Newsroom

Sorted by: Latest

-

AI賦能現貨級抗體庫+自動化智造閉迴路:RenSuper Workstation協助百奧賽圖加快邁向「全球新藥發源地」

中國北京--(BUSINESS WIRE)--(美國商業資訊)-- 百奧賽圖(北京)醫藥科技股份有限公司(以下簡稱「百奧賽圖」,SSE: 688796;HKEX: 02315)近日宣布正式發表RenSuper Workstation,這一AI驅動的下一代抗體發現平台針對全球合作夥伴提供可現貨取得的大規模、經實驗驗證的全人源治療性抗體資源,支援推動抗體發現從「客製化專案」邁向「可檢索、可規模化、更高效」的新模式。 平台崛起的基石:真實全人抗體庫 + AI與自動化雙引擎 RenSuper Workstation的核心基礎,來自百奧賽圖憑藉自主RenMice®全人抗體小鼠平台長期累積的規模化免疫與真實資料體系。 圍繞1000多個潛在可成藥標靶,百奧賽圖展開大規模體內免疫與篩選,建構了海量真實全人抗體序列「現貨分子庫」。這一「真實庫」與傳統依賴預測模型生成的虛擬庫不同,其每條序列均來源於體內免疫並經過實驗驗證,具備真實結合與功能證據,為抗體研發提供更可靠的源頭分子資產。 在此基礎上,RenSuper將大規模體內免疫、下一代定序(NGS)、AI驅動的高通量篩選、實驗驗證整合為統一作業流程,並結合...

-

Computershare Trustees (Jersey) Limited UK Regulatory Announcement: Form 8.3

LONDON--(BUSINESS WIRE)-- FORM 8.3 PUBLIC OPENING POSITION DISCLOSURE/DEALING DISCLOSURE BY A PERSON WITH INTERESTS IN RELEVANT SECURITIES REPRESENTING 1% OR MORE Rule 8.3 of the Takeover Code (the “Code”) 1. KEY INFORMATION (a) Full name of discloser: Computershare Trustees (Jersey) Limited as trustee of the Schroders Employee Benefit Trust (b) Owner or controller of interests and short positions disclosed, if different from 1(a): The naming of nominee or vehicle companies is insufficient. Fo...

-

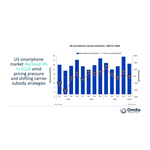

Omdia: US Smartphone Market Declined 3% in 1Q26 Amid Pricing Pressure and Carrier Subsidy Shifts

LONDON--(BUSINESS WIRE)--The US smartphone market declined 3% year over year to 33.4 million units in 1Q26, according to Omdia’s latest research. The comparison was against an elevated 1Q25 base when vendors and carriers accelerated inventory build-up ahead of potential US tariff actions. Beyond this comparison effect, US smartphone shipments were pressured by a more restrained carrier upgrade environment, rising memory and storage costs, and delayed device launches that compressed sell-through...

-

Natixis Syndicate UK Regulatory Announcement: Pre-stabilisation Period Announcement

LONDON--(BUSINESS WIRE)-- PRE-STABILISATION ANNOUNCEMENT Date: 27th May 2026 Not for distribution, directly or indirectly, in or into the United States or any jurisdiction in which such distribution would be unlawful. Carrefour S.A Pre-stabilisation Period Announcement Natixis (contact: Christopher Agathangelou; telephone: 0158550814) hereby gives notice, as Stabilisation Coordinator, that the Stabilisation Manager(s) named below may stabilise the offer of the following securities in accordanc...

-

euNetworks launches new quantum-safe private connectivity service powered by Adtran’s encrypted optical transport technology

LONDON--(BUSINESS WIRE)--Adtran and euNetworks today announced their collaboration on the launch of a new quantum-safe private connectivity service, Quantum Shield. euNetworks has developed Quantum Shield using Adtran’s optical transport technology to augment its broader architecture, which is designed to deliver secure, scalable data center connectivity across euNetworks’ pan-European network. The new offering is built for enterprises with stringent security, performance and customer-controlle...

-

National Bank of Greece in Cyprus Goes Live With Smartstream’s Air to Consolidate Reconciliations

LONDON--(BUSINESS WIRE)--Smartstream, the trusted data solutions provider for leading global financial institutions and enterprises, today announces that the National Bank of Greece (NBG) in Cyprus has successfully gone live with Air, the company’s AI-enabled reconciliation solution. The go-live marks a significant step forward in the bank’s operational efficiency, reducing daily manual processing effort and eliminating the complexity of working across multiple data formats. The bank has deploy...

-

First Trust Global Funds PLC UK Regulatory Announcement: Net Asset Value(s)

LONDON--(BUSINESS WIRE)-- Funds Date TIDM ISIN Code Shares in Issue Currency Net Asset Value NAV/per Share First Trust Eurozone AlphaDEX UCITS ETF 26.05.2026 FEUZ IE00B8X9NY41 1,838,344.00 EUR 119,392,657.48 64.946 ...

-

First Trust Global Funds PLC UK Regulatory Announcement: Net Asset Value(s)

LONDON--(BUSINESS WIRE)-- Funds Date TIDM ISIN Code Shares in Issue Currency Net Asset Value NAV/per Share First Trust Emerging Markets AlphaDEX UCITS ETF 26.05.2026 FEM IE00B8X9NX34 325,002.00 USD 16,562,275.18 50.961 ...

-

D&D Pharmatech Announces Positive 48-Week Histology Results for Zabopegdutide (DD01), Demonstrating Statistically Significant Fibrosis Improvement and MASH Resolution

GYEONGGI-DO, South Korea & GAITHERSBURG, Md.--(BUSINESS WIRE)--D&D Pharmatech, Inc. (D&D) (KOSDAQ: 347850), a clinical-stage biotechnology company developing breakthrough treatments for liver and metabolic diseases, today announced positive top-line 48-week histology results from its Phase 2 trial (DD01-DN-02) evaluating zabopegdutide (DD01) in patients with Metabolic Dysfunction-Associated Steatohepatitis (MASH). Following the rapid and robust liver fat reduction observed at the Week 1...

-

First Trust Global Funds PLC UK Regulatory Announcement: Net Asset Value(s)

LONDON--(BUSINESS WIRE)-- Funds Date TIDM ISIN Code Shares in Issue Currency Net Asset Value NAV/per Share First Trust US Large Cap Core AlphaDEX UCITS ETF 26.05.2026 FEXD.LN IE00BWTNMB87 457,230.00 USD 45,318,827.51 99.116 ...