")

balance than lose weight (Graphic: Business Wire)")

")

")

plan participants")

")

participant education and advice (Photo: Business Wire)")

SAN FRANCISCO--(BUSINESS WIRE)--A new survey illustrates the vital role of 401(k) plans in helping workers save for retirement, but also identifies obstacles to saving effectively and a strong desire among participants for professional help in choosing the right investments. There is also widespread belief that retirement should be a major issue discussed by the presidential candidates in the upcoming debates.

Wealth & Health

The nationwide survey of 1,000 401(k) plan participants, commissioned by Schwab Retirement Plan Services, finds that a 401(k) is viewed as an essential workplace benefit and that people are taking saving for retirement very seriously in much the same way they strive to manage their health. In fact, 90 percent of respondents said they would think twice about taking a job if the company did not offer a 401(k) plan. The survey also found:

- More than two-thirds (68%) consider making the best 401(k) investment choices a key priority – even more so than staying in shape (59%).

- 73 percent would rather have their 401(k) balance grow by 15 percent this year than lose 15 pounds.

- Participants pay more attention to 401(k) investment fees (64%) than ATM fees (60%), airline baggage fees (50%) or gym sign-up fees (49%).

“When it comes to retirement, there’s been a significant shift of responsibility from employer to employee over the past 30 years, making the 401(k) plan a critical part of the retirement system,” said Steve Anderson, head of Schwab Retirement Plan Services. “Our survey found only one in five participants would be confident in their ability to save for retirement without a 401(k) plan. In fact, participants worry as much about having enough money to enjoy retirement as they do about being healthy enough to enjoy retirement.”

Retirement Roadblocks

While it’s clear that participants recognize the importance of saving in a 401(k) plan, survey respondents also note that saving can be difficult and cite a number of concerns and competing priorities that interfere with their ability to meet retirement goals.

More than one-third (35%) say they aren’t saving more for tomorrow because they are unwilling to sacrifice their quality of life today – expenditures like dinners out and vacations. Other top obstacles to retirement saving include paying for unexpected expenses (31%), covering basic monthly bills (31%), paying off credit card debt (24%) and saving for education (22%). Other key findings include:

- While 90 percent know what their ideal credit score should be, only 58 percent know how much they should save for a comfortable retirement.

- Nearly half (47%) say that materials explaining their 401(k) plan investments are more confusing than materials explaining their health & medical benefits.

- Roughly three in ten (29%) have either decreased or not made any changes to their 401(k) savings rate in the last two years.

“Today, many employers are designing their 401(k) plans to better address savings obstacles and help their employees take more control of their investments,” noted Anderson. “These employers are at the forefront, using automatic enrollment, automatic savings rate increases and automatic investment advice to help their employees prepare for retirement. The industry needs to focus more on plan design features like these if we are to further our goal of improving participant outcomes.”

