")

BOSTON--(BUSINESS WIRE)--While saving for college remains at an all-time high with 72 percent of families focused on building their college nest eggs, Fidelity Investments® new College Savings IQ survey reveals that many parents could benefit from additional education when it comes to savings and planning best practices. The survey identified knowledge gaps in three categories: 1) the future cost of college and how much they should be saving; 2) fundamentals of 529 college savings plans; and 3) how saving for college impacts financial aid eligibility.

Parents Committed to Minimizing Student Debt, but Underestimate

College Costs

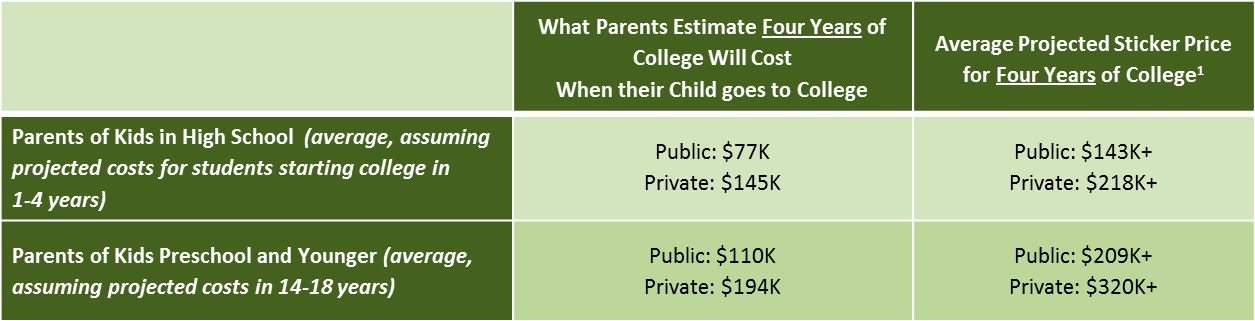

While college savers appreciate higher education

as an investment in the future, many parents may be dramatically underestimating

the sticker price associated with earning a degree, based on current

average costs and rates of college inflation. When asked what they

expect the four-year cost of college will be by the time their child

heads to campus (before financial aid, scholarships or other discounts),

parents of preschoolers fell short by an eye-opening average of

$110,000, according to the current pace of college inflation1.

Even parents with high school students, who should be most likely to

have a handle on what to expect, were significantly off the mark,

underestimating the potential sticker price of a four-year degree by an

average of $70,000.

Estimating future college costs is not the only area where parents need more guidance. Nearly half (45 percent) of parents admit they do not have a good idea of exactly how much they should be saving each month.

“Pinpointing how much you should save can feel like a moving target — especially when your kids are young and college goals for your child’s education may be more undefined,” says Keith Bernhardt, vice president of college planning at Fidelity. “But the key is to get started. Set a reasonable goal to start building your college fund, and take advantage of free and simple to use tools available online to refine your savings goals over time.”

This uncertainty is not hindering parents’ motivation to save and ultimately reduce the potential student loan debt their children may face down the road. Eight-in-10 parents cite concern for their child taking on significant debt as a factor motivating them to save more. Just how much debt do they worry their kids will carry? Eighty-five percent of parents expect their child to graduate with debt, estimating an average of $45,000 in student loans.

Furthermore, many parents are looking to reduce the financial burden their children will face. In fact, many parents intend to bear the brunt of college expenses, planning to cover 51 percent of college costs with their own savings and parental loans. They expect their child to take on approximately a quarter (23 percent) of the expenses and estimate another 19 percent will be covered by scholarships.

For many, this commitment may be influenced by their own experience managing debt. Thirty-seven percent of parents with kids in high school report they are still paying down their own student loans; that percentage skyrockets to 68 percent for parents of kids in preschool or younger.

To help do their part, nearly half (48 percent) of parents saving for college are doing so in a tax-advantaged 529 plan, with those contributing regularly saving a median of $300 each month. Almost all (93 percent) believe that saving in a dedicated college account helps keep them on track as they work toward their college goals. Overall, 529 plan owners report having accumulated an average of approximately 50 percent more in their college nest egg than those who are saving, but not using a 529 plan ($32k vs. $21k).

