")

SASKATOON, Saskatchewan--(BUSINESS WIRE)--Gensource Potash Corporation (“Gensource” or the “Company”) (TSX.V: GSP) is pleased to announce the results from the detailed feasibility study (“Study” or “FS”) for its Vanguard One Potash Project (“Vanguard”, or “Project”) in Saskatchewan.

The FS was completed by an integrated team, consisting of ENGCOMP Engineering and Computing Professionals Inc. of Saskatoon, SK and its engineering sub-consultants, South East Construction L.P. of Esterhazy, SK, Terra Modelling Services Inc. of Dalmeny, SK, Innovare Technologies Ltd. of Carlyle, SK, Golder Associates Ltd. of Saskatoon, SK, and Whiting Equipment Canada Inc. of Welland, ON. These companies are experts in their respective fields, and bring best-in-class Saskatchewan potash knowledge and experience to the Project. The integrated team joined together the engineers, designers, fabricators, and construction contractors to collaborate on the design, constructability, and optimization of key projects elements. This integrated approach supports the development of a solid capital cost estimate and project schedule, which bolsters confidence in the overall Study.

Gensource’s President & CEO, Mike Ferguson, said, “We are delighted to have completed the feasibility study for Vanguard, and are even more pleased that, as we dig deeper into the detail, the chosen mining and processing methods continue to affirm that Gensource has selected the right approach to potash production. Not only do we have a world class resource, but the project also provides a strong return on investment, in part because it is small and easily scalable, and all the while setting a new bar for environmental responsibility in the development of new potash production. The results of the Study speak for themselves: even in this time of low potash prices, and even with Gensource’s conservative assumptions on potash price into the future and on-going sustaining capital costs for the operation, the project is technically and economically robust. We are excited to take the Vanguard Project to the next step – confirming the construction financing and then into construction and ultimately, operation. We are more convinced more than ever that this is the way to produce potash in the 21st century.”

The Study was initiated in October 2016 with a planned completion date of Q2 2017, a goal which has now been met. Effort invested in engineering, design, management, procurement, estimating, planning, and report preparation exceeded 20,000 hours over the Study period. A National Instrument (NI) 43-101 technical report will be filed within 45 days of this news release, and will also be available on the Company’s website.

The FS was undertaken, financed and completed directly by Gensource Potash Corporation and it represents the next step in the Company’s drive to bring new technologies and new business approaches to the potash industry. It is based on engineering and cost estimating methods and levels of effort sufficient to support an AACE International Class 3 capital cost estimate – key to adding certainty to both the engineering design as well as construction costs and schedule for the project.

As background, the Company’s new “business + technology” approach to potash utilizes a small-scale production model that has the following features:

- It allows for vertical integration of the mine with an identified market partner,

- It facilitates lower capital expenditures (CAPEX), and is therefore more readily financed, together with site-based operating costs (OPEX) that are at the low end of the lowest quartile of all potash operations globally, and

- The selective solution mining techniques continue to exhibit a significantly reduced environmental footprint, with no salt tailings on surface, no brine ponds or other brine control structures, and no requirement for surface water consumption. Consequently, the Company hopes that permitting the Vanguard One project will be easier than a typical potash project.

