")

and Connecticut Southern Railroad (CSO)(Photo: Business Wire)")

DARIEN, Conn.--(BUSINESS WIRE)--Genesee & Wyoming Inc. (G&W) (NYSE:GWR) announced today that it has agreed to acquire Providence and Worcester Railroad Company (P&W)(NASDAQ: PWX) for $25.00 per share, or approximately $126 million. Subject to satisfaction of customary closing conditions, the acquisition is expected to close following the receipt of P&W shareholder approval in the fourth quarter of 2016.

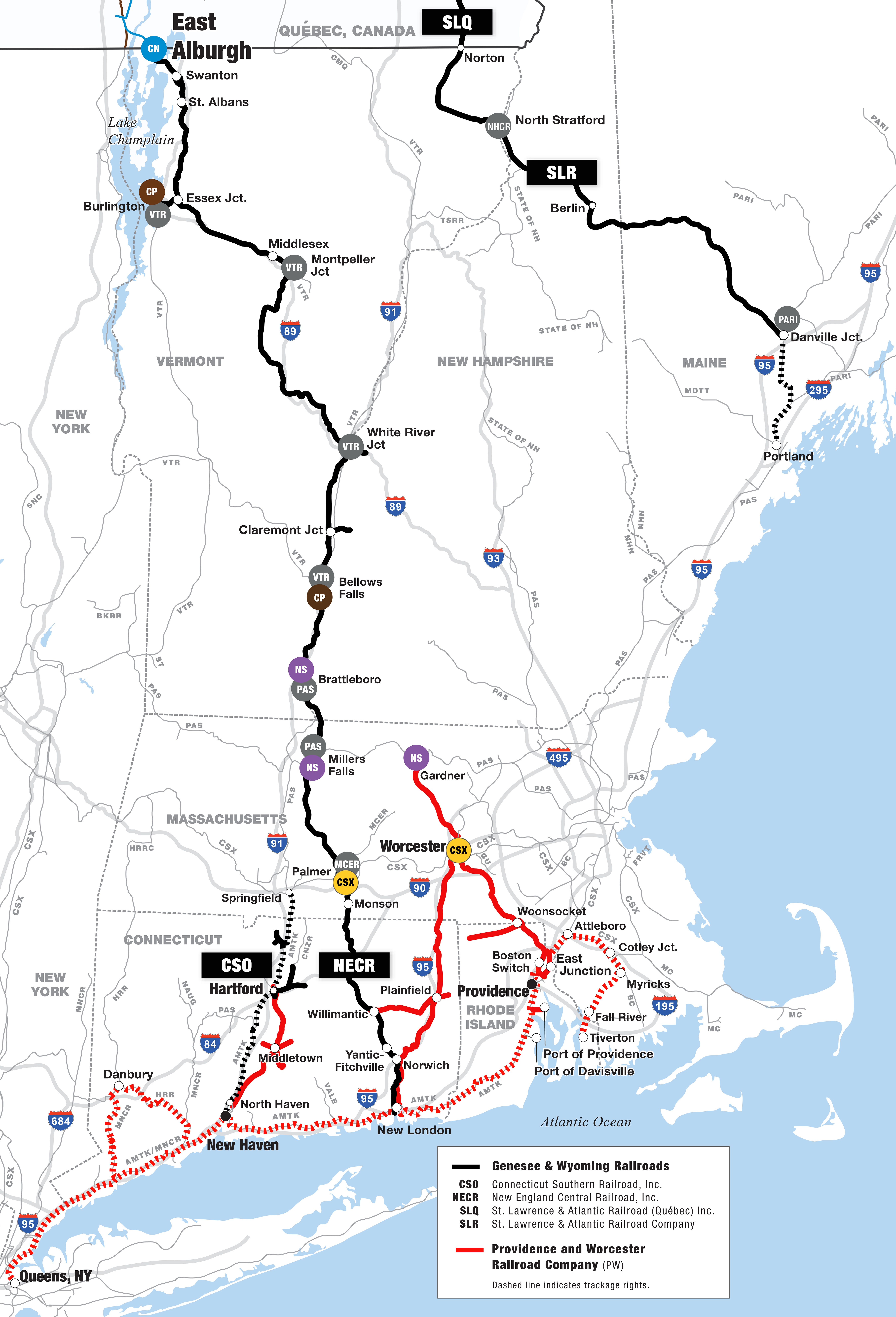

Headquartered in Worcester, Mass., and operating in Rhode Island, Massachusetts, Connecticut and New York, P&W is contiguous with G&W’s New England Central Railroad (NECR) and Connecticut Southern Railroad (CSO). Rail service is provided by approximately 140 P&W employees with 32 locomotives across 163 miles of owned track and over approximately 350 miles under track access agreements, including exclusive freight access over Amtrak’s Northeast Corridor between New Haven, Conn., and Providence, R.I., and trackage rights over Metro-North Commuter Railroad, Amtrak and CSX Corp. (NASDAQ: CSX) between New Haven, Conn., and Queens, N.Y. P&W interchanges with G&W’s NECR and CSO railroads, as well as with CSX, Norfolk Southern (NYSE: NSC), Pan Am Railways, Pan Am Southern, the Housatonic Railroad and the New York and Atlantic Railroad, and also connects to Canadian National (NYSE: CNI) and Canadian Pacific (NYSE: CP) via NECR.

P&W serves a diverse mix of aggregates, auto, chemicals, metals and lumber customers in southeastern New England, handling approximately 43,000 carloads and intermodal units annually. In addition, P&W provides rail service to three ports (Providence, Davisville and New Haven) and to a U.S. Customs bonded intermodal terminal in Worcester, Mass., that receives inbound intermodal containers for distribution in New England. P&W also owns approximately 45 acres of undeveloped waterfront land in East Providence, R.I., that was initially created as a deep water, rail served port through a $12 million investment. G&W expects to sell this undeveloped land.

Upon approval by the Surface Transportation Board (STB), P&W would be managed as part of G&W’s Northeast Region, led by Senior Vice President Dave Ebbrecht. The addition of P&W to G&W’s existing presence in the region substantially enhances G&W’s ability to serve customers and Class I partners in New England, which is a highly competitive rail market with a premium placed on timely, efficient and safe rail service. The acquisition is anticipated to unlock significant cost savings through overhead, operational and long-term network efficiencies as well as to generate significant new commercial opportunities.

Jack Hellmann, President and Chief Executive Officer of G&W, commented: “The acquisition of P&W is an excellent strategic fit with G&W’s contiguous railroads, the New England Central and the Connecticut Southern. Following anticipated STB approval of the acquisition, our connectivity with the P&W enables us to realize substantial immediate cost savings, to share and optimize the utilization of equipment and other assets, and to unlock significant new customer opportunities across sister G&W railroads as well as connecting partners at two Canadian Class I Railroads, two U.S. Class I Railroads and two regional railroads. Our acquisition of the P&W will ultimately enhance the efficiency and customer service of rail in New England.”

