NEW YORK & LONDON & HONG KONG--(BUSINESS WIRE)--Seven in 10 consumers around the world would welcome robo-advisory services – computer-generated advice and services that are independent of a human advisor – for their banking, insurance and retirement planning, according to a new report by Accenture (NYSE:ACN). Yet, a large number of consumers still want human interaction for their more complex needs, leaving firms challenged with blending a physical presence with an advanced digital user-experience, as they look to integrate robot and human services.

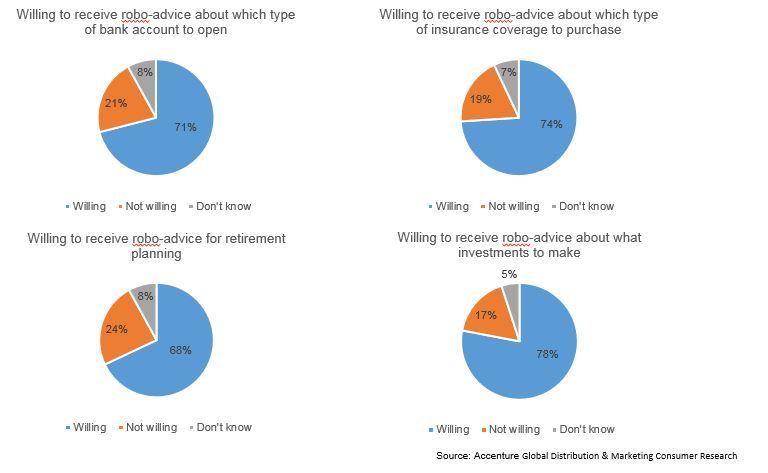

The global Distribution & Marketing Consumer research by Accenture, which includes a survey of nearly 33,000 consumers in 18 countries and regions, found that the vast majority are willing to receive exclusively robo-generated advice for certain banking and insurance products. Consumers are now open to robo-advice to help determine which bank account to open (71 percent), which insurance coverage to purchase (74 percent), and how to plan for retirement (68 percent). Nearly four out of five (78 percent) consumers said they would welcome robo-advice for traditional investing, where the technology first emerged.

Consumers also Expect First-Class Human Interaction

However, the study also found that nearly two-thirds of consumers still want human interaction in financial services, especially to deal with complaints (68 percent) and advice about complex products such as mortgages (61 percent).

Piercarlo Gera, senior managing director, Accenture Financial Services, said: "We found strong consumer demand exists today for robo-advice in all areas of financial services - banking, insurance and financial advice. While financial institutions may expect to benefit from internal cost reduction by providing customers with a ‘robo’ option, our research found that consumers also expect first-class human interaction. Successful financial services firms will therefore need a "phygital" strategy that seamlessly integrates technology, branch networks and staff to provide a service that combines physical and digital capabilities and gives consumers a choice."

Consumers indicated the main attractions for using robo-advice platforms is the prospect of faster (39 percent) and less expensive (31 percent) services, and because they think computers/artificial intelligence are more impartial and analytical than humans (26 percent).

The research found that the countries with the biggest appetite for robo-advice are in the emerging economies of Indonesia (92 percent), Thailand (90 percent), Brazil (86 percent) and Chile (84 percent) – all markets where it is already common to use a smartphone or other digital device as the primary vehicle for financial services interactions. Even in the countries with the lowest demand – Canada (56 percent), Germany (59 percent) and Australia (61 percent) – more than half of consumers surveyed said they are willing to use robo-advice.

Non-traditional Providers Hold Strong Appeal

The survey also found that consumers are willing to switch to non-traditional providers for financial services. Nearly one-third would switch to Google, Amazon or Facebook for banking services (31 percent), insurance services (29 percent) and financial advisory services (38 percent). For consumers aged 18 to 21 years old, the number willing to switch banking services to one of these companies only rises to 41 percent, indicating that many younger consumers see value in traditional financial institutions. Tech giants are not the only ones putting pressure on financial service firms; nearly the same percentage of global consumers would also consider switching to a supermarket or retailer for their banking (31 percent) and insurance (30 percent) services.

Alan McIntyre, senior managing director, head of Accenture Banking, said: “Consumers expect nearly all of their transactions to be on par with the service they receive from GAFA (Google, Amazon, Facebook and Apple) companies, which poses a challenge for banks in particular. Banks need to create branches that provide an advanced digital experience combined with convenient locations, while also developing an online digital experience that can compete head on with the tech giants. The vast majority of today’s consumers view their bank relationships as entirely transactional; in order to gain customer loyalty, banks have to be more assertive in using technology to provide tailored, personalized offerings when, where and how customers want them.”

Personalization

The survey found nearly two-thirds of consumers are interested in personalized insurance (64 percent) and banking (63 percent) advice based on their individual circumstances, and when asked about wealth management advice, that increases to 73 percent. Nearly half of consumers (48 percent) want banks to play a supporting role in the purchasing process for non-banking products, such as a house or new car or services related to those purchases (i.e. insurance products, assistance with the sale and/or closing process). Consumers indicated that banks could assist with these important decisions by sending helpful information based on consumer location data, price range and other personal preferences.

Data as Currency

The survey also found that consumers are willing to share their data with financial services providers in exchange for benefits like less expensive and faster services. Globally, 67 percent would grant their bank access to more personal data, but 63 percent want more tailored advice and demand a priority service – such as expedited loan approvals – or a monetary benefit, such as more competitive pricing, in return for the information they share. More than half (57 percent) of consumers would grant their insurance provider access to personal data, but 64 percent want more tailored advice in exchange.

Three consumer personas

Accenture identified three distinct consumer personas from the research with specific characteristics around what they value most from their financial service providers, how they want to access services in the future, and how they would like to embrace digital innovation.

Nomads: Highly digitally active group, ready for a new model of delivery, represents 39 percent of consumers surveyed, but significantly more in less developed economies, such as Brazil where Nomads were more than 60 percent

Hunters: Searching for the best deal on price, represents 17 percent of consumers surveyed and tend to skew a little older

Quality Seekers: Looking for high quality, responsive service and data protection, represents 44 percent of consumers

The full report can be downloaded at www.accenture.com/FSConsumerStudy.

Methodology

Accenture surveyed 32,715 respondents across 18 countries and regions including the US, Canada, Benelux, France, Germany, Ireland, Italy, Nordic countries, Spain, the United Kingdom, Brazil, Chile Australia, Hong Kong, Indonesia, Japan, Singapore and Thailand. Respondents were consumers of banking, insurance and wealth management services; they were required to have a bank account and an insurance policy and were asked if they used an Independent Financial Advisor, Wealth Manager or Asset Manager, with total financial advisory responses totaling 9,987. Respondents covered multiple generations and income levels. The survey was conducted during May and June 2016.

About Accenture

Accenture is a leading global professional services company, providing a broad range of services and solutions in strategy, consulting, digital, technology and operations. Combining unmatched experience and specialized skills across more than 40 industries and all business functions – underpinned by the world’s largest delivery network – Accenture works at the intersection of business and technology to help clients improve their performance and create sustainable value for their stakeholders. With more than 394,000 people serving clients in more than 120 countries, Accenture drives innovation to improve the way the world works and lives. Visit us at www.accenture.com.