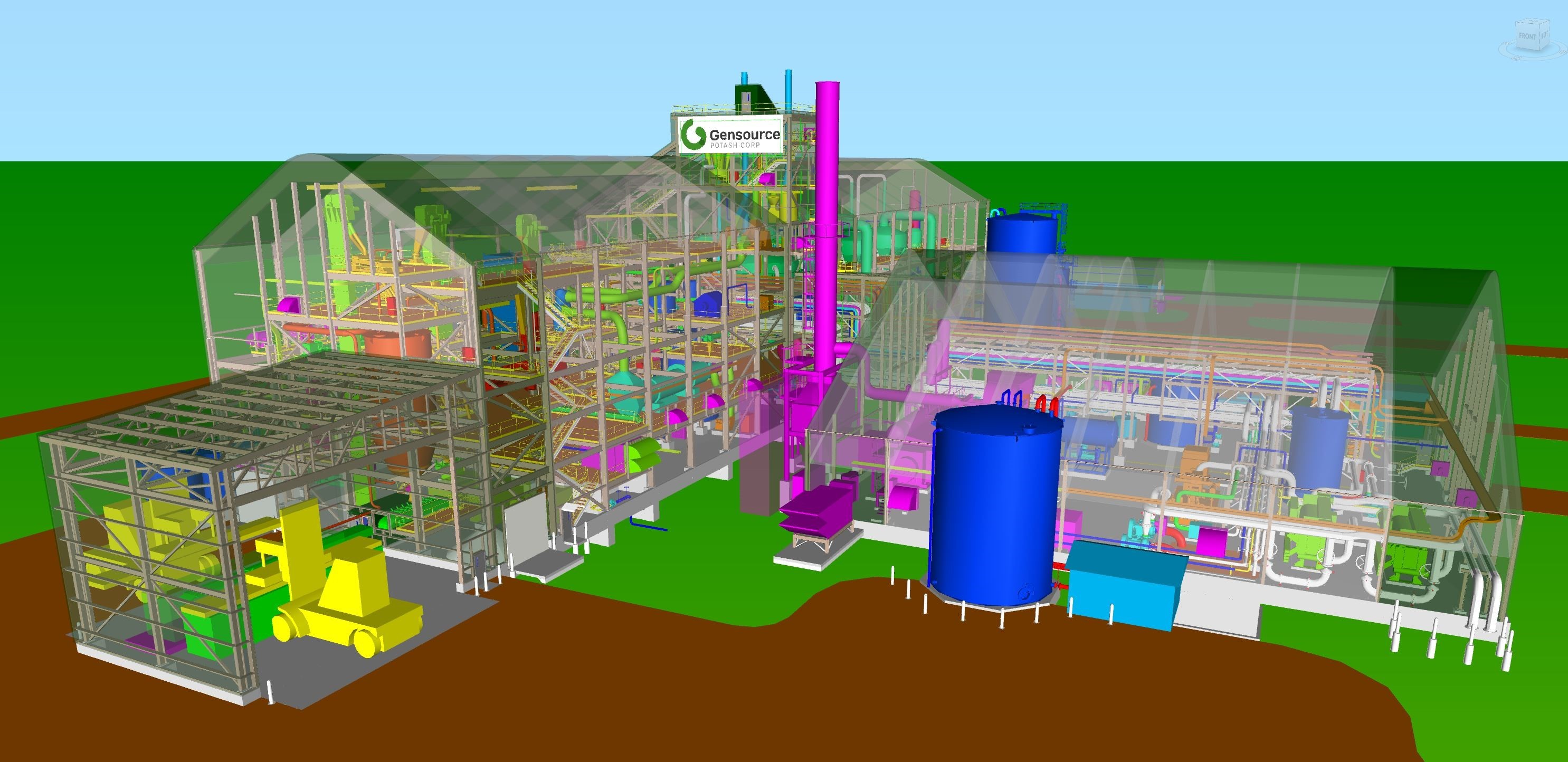

See *Figure 1: 3D Model of the Gensource Small Scale Potash Facility

FS SUMMARY

The following are general highlights from the

Study:

General:

Table 1: FS Highlights

| Parameter | Results | |

| Project capacity: | 250,000 t/y final product, standard grade (“MOP”, or “potash”) | |

| Mine life: | See Geology section below | |

| Mining method: | Selective dissolution using horizontal caverns | |

| Processing: | Cooling crystallization incorporating innovative energy efficiency measures | |

| Product storage: | Intermodal shipping containers covering 7 days of operation (typical) on rotation, with an additional 14 days of container storage available on-site as needed | |

| Product Transport: | $100/t transportation and logistics to overseas destination included in the economic analysis, based on quotations received | |

| CAPEX: | $CAD 279M including contingency – (~$US 210M at today’s nominal exchange rate of 1.33) | |

| OPEX: | $CAD 53.23/t final product ($US 39.54/t at today’s nominal CAD/US exchange rate of 1.345 as set by the Bank of Canada May 25, 2017). The major components of OPEX are natural gas delivered to site at $CAD 3.71/GJ and operating personnel count of 46 full time staff. All operating costs were inflated at 1.5% per annum. Natural gas prices were taken as a 5-year forecasted average as per Sproule Associates Ltd., April 2017 and inflated annually. | |

| Sustaining CAPEX: | Average annual sustaining capital of $CAD 3.29 million ($US 2.91 million) or $CAD 15.68/t ($US 11.65/t) per year includes full cavern replacement every 14 years, annual well work-overs and 2% of plant site equipment. Sustaining capital is inflated at 1.5% per annum. | |

| Construction: | 22-month construction period, peak construction work force of approximately 150. |