In addition, nearly half of parents saving for college (49 percent) are working with a financial professional for savings and planning guidance as they work toward these college goals, and those working with an advisor report having saved an average $14k more than those without.

Opportunity to Build Greater Awareness of 529 College Savings Plan

Benefits

While familiarity with 529

plans continues to grow (76 percent say they are very/somewhat

familiar), many parents still remain unclear on the basics of these

accounts, and may be missing out on certain benefits and opportunities

to maximize their savings potential. When asked questions specific to

college savings plans, many showed a lack of understanding around key

529 plan attributes including:

- Account owners can change a plan’s beneficiary at any time.

- 529 savings can be used to pay for more than just tuition and school fees.

- Account owners have the ability to adjust the investments within their 529 plan portfolio after opening.

- Options for 529 savings if the beneficiary doesn’t need all funds to pay for college.

- Whether their home state offers a tax deduction or credit for contributions to college savings.

While there is still work to be done to raise greater awareness of 529 plans and their benefits, Fidelity sees more families taking advantage of this tax-advantaged savings vehicle each year. The firm has seen a 34 percent increase in 529 college savings plan account openings through the first half of 2017, compared to the same time last year.

Parents Need More Insight into How (Little) Saving Affects Financial

Aid

The third category that caused confusion among parents is

recognizing that saving for college has only a small impact on financial

aid eligibility. One of the most popular myths associated with college

savings is that saving too much will significantly hurt a family’s

chances for financial aid. Forty-four percent of parents believe that

how much they have saved for college will eliminate their opportunity to

be offered future aid.

In truth, only a small percentage of 529 plan assets (or savings in general), up to 5.6 percent, are included in a family’s Expected Family Contribution (EFC), as determined by the federal financial aid formula. And yet, when asked how much of their total 529 savings they would be expected to contribute per year of college, 98 percent of parents either significantly overestimated or couldn’t answer, illustrating a critical lack of knowledge of how 529 savings are considered in the financial aid evaluation process.

How to Close the Knowledge Gaps and Strengthen College Savings

While

parents may earn high marks for their commitment to saving, taking

action now to learn more about college costs and how to plan for them

can help ensure families reach their college goals. Fidelity recommends

three steps to better prepare:

-

Consider Reaching Out to a Financial Professional: The majority

(78 percent) of savers working with an advisor say that working with a

professional has helped them get closer to their college savings goals.

With 33 percent of parents having either stopped or reduced savings for retirement in order to save for college, advisors can also help prioritize financial needs based on a family’s individual situation.

“Juggling the multitude of financial priorities that are a reality for most families can be overwhelming, from saving for college, to planning for retirement, to building an emergency fund, to managing additional day-to-day financial responsibilities,” said Ron Hazel, senior director of Fidelity Advisor 529 and individual retirement products. “By working with an advisor, parents can benefit from valuable guidance in mapping out their financial landscape and adopting savings and investing strategies to successfully meet their family’s goals.”

- Map Out Your Savings Journey: Parents with a financial plan in place are more than twice as likely to feel they have a good idea of how much they need to save in comparison to those without. Findings in the survey show those with a plan are also more likely to save regularly (72 percent vs 46 percent) and have saved nearly double of those without a financial plan ($34k vs. $19k).

- Find Opportunities to Boost Your College Savings Nest Egg: Savings can truly be a family affair, as previous Fidelity research has found that 90 percent of grandparents would contribute to a college fund if asked2, yet only 23 percent of parents have actually inquired. To make contributing easier, Fidelity offers a 529 Online Gifting Service, which lets owners of Fidelity’s retail 529 college savings accounts use social media to encourage friends and family to help them save for college. For additional ways to jump start savings, see this Calendar of College Savings Strategies.