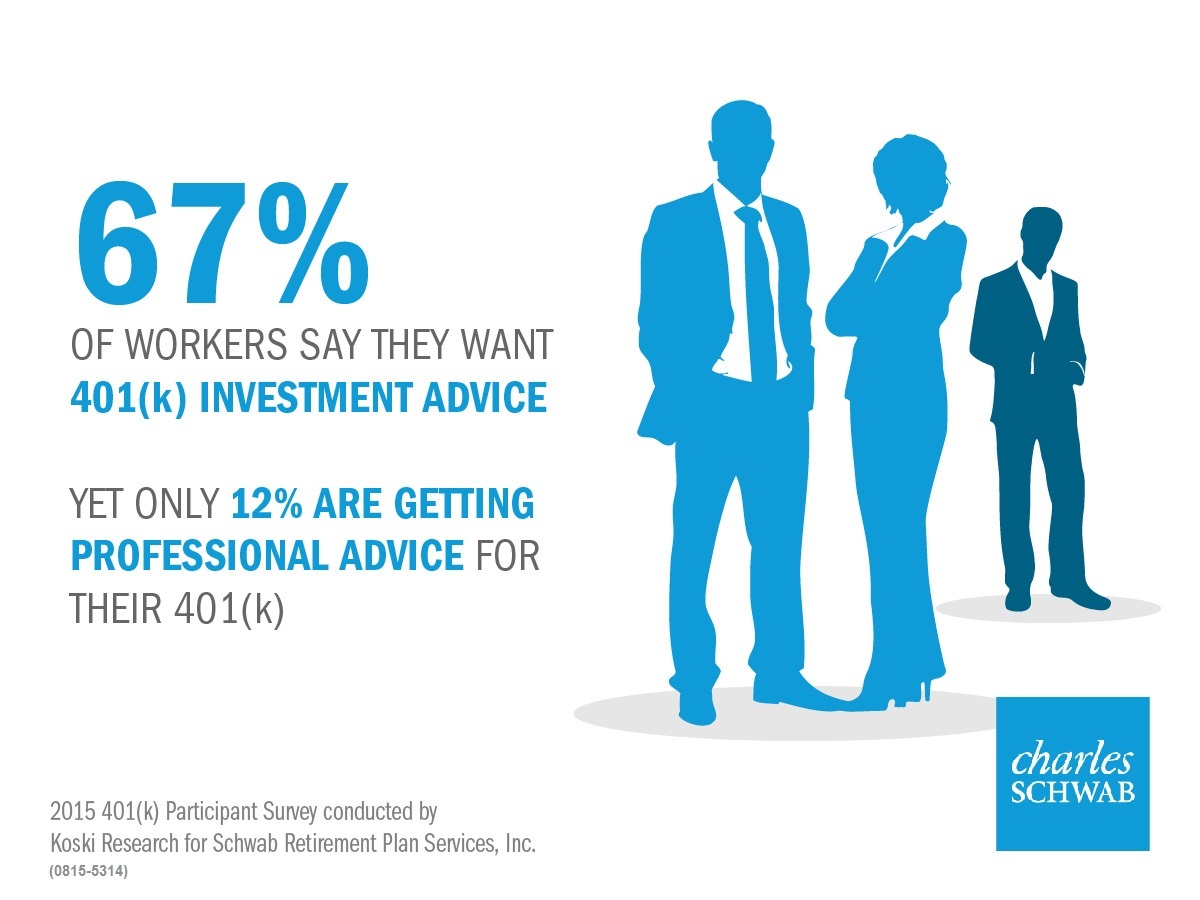

According to the survey, professional 401(k) investment advice is something that participants say they value, even though relatively few are actually using it. For example:

- 67 percent want personalized investment advice for their 401(k) and 79 percent say they are likely to seek out professional help for making the best 401(k) investment choices; and

- 73 percent say they would be very or extremely confident in their ability to make the right investment decisions with the help of a financial professional, versus only 44 percent who would feel that same level of confidence on their own;

- Yet only 12 percent of participants questioned are currently getting professional advice for their 401(k), even though nearly half (49%) say they’d expect better performance if they used advice.

“Most participants want 401(k) advice, but whether because of inertia or discomfort, many don’t take that first step of asking for help,” said Catherine Golladay, vice president of participant services and administration at Schwab Retirement Plan Services. “We’ve observed that when advice is built into the plan so that participants start off with it and are free to opt out if they wish, nearly 86% stick with it.1 That can make a big difference.” Research from Morningstar Associates, LLC suggests that participants receiving advice as part of a managed account service could end up with nearly 40 percent more income in retirement.2

Politics & Pocketbooks

While the survey found that hardly any respondents expect to rely primarily on the government for income in retirement, they do believe the retirement system is a critical national priority and that politicians should pay attention to retirement issues.

- Nine in ten say they’ll rely on themselves for the money needed to retire.

- Almost everyone surveyed (97%) believes Americans are not saving enough for a comfortable retirement.

- When asked to grade politicians on their efforts to help Americans save for retirement, 89 percent gave them a C or less; 29 percent actually gave them an F.

- Despite all the issues America faces, 69 percent say that Americans’ ability to save for a comfortable retirement should be a major public policy focus and the same percentage (69%) want it to be a major issue addressed in the upcoming presidential debates.

Other Notable Survey Findings

- Nearly 60 percent (59%) say their 401(k) is their only or largest source of retirement savings.

- One quarter of participants (25%) have taken a loan from their 401(k), mostly to pay for a down payment on a house, to make home improvements or to cover everyday bills.

- Almost all (91%) participants surveyed receive a company match and 87 percent of those who do contribute enough to get the full company match.

About the Survey

This online survey of U.S. 401(k) participants was conducted by Koski Research for Schwab Retirement Plan Services. The survey is based on 1,000 interviews and has a three percent margin of error at the 95 percent confidence level. Survey respondents worked for companies with at least 25 employees, were current contributors to their 401(k) plans and were 25-70 years old. Survey respondents were not asked to indicate whether they had 401(k) accounts with Schwab Retirement Plan Services. All data is self-reported by study participants and is not verified or validated. Respondents participated in the study between May 26 and June 3, 2015. Detailed findings can be found on our research page.

About Charles Schwab

At Charles Schwab we believe in the power of investing to help individuals create a better tomorrow. We have a history of challenging the status quo in our industry, innovating in ways that benefit investors and the advisors and employers who serve them, and championing our clients’ goals with passion and integrity.