CAPEX:

The total project capital

construction cost is estimated at $CAD 279M, including contingency –

(~$US 210M at today’s nominal exchange rate of 1.345)

The following is a summary of the Class 3, Capital Cost Estimate, summarized by project area:

Table 2: CCE Summary

| AREA | $CAD | ||

| Mining | $ | 23,738,000 | |

| Wellfield | $ | 17,304,000 | |

| Process Plant | $ | 70,610,000 | |

| Product Storage & Loadout | $ | 957,000 | |

| Site Infrastructure | $ | 27,297,000 | |

| Offsites | $ | 6,877,000 | |

| Non-Process Facilities | $ | 29,550,000 | |

| Project Indirects | $ | 77,972,000 | |

| TOTAL (Pre-Contingency)* | $ | 254,305,000 | |

| Contingency (P75) | $ | 25,564,000 | |

| GRAND TOTAL | $ | 279,869,000 | |

*A statistical analysis was completed, using Palisade’s @Risk software, to yield a range of probable project costs and aid in the determination of a probabilistic contingency to apply to the project. A contingency of $25,564,000 was selected, representing the value from the 75th percentile of the analysis output. The 75th percentile (or Level of Confidence) value means that 75% of the total project cost outputs from the statistical analysis were equal to or less than this value.

Economic Analysis:

The financial

performance of the project is shown in table below, for a range of

product prices and costs of capital.

Table 3: Financial Performance Post Potash Production Tax, Royalties, Levies and Surcharges

|

Price/Tonne |

Project |

NPV @ | Opp Margin |

Payback |

||||||||

| 6.00% | 8.00% | 10.00% | ||||||||||

| $225 | 9.83% | $ 135,019,994 | $49,178,315 | ($3,494,593) | 78.20% | 10.00 | ||||||

| $250 | 12.10% | $ 220,792,606 | $ 112,507,467 | $45,070,745 | 79.88% | 8.00 | ||||||

| $275 | 14.26% | $ 305,333,691 | $ 174,755,710 | $92,696,697 | 81.34% | 7.00 | ||||||

| $300 | 16.31% | $ 388,540,731 | $ 235,822,250 | $139,282,488 | 82.42% | 6.30 | ||||||

| $325 | 18.30% | $ 471,047,175 | $ 296,232,842 | $ 185,262,292 | 83.45% | 5.25 | ||||||

| $350 | 20.24% | $ 553,536,139 | $ 356,569,799 | $ 231,132,156 | 83.45% | 5.00 | ||||||

| $375 | 22.11% | $ 635,518,277 | $ 416,435,959 | $ 276,567,150 | 85.00% | 4.80 | ||||||

| $400 | 23.97% | $ 717,756,211 | $ 476,482,843 | $ 322,125,403 | 85.78% | 4.70 | ||||||

| $425 | 25.75% | $ 799,288,171 | $ 535,897,782 | $ 367,117,241 | 86.36% | 4.30 | ||||||

| $450 | 27.50% | $ 880,785,576 | $ 595,272,298 | $ 412,064,642 | 86.89% | 4.00 | ||||||

| $475 | 29.22% | $ 962,232,078 | $ 654,587,267 | $ 456,946,581 | 87.35% | 3.80 | ||||||

| $500 | 30.92% | $ 1,043,678,579 | $ 713,902,236 | $ 501,828,519 | 87.77% | 3.00 | ||||||

At a base case potash price of $US 300/t, a 45-year economic project life, 1.5% operating cost inflation, $CAD 100/t ($US 74.29) shipping cost to East Asia, operating costs of $CAD 53.23/t ($US 39.54), sustaining capital reinvestment totaling $CAD 15.68/t ($US 11.65/t) and a constant exchange rate of 1.30 $CAD/$US the financial performance of the project can be summarized as:

Table 4: Financial Performance Summary

| Indicator |

Pre Sask. Profit |

Post Sask. Profit |

||

| NPV8 | $329,403,545 | $235,822,250 | ||

| IRR | 18.32% | 16.31% |

The following defines the input parameters and assumptions used in the discounted cash flow model (DCFM) for the Gensource Vanguard project:

- The economic analysis is based on a 100% equity scenario.