Both online and in-person resources are available to help families save and plan for college. Parents can access a full library of educational articles, videos, calculators and other tools at Fidelity’s College Learning Center. Additional Viewpoints articles provide a range of insights on college topics including: Are your college savings on track?, ABCs of 529 college savings plans, and 3 “must know” college financial aid tips. College planning specialists are also available to answer questions and provide guidance at Fidelity 196 investor centers across the county, or by calling 800-544-1914.

Tools and Resources for Advisors

Fidelity also provides

financial advisor clients with 529 plan information, marketing support

and online tools such as the 529 State Tax Deduction Calculator and the

College Savings Planning tool. Financial advisors can get more

information at institutional.fidelity.com/529

or 1-800-544-9999.

About the Fidelity Investments College Savings

IQ Survey

As part of the study, Fidelity conducted a

survey of parents with college-bound children of all ages. Parents

provided data on their current and projected household asset levels

including college savings, use of an investment advisor and general

expectations and attitudes toward financing their children’s college

education. Data was collected by Boston Research Technologies, an

independent research firm, through an online survey from July 26 –

August 22, 2017, of 1,984 parents nationwide with children aged 18 and

younger who are expected to attend college. The survey respondents had

household incomes of $30,000 a year or more, and were the financial

decision makers in their household. College costs were sourced from the

College Board’s Trends in College Pricing 2016. The results of the

Fidelity College Savings IQ may not be representative of all parents and

students meeting the same criteria as those surveyed for this study.

About Fidelity Investments

Fidelity’s

mission is to inspire better futures and deliver better outcomes for the

customers and businesses we serve. With assets under administration of

$6.4 trillion, including managed assets of $2.3 trillion as of August

31, 2017, we focus on meeting the unique needs of a diverse set of

customers: helping more than 26 million people invest their own life

savings, 23,000 businesses manage employee benefit programs, as well as

providing more than 12,500 financial advisory firms with investment and

technology solutions to invest their own clients’ money. Privately held

for 70 years, Fidelity employs more than 40,000 associates who are

focused on the long-term success of our customers. For more information

about Fidelity Investments, visit https://www.fidelity.com/about.

The UNIQUE College Investing Plan, the Fidelity Advisor 529 Plan, the U.Fund® College Investing Plan, the Delaware College Investment Plan and the Fidelity Arizona College Savings Plan are offered by the state of New Hampshire, MEFA, the state of Delaware, and the Arizona Commission for Postsecondary Education, respectively, and managed by Fidelity Investments. If you or the designated beneficiary are not a New Hampshire, Massachusetts, Delaware or Arizona resident, you may want to consider, before investing, whether your state or the designated beneficiary’s home state offers its residents a plan with alternate state tax advantages or other benefits such as financial aid, scholarship funds and protection from creditors.

Units of the portfolios are municipal securities and may be subject to market volatility and fluctuation.

This information is intended to be educational and is not tailored to the investment needs of any specific investor.

Fidelity, Fidelity Investments, Fidelity Advisor Funds, and the Fidelity Investments & Pyramid Design logo are registered service marks of FMR LLC.

The third-party marks appearing herein are the property of their respective owners.

Please carefully consider each plan’s investment objectives, risks, charges and expenses before investing. For this and other information, contact Fidelity or visit fidelity.com for a free Fact Kit or request a free Offering Statement from your advisor or through advisor.fidelity.com. Read it carefully before you invest or send money.

Fidelity Brokerage Services LLC, Member NYSE, SIPC

900

Salem Street, Smithfield, RI 02917

Fidelity Investments Institutional Services Company, Inc.,

500

Salem Street, Smithfield, RI 02917

National Financial Services LLC, Member NYSE, SIPC,

200

Seaport Boulevard, Boston, MA 02110

819807.1.0

© 2017 FMR LLC. All rights reserved.

1 College Board, Trends in College Pricing 2016, October 2016. Estimates assume the cost of college is growing at 2.98% each year. A straight average of total charges (tuition, fees, room and board) for a combination of public and private four-year colleges was used for this calculation. Note that total expenses include books, supplies, transportation and other costs.

2 Fidelity Investments Grandparents and College Savings Study, June 2014