but Hong Kong and Singapore are preferred overall. For example, HNWIs in China, Malaysia, and Indonesia prefer Hong Kong and Singapore while New York and London are favorites of HNWIs in Japan, Australia, and Hong Kong.

The industry, especially in the key financial centers of Hong Kong and Singapore, will need to accelerate investment in digital technology to meet Asia-Pacific HNWI demand for offshore wealth management, hybrid5 and self-service advice delivery to improve client satisfaction, unlock financial benefits, and protect against BigTech6 disruption.

Asia-Pacific Wealth Report 2017 Methodology

The Asia-Pacific Wealth Report from Capgemini is the industry-leading benchmark for tracking high net worth individuals (HNWIs) in the Asia-Pacific region, their wealth, and the global and economic conditions that drive change in the Wealth Management industry. The 12th annual edition includes findings from an in-depth primary research on global HNWI perspectives and behavior. The 2017 Asia-Pacific Wealth Report focuses on 9 core markets: Australia, China, Hong Kong, India, Indonesia, Japan, Malaysia, Singapore, and South Korea. The market-sizing model includes 18 countries and territories (i.e., the 9 core markets plus New Zealand, Kazakhstan, Myanmar, Pakistan, Philippines, Sri Lanka, Taiwan, Thailand, and Vietnam.)

About Capgemini

A global leader in consulting, technology services and digital transformation, Capgemini is at the forefront of innovation to address the entire breadth of clients’ opportunities in the evolving world of cloud, digital and platforms. Building on its strong 50-year heritage and deep industry-specific expertise, Capgemini enables organizations to realize their business ambitions through an array of services from strategy to operations. Capgemini is driven by the conviction that the business value of technology comes from and through people. It is a multicultural company of 200,000 team members in over 40 countries. The Group reported 2016 global revenues of EUR 12.5 billion.

Visit us at www.capgemini.com. People matter, results count.

Capgemini’s Financial Services Business Unit offers global banks, capital markets firms, and insurers transformative business and IT solutions to help them nimbly respond to industry disruptions, to give their customers differentiated value, and to expand their revenue streams. A team of more than 55,000 professionals collaboratively delivers a holistic framework across technologies and geographies, from infrastructure to applications, to provide tailored solutions to 1000+ clients, representing two-thirds of the world’s largest financial institutions. Client engagements are built on bar-setting expertise, fresh market insights and more than a quarter century of global delivery excellence. Learn more at www.capgemini.com/financialservices.

1 HNWIs are defined as those having investable assets of US$1million or more, excluding primary residence, collectibles, consumables, and consumer durables

2 Emerging Asia Includes China, India, Indonesia, and Thailand

3 Mature Asia includes Japan, Australia, New Zealand, Singapore, Hong Kong, Taiwan, Malaysia, and South Korea

4 Net Promoter, Net Promoter System, Net Promoter Score, NPS®, and the NPS®-related emoticons are registered trademarks of Bain & Company, Inc., Fred Reichheld and Satmetrix Systems, Inc. Net Promoter Score® (NPS®) is an index ranging from -100 to 100 that measures the willingness of customers to recommend a company's products or services to others. It is used as a proxy for gauging overall satisfaction with a company's product or service and the customer's loyalty to the brand

5 Capgemini defines the hybrid-advice model as, “Putting clients in the driver’s seat by allowing them to tap into life-stage and need-based wealth management and financial planning capabilities in a modular, personalized pay-as-you-go manner. These capabilities will be delivered through: the amalgamation of (1) a cognitive analytics-driven automated/self service delivery (such as for basic investment management); (2) a human-led delivery (such as for complex wealth structuring); or (3) a wealth manager-assisted hybrid approach – as preferred by the client”

6 BigTech is a general term referring to technology firms not traditionally present in Asia-Pacific financial services, such as Alibaba and Tencent