- Potash production is 100% standard grade.

- Cash-flow model constructed in $CAD.

- Base-case pricing for standard product is $US 300/t, CFR Asia starting in 2019 with an escalation of 1%.

- Operating costs and sustaining capital reinvestment costs have been inflated at 1.5% per annum.

- There will be no expansion beyond 250,000 t/y.

- Consideration was given to the expected timing of construction expenses.

- Operating costs and sustaining capital costs are included in the model.

- Annual sustaining Capital cost averages $CAD 15.68/t ($US $11.65/t)

- Insurance during construction is included in the models.

- The cash flows include Saskatchewan Resource Surcharge (3% of revenue), Provincial Royalties (4.4% of K2O), and Saskatchewan Potash Production Tax.

- The economic model includes a 3% per annum “Other Royalty” on net revenue.

- Transportation costs to destination are assumed CFR Asia. $CAD 100/t has been included under the OPEX section of the cash flow.

- Revenue generated from future potash sales are converted into $CAD at a long-term historical exchange $CAD:$US of 1.30.

- Working capital requirements of $CAD 2.66/t.

- Head office general and administrative expenses of 1.1% of Revenue or $CAD 5/t.

- Spot $CAD:$US exchange rate used as of the date of this report is 1.345 as set by the Bank of Canada May 25, 2017.

Schedule:

Gensource’s small-scale

concept facilitates a development timeline of approximately two years

from construction to first production.

Conclusions and Recommendations:

The

conclusions and recommendations made in the report are to:

- Complete the environmental assessment approval process and move into the permitting phase to ensure the appropriate permits, approvals, and licenses are obtained to advance the Project into the construction phase, followed by operations.

- Complete the full project financing package

- Initiate procurement for key long-lead items

- Initiate detailed engineering including final trade-off studies.

- Complete advanced modelling and testing of cavern temperature and dissolution rates

FURTHER FS DETAIL

Geology:

From

the 17Feb2017 NI 43-101 Technical Report, the following tables define

the Indicated and Inferred Resource in the Vanguard area (Base Case

Highlighted). Note that the Indicated Resource data is inclusive of the

Reserve data listed in Table 7.

Table 5: Indicated Resource

| INDICATED RESOURCE | ||||||||||||||||||||

| Member |

Sub- |

Total KCl |

Carnallite |

Insoluble |

Average |

Total |

Sylvinite |

Sylvite |

Sylvite |

Sylvite |

||||||||||

| Weight % | Weight % | Weight % | meters | Weight % | Million tons | Million tons | Million tons | Million tons | ||||||||||||

|

Patience

|

PLM1 | 39.03 | 0.75 | 6.21 | 4.40 | 290.00 | 232.00 | 27.16 | 36.22 | 45.27 | ||||||||||

| PLM2 | 28.91 | 0.60 | 7.03 | 3.65 | 240.07 | 192.06 | 16.66 | 22.21 | 27.76 | |||||||||||

| PLM3 | 39.33 | 0.60 | 9.24 | 2.91 | 145.84 | 116.67 | 13.77 | 18.36 | 22.94 | |||||||||||

| PLM4 | 36.32 | 0.67 | 10.43 | 1.90 | 125.48 | 100.38 | 10.94 | 14.58 | 18.23 | |||||||||||

| Sub-Total | 35.63 | 0.67 | 7.67 | 12.86 | 801.39 | 641.11 | 68.53 | 91.37 | 114.21 | |||||||||||

|

Belle Plaine |

BPM1 | 37.82 | 0.98 | 6.20 | 0.79 | 35.24 | 28.19 | 3.20 | 4.26 | 5.33 | ||||||||||

| BPM2 | 41.18 | 0.44 | 2.69 | 2.06 | 81.79 | 65.43 | 8.08 | 10.78 | 13.47 | |||||||||||

| BPM3 | 33.36 | 0.45 | 2.38 | 1.27 | 59.09 | 47.27 | 4.73 | 6.31 | 7.88 | |||||||||||

| BPM4 | 28.70 | 0.70 | 3.58 | 2.00 | 130.12 | 104.09 | 8.96 | 11.95 | 14.94 | |||||||||||

| BPM5 | 35.65 | 1.40 | 4.83 | 1.26 | 82.05 | 65.64 | 7.02 | 9.36 | 11.70 | |||||||||||

| BPM6 | 26.53 | 1.62 | 2.00 | 1.70 | 110.51 | 88.41 | 7.04 | 9.38 | 11.73 | |||||||||||

| BPM7 | 55.73 | 1.64 | 0.63 | 0.45 | 8.58 | 6.86 | 1.15 | 1.53 | 1.91 | |||||||||||

| Sub-Total | 33.00 | 0.98 | 3.29 | 9.53 | 507.37 | 405.89 | 40.18 | 53.57 | 66.96 | |||||||||||

