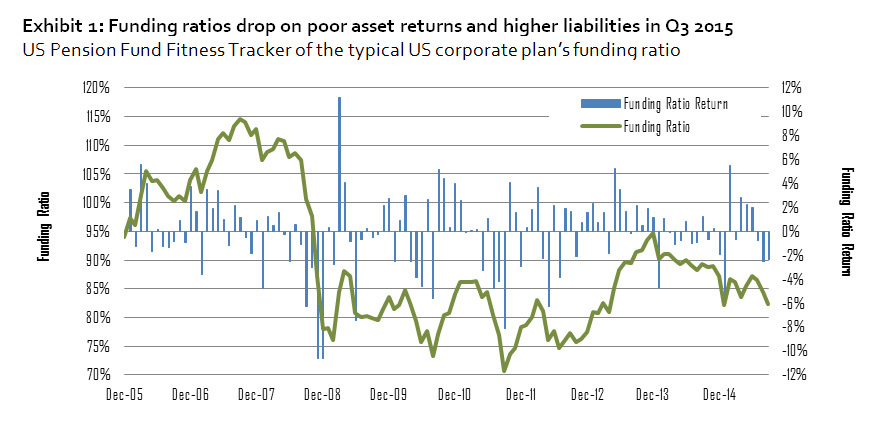

CHICAGO--(BUSINESS WIRE)--The UBS Global Asset Management US Pension Fund Fitness Tracker saw the funding ratio of the typical corporate US pension plan fall by approximately five percentage points to 82% in the third quarter of 2015.

"In the third quarter, we saw the funding ratios of pension plans decrease as both investment returns as well as liability returns were unfavorable. Over the course of the full year many plans have seen a substantial aggregate negative net effect on the overall funding ratios. Because of that, some plans have started to re-risk due to upward adjustments of expected return targets. Other plans have not yet taken action, but we do expect more shifts in allocations given the decreased levels of funding ratios. We continue to advise our clients on appropriate strategy and timing of implementation of new allocation targets," said Frank van Etten, head of Client Solutions at UBS Global Asset Management.

Negative investment returns of -3.1%, along with positive liability returns of 2.5%, led to nearly a 5 percentage point drop in funding ratios over the third quarter. Widening credit spreads failed to offset lower Treasury yields this quarter. These estimates are based on the average corporate plan’s reported asset allocation weightings from the UBS Global Asset Management Pension 500 Database and publicly available benchmark information.

In the third quarter of the year, the investor focus shifted from Greece to China, with the latter having a much more pronounced market impact. China’s decision to bring the yuan closer to a market-based valuation mechanism and its ensuing weakening triggered a selloff in risk assets globally. Concerns about a major slowdown in the Chinese economy caused investors to lower their global growth expectations, which exacerbated the flight to quality.

In the US, despite continued economic recovery supported by improving data, the Federal Reserve surprised market participants by its decision not to raise the fed funds rate. In light of supportive data, most investors expected a liftoff, given indications throughout the year that the decision to hike would be data-dependent...yet, the Fed introduced another variable in the equation when it made reference to the global economic conditions. That being said, the majority of members in the Federal Open Market Committee have indicated that they still expect the fed funds rate to be raised in 2015.

During the third quarter, equity markets globally delivered strong negative performance. The S&P 500 Index ended the quarter down with a total return of -6.44%. The Euro Stoxx Total Return Index was down at -8.05%, in US dollar (USD) terms, over the quarter. The MSCI Emerging Markets Total Return Index ended the quarter 17.78% lower in USD terms.

The yield on 10-year US Treasury Notes ended the quarter down 31 basis points (bps) at 2.04%. The yield on 30-year US Treasury bonds decreased 27 bps, ending at 2.85%. High-quality corporate bond credit spreads, as measured by the Barclays Long Credit A+ option-adjusted spread, ended the quarter 16 bps wider. As a result, pension discount rates (which are based on the yield of high-quality investment grade corporate bonds) decreased over the quarter. The passage of time caused liabilities for a typical pension plan to increase by about one percentage point over the quarter. Together, these effects caused liabilities to increase 2.5% for the quarter. (Please see disclosures for assumptions and methodology.)

Disclosures and methodology

Funding ratio

Funding ratios measure a pension fund’s ability to meet future payout obligations to plan participants. The main factors impacting the funding ratio of a typical US defined benefit plan are equity market returns, which grow (or shrink) the asset pool from which plan participants’ benefits are paid, and liability returns, which move inversely to interest rates.

Liability indices: Methodology

Pension Protection Act (PPA) liability returns are approximated by the Barclays Capital US Long Credit A-AAA Index. This index broadly reflects the duration and credit characteristics of the PPA discount curve that is used to discount expected pension benefit payments for US defined benefit pension plans.

Asset index: Methodology

UBS Global Asset Management approximates the return for the ”typical” US defined benefit plan using the reported asset allocation of the UBS Global Asset Management Pension 500 Database. The series is constructed using the aggregate asset allocation weightings and publicly available benchmark information, with geometrically linked monthly total returns.

Pension Fund Fitness Tracker: Methodology

The US Pension Fund Fitness Tracker is the ratio of the asset index over the liability index. Assuming all other factors remain constant, it combines asset and liability returns, and measures the impact of a “typical” investment strategy on the funding ratio of a model defined benefit plan in the US due to interest rollup, change in interest rates and typical asset performance, but excludes unique plan factors, such as service cost and benefit payments. The impact of changes in mortality tables in 2014 was estimated to be a 6% increase in liabilities and was reflected in Q2 2015.

The UBS Global Asset Management Pension 500 Database

The UBS Global Asset Management Pension 500 Database is a proprietary database that is based on the analysis of 500 public companies sponsoring large defined benefit plans. The information was extracted from the companies’ 10-K statements, and therefore represents generally accepted accounting principles (GAAP) information. The study may include figures for companies’ nonqualified and foreign plans, both of which are not subject to ERISA.

The aggregate asset allocation is based on an equally weighted average of the 500 companies included in the database. The aggregate asset allocation includes equities, fixed income, hedge funds, private equity, real estate and cash.

NOTES TO EDITORS

About Global Asset Management

Global Asset Management is a large-scale asset manager with well diversified businesses across regions and client segments. It serves third-party institutional and wholesale clients, as well as clients of UBS’s wealth management businesses with a broad range of investment capabilities and styles across all major traditional and alternative asset classes. Complementing the investment offering, the fund services unit provides fund administration services for UBS and third-party funds.

About UBS

UBS is committed to providing private, institutional and corporate clients worldwide, as well as retail clients in Switzerland, with superior financial advice and solutions while generating attractive and sustainable returns for shareholders. Its strategy centers on its Wealth Management and Wealth Management Americas businesses and its leading universal bank in Switzerland, complemented by its Global Asset Management business and its Investment Bank. These businesses share three key characteristics: they benefit from a strong competitive position in their targeted markets, are capital-efficient, and offer a superior structural growth and profitability outlook. UBS's strategy builds on the strengths of all of its businesses and focuses its efforts on areas in which it excels, while seeking to capitalize on the compelling growth prospects in the businesses and regions in which it operates. Capital strength is the foundation of its success.

Headquartered in Zurich, Switzerland, UBS has offices in more than 50 countries, including all major financial centers, and approximately 60,000 employees. UBS Group AG is the holding company of the UBS Group. Under Swiss company law, UBS Group AG is organized as an Aktiengesellschaft, a corporation that has issued shares of common stock to investors. The operational structure of the Group comprises the Corporate Center and five business divisions: Wealth Management, Wealth Management Americas, Retail & Corporate, Global Asset Management and the Investment Bank.