More information is available at www.aboutschwab.com. Follow us on Twitter, Facebook, YouTube and LinkedIn.

Disclosures

Through its operating subsidiaries, The Charles Schwab Corporation (NYSE: SCHW) provides a full range of securities brokerage, banking, money management and financial advisory services to individual investors and independent investment advisors. Its broker-dealer subsidiary, Charles Schwab & Co., Inc. (member SIPC, www.sipc.org), and affiliates offer a complete range of investment services and products including an extensive selection of mutual funds; financial planning and investment advice; retirement plan and equity compensation plan services; compliance and trade monitoring solutions; referrals to independent fee-based investment advisors; and custodial, operational and trading support for independent, fee-based investment advisors through Schwab Advisor Services. Its banking subsidiary, Charles Schwab Bank (member FDIC and an Equal Housing Lender), provides banking and lending services and products. More information is available at www.schwab.com and www.aboutschwab.com.

Schwab Retirement Plan Services, Inc., Schwab Retirement Plan Services Company, and Charles Schwab & Co., Inc. are separate but affiliated companies and subsidiaries of The Charles Schwab Corporation. Brokerage products and services are offered by Charles Schwab & Co., Inc. (Member SIPC). Schwab Retirement Plan Services, Inc. and Schwab Retirement Plan Services Company (collectively, Schwab Retirement Plan Services) provide recordkeeping and related services with respect to retirement plans.

(0815-5314)

1 Results based on the initial 85 Schwab Index Advantage® plans as of December 31, 2014.

Schwab Index Advantage® provides a combination of index funds with low operating expenses, built-in independent professional advice available through Schwab Retirement Planner®, and Schwab Bank Savings, an interest-bearing, FDIC-insured savings feature available through Charles Schwab Bank. Schwab Retirement Planner provides participants with a fee-based retirement savings and investment strategy, a major component of which is a discretionary investment management service furnished by independent registered investment advisors GuidedChoice Asset Management, Inc.® ("GuidedChoice") or Morningstar Associates, LLC, a wholly owned subsidiary of Morningstar, Inc. GuidedChoice and Morningstar Associates are not affiliated with or agents of Schwab Retirement Plan Services, Inc.; Charles Schwab & Co., Inc., a federally registered investment advisor; or their affiliates. Schwab Index Advantage, including the Schwab Retirement Planner feature, is only available in select retirement plans serviced by Schwab Retirement Plan Services, Inc.

2 This figure represents the potential wealth increase an average 25-year-old could have at retirement when using a managed accounts service versus an average 25-year-old that did not use a managed accounts service. The analysis is based on 58,444 participants who used the Morningstar® Retirement Manager℠ service between the dates of January 2006 and February 2014. Participants are grouped by the age when they first implemented or received advice from Morningstar Retirement Manager and are assumed to have an initial retirement account value of $0 and a retirement age of 65. The results show that the average participant who first uses Morningstar Retirement Manager as a 25-year-old with a 0.4% annual fee could have 38.9% more retirement income at retirement than an average 25-year-old participant who did not use Morningstar Retirement Manager. Similarly, the average 45-year-old using Morningstar Retirement Manager with a 0.4% annual fee could have 23.3% more and the average 55-year-old could have 13.8% more retirement income at retirement. The amount of additional retirement income attributed to the use of Morningstar Retirement Manager at retirement varies by age, and tends to decrease with the age the participant first uses the Morningstar Retirement Manager service. Additionally, the potential amount of additional retirement income increases as the management fee decreases; conversely, decreases as the management fee increases. The average difference in the saving rate before and after using Morningstar Retirement Manager is calculated for each age group. The savings rate was applied to an assumed median income value for each age group. In a similar manner, the average difference in portfolio investment return before and after using Morningstar Retirement Manager was calculated for each age group. Six different annual fee levels (0.0%, 0.2%, 0.4%, 0.6%, 0.8%, and 1.0%) for the Morningstar Retirement Manager advice service were analyzed and the fee was applied to the average portfolio balance for each age group on an annual basis. The final account value for each age group at retirement age was then compared for each annual fee level. This analysis does not account for all portfolio costs such as fees, taxes, or expenses other than the annual account fee. If included, they would lower the potential amount of additional retirement income at retirement shown in this analysis. In no way should the results of this analysis be considered indicative or a guarantee of the future performance of an actual client using Morningstar Retirement Manager or considered indicative of the actual performance achieved by actual participants that have used Morningstar Retirement Manager. Actual results of participants that use Morningstar Retirement Manager may differ substantially from the results shown here and may include an individual participant incurring a loss. Morningstar Associates, LLC does not guarantee that the results of their advice, recommendations, or the objectives of Morningstar Retirement Manager will be achieved.