| Total | 1047.01 | 108.70 | 144.94 | 181.17 | ||||||||||||||||

| Base Case | ||||||||||||||||||||

Table 6: Indicated Resource

| INDICATED RESOURCE | ||||||||||||||||||||

| Member |

Sub- |

Total KCl |

Carnallite |

Insoluble |

Average |

Total |

Sylvinite |

Sylvite |

Sylvite |

Sylvite |

||||||||||

| Weight % | Weight % | Weight % | meters | Weight % | Million tons | Million tons | Million tons | Million tons | ||||||||||||

|

Patience |

PLM1 | 39.10 | 0.69 | 6.61 | 4.27 | 743.30 | 557.47 | 65.39 | 87.19 | 108.99 | ||||||||||

| PLM2 | 29.59 | 0.73 | 8.52 | 2.82 | 441.02 | 330.77 | 29.36 | 39.15 | 48.94 | |||||||||||

| PLM3 | 35.09 | 0.83 | 11.58 | 2.39 | 296.75 | 222.56 | 23.43 | 31.24 | 39.05 | |||||||||||

| PLM4 | 36.86 | 0.65 | 9.38 | 2.29 | 336.86 | 252.64 | 27.94 | 37.25 | 46.56 | |||||||||||

| Sub-Total | 35.72 | 0.72 | 8.40 | 11.77 | 1817.93 | 1454.34 | 146.12 | 194.83 | 243.53 | |||||||||||

|

Belle Plaine

|

BPM1 | 54.80 | 4.16 | 0.72 | 0.83 | 70.53 | 52.90 | 8.70 | 11.60 | 14.49 | ||||||||||

| BPM2 | 27.29 | 3.82 | 2.19 | 2.07 | 190.20 | 142.65 | 11.68 | 15.57 | 19.46 | |||||||||||

| BPM3 | 35.02 | 3.22 | 4.77 | 1.23 | 165.83 | 124.37 | 13.07 | 17.42 | 21.78 | |||||||||||

| BPM4 | 28.55 | 0.78 | 3.68 | 2.00 | 343.42 | 257.57 | 22.06 | 29.41 | 36.77 | |||||||||||

| BPM5 | 32.18 | 0.56 | 2.58 | 1.31 | 224.79 | 168.60 | 16.28 | 21.70 | 27.13 | |||||||||||

| BPM6 | 41.04 | 0.47 | 2.75 | 1.61 | 276.84 | 207.63 | 25.56 | 34.08 | 42.61 | |||||||||||

| BPM7 | 42.28 | 1.05 | 8.20 | 0.59 | 40.33 | 30.25 | 3.84 | 5.12 | 6.39 | |||||||||||

| Sub-Total | 34.28 | 1.62 | 3.20 | 9.64 | 1311.95 | 983.96 | 101.18 | 134.91 | 168.63 | |||||||||||

| Total | 2438.31 | 247.30 | 329.73 | 412.17 | ||||||||||||||||

| Base Case | ||||||||||||||||||||

Based on the geological work completed to date, including the 3D seismic program just completed, the following Reserve is defined as the base case for the Vanguard One Project FS:

Table 7: Proven & Probable Reserve

|

Potash Sub-Member |

Reserve |

Grade KCl (Weight % KCl)* |

Recoverable |

|||

| PLM1 | Proven | 44.0 | 5.19 | |||

| Probable | 41.2 | 2.67 |

*cutoffs: 24.6% KCl, 6% Carnallite, no insoluble or thickness cutoff

Cautionary Notes on Geology:

- The above Reserve data represents only the base case for the FS for the Vanguard One project. Since the mine plan is focused initially only on the Patience Lake sub-member 1 (PLM1) within the Patience Lake member of the Prairie Evaporite, and focuses on a relatively small component of the area of 3D seismic coverage, only a small portion of the overall Resource is converted to Reserve for the base case.