“We are excited to welcome P&W’s employees to G&W as we work together to provide safe, reliable and efficient rail service to our customers for the long term. We also look forward to working with our Class I partners, Amtrak and Metro-North Commuter Railroad to ensure a smooth transition of services and build upon the success of P&W’s current operations.“

Financial Impact and Financing

In the first year of operation, G&W anticipates P&W will generate approximately $35 million of revenue and $12 million of EBITDA, including realization of $8 million of immediate overhead and operational cost savings. In the medium term, G&W anticipates additional operational efficiencies and commercial opportunities will generate a further $5 million of EBITDA that will be realized over the following two to three years.

G&W expects P&W will require approximately $3 million of annual capital expenditures and have depreciation and amortization expense of approximately $3 million. G&W expects annual diluted EPS accretion from the acquisition of approximately 2%, subject to finalization of acquisition accounting under U.S. GAAP.

G&W expects to fund the approximately $126 million acquisition through its revolving credit facility under which it had available capacity of $542 million as of June 30, 2016. As previously noted, G&W expects to sell the land in East Providence, R.I., which was developed through a $12 million investment.

Closing Conditions

The closing of the transaction is subject to the approval of the Surface Transportation Board (STB). G&W will seek confirmation from the staff of the STB that, if the STB has not yet approved the transaction, G&W may close the transaction into a proposed form of voting trust, which will be managed by an independent voting trustee until G&W is granted approval from the STB to control P&W.

The closing of the transaction is also subject to satisfaction of customary closing conditions, including without limitation the approval by the holders of at least a majority of the outstanding shares of P&W’s common stock and preferred stock entitled to vote.

This press release contains “forward-looking statements” relating to the proposed acquisition of Providence and Worcester Railroad Company by Genesee & Wyoming. Such forward-looking statements are based on current expectations and involve inherent risks and uncertainties, including factors that could change or delay any of them, and could cause actual outcomes and results to differ materially from current expectations. No forward-looking statement can be guaranteed. Among other risks, there can be no guarantee that the acquisition will be completed within the anticipated time frame or at all or that the expected benefits of the acquisition will be realized. Factors that could cause actual results to differ materially include, but are