- Modelling and analysis work is not 100% complete at the time of this news release, and on that basis, the final Reserve data is subject to change in the final 43-101 Technical Report, however the QP does not anticipate that the base case mineral reserve will change materially.

Mining:

Vanguard will implement a

selective mining approach, using horizontal caverns. A total of 6

caverns, covering nominally 2 sections (1 section = 1 square mile) of

mineral resource will be required to attain the planned 250,000 t/a

production rate. Calculated cavern life, using only the PLM1 sub-member

of the Patience Lake member of the Prairie Evaporite formation (as

defined in the Technical Report) is 11.9 years. Allowances for cavern

replacement costs and pipeline extension costs have been made in the

sustaining capital estimate.

Processing:

The process plant is

designed to recover 250,000 metric tons per annum of standard grade

Muriate of Potash (MOP) from the solution mining operation. The

production of potash product (nominally 96% purity KCl) is accomplished

by the removal of KCl from the recirculating brine stream by temperature

reduction. Temperature reduction is accomplished by a vacuum

crystallizer, followed by a surface cooling crystallizer operation. The

brine stream continuously recirculates between the solution mining

caverns and the process plant, picking up KCl in the caverns and

crystallizing it into solid KCl in the process plant.

Utilities:

Plant utilities, including

steam, natural gas, water, power, etc. are distributed from central

locations to each process/mining unit operation.

All power required on-site will be self-generated by a natural gas fired steam turbine-driven generator. Construction Power and Temporary “backup” power will be provided by a 25kV, 2MVA service from SaskPower.

Based on field drilling investigation and aquifer modelling completed during the study it has been determined that raw water for the entire site can adequately be supplied from a local and accessible aquifer should deep brackish sources not be identified.

Off-site utilities include, natural gas, fibre optic line, and potentially potable water. For natural gas to the site, a new 150mm diameter pipeline is to be supplied by an existing 400mm diameter TransGas transmission pipeline, located approximately 10 kilometers north of the project area.

Product Loading & Handling:

Gensource

will direct load product into intermodal shipping containers, utilizing

these containers as the primary means of loading, storing, and moving

product at the mine site and to the end customers. No on-site or tide

water bulk storage and handling facilities/systems are required as a

result. Direct loading into containers has the added benefit of

minimizing product handling, reducing product degradation and losses as

a result. It also allows for easier transport and handling for the end

customer.

Transportation and Logistics:

A plant

site rail spur is planned, thereby allowing all product to be

transported in intermodal shipping containers by rail, avoiding

heavy-haul truck traffic on the exiting road network.

The cost of ocean freight, including the cost to move the product from a West coast port in North America to an East coast port in Asia has been factored into the operating cost estimate.

Environmental & Regulatory:

Gensource

has engaged Golder Associates to prepare a Technical Proposal for the

Vanguard One Project, to be submitted to the Environmental Assessment &

Stewardship Branch of the Ministry of Environment. This submission is

currently being completed and will be submitted in June 2017.

The scientific and technical information contained in this news release is based on the actual feasibility study work and data produced. Each named company participating in the FS has reviewed and approved the content of this news release. Gensource’s independent QP for this work, Mr. Louis Fourie, P.Geo., Pri. Sci. Nat., of Terra Modelling Services Inc., has reviewed and approved the content of this news release.

About ENGCOMP

ENGCOMP is a multi-discipline engineering

consulting firm located in Saskatoon, SK. With more than 13 years of

establishment in the heart of Saskatchewan's potash industry, ENGCOMP is

a leader in the delivery of engineering for potash processing

facilities. For more information see www.engcomp.ca.

About South East Construction

SECON is a multi-discipline

construction and service company with its head office in Esterhazy,

Saskatchewan. By delivering projects safely with uncompromised

integrity, SEC has proven to be a preferred contractor in the province.

For more information see www.secon.ca.

About Terra Modelling Services

Terra Modelling Services Inc.

is a geological consulting company based in Dalmeny, Saskatchewan, with

specific expertise in potash and related minerals, as well as diamonds

and kimberlites. For further information about Terra Modelling Services,

email: louis.fourie@terramodellingservices.ca

About Innovare

Innovare Technologies Ltd. is a consulting

firm, specialized in drilling, solution mining and processing

technologies for potash mining projects. The three principals of the

company have a combined 100+ years’ experience, much of that in the

potash industry, and have successfully developed potash projects in

Saskatchewan. Based on solution mining and processing concepts developed

in other commodities dating back to 1997, the principals realized the

potential applications of these concepts and began to adapt them to the

extraction of potash.

About Golder

Established in 1960, Golder is a global,

employee-owned group of companies driven by our purpose to engineer

earth’s development while preserving earth’s integrity. From over 165

offices worldwide, our more than 6,500 employees help our clients find

sustainable solutions to the challenges society faces today. Golder has

been working in Saskatchewan since 1970, and Golder’s potash experience

includes environmental assessment for greenfield potash mines, tailings

management, and geotechnical investigations for mining infrastructure.

About Whiting

Whiting Equipment Canada Inc. is a licensee of

the internationally recognized and accepted line of Swenson Technology,

Inc., supplying evaporation and crystallization equipment and systems

for the chemical processing industry. Our equipment is used in various

applications including salt, potash and sodium chlorate. Typical scope

of supply ranges from engineering and feasibility studies to a fully

integrated process including structural steel, vessels, piping,

instrumentation, and electrical components. For more information, visit www.whiting.ca.

About Gensource

Gensource is based in Saskatoon,

Saskatchewan and is focused on developing the next potash production

facility in that province. Gensource’s President and CEO, Mike Ferguson,

P.Eng., has assembled a management and technical team with direct and

specific expertise and experience in potash development in Saskatchewan.

Gensource operates under a business plan that has two key components - vertical integration with the market to ensure that all production capacity built is directed to a specific market, eliminating market-side risk; and, technical innovation which will allow for a small and economic potash production facility, the output of which can then be directed to a single, specific market. For more information, visit www.gensource.ca

Neither TSX Venture Exchange nor its Regulation Services Provider (as that term is defined in the policies of the TSX Venture Exchange) accepts responsibility for the adequacy or accuracy of this release.

Caution Regarding Forward-Looking Statements

This news release may contain forward looking information and Gensource cautions readers that forward looking information is based on certain assumptions and risk factors that could cause actual results to differ materially from the expectations of Gensource included in this news release. This news release includes certain "forward-looking statements”, which often, but not always, can be identified by the use of words such as "believes", "anticipates", "expects", "estimates", "may", "could", "would", "will", or "plan". These statements are based on information currently available to Gensource and Gensource provides no assurance that actual results will meet management's expectations. Forward-looking statements include estimates and statements with respect to Gensource’s future plans, objectives or goals, to the effect that Gensource or management expects a stated condition or result to occur, including funding and development pursuant to the definitive joint venture agreement with the EGME, the expected timing for release of a reserve estimate and a feasibility study and whether or not the study will conclude that mineral production is feasible on a technical or economic basis, and the establishment of vertical integration partnerships and the sourcing of end use potash purchasers. Since forward-looking statements are based on assumptions and address future events and conditions, by their very nature they involve inherent risks and uncertainties. Actual results relating to, among other things, funding and development pursuant to a definitive joint venture agreement with the EGME, results of exploration, the economics of processing methods, project development, reclamation and capital costs of Gensource’s mineral properties, the ability to complete a feasibility which supports the technical and economic viability of mineral production, Gensource’s financial condition and prospects, the ability to establish viable vertical integration partnerships and the sourcing of end use potash purchasers, could differ materially from those currently anticipated in such statements for many reasons such as: failure to obtain funding and undertake development pursuant to the definitive joint venture agreement with the EGME; an inability to finance and/or complete an update of the resource estimate to a reserve estimate, and a feasibility study which supports the technical and economic viability of mineral production; changes in general economic conditions and conditions in the financial markets; the ability to find distributors and source off-take agreements; changes in demand and prices for potash; litigation, legislative, environmental and other judicial, regulatory, political and competitive developments; technological and operational difficulties encountered in connection with Gensource’s activities; and other matters discussed in this news release and in filings made with securities regulators. This list is not exhaustive of the factors that may affect any of Gensource’s forward-looking statements. These and other factors should be considered carefully and readers should not place undue reliance on Gensource’s forward-looking statements. Gensource does not undertake to update any forward-looking statement that may be made from time to time by Gensource or on its behalf, except in accordance with applicable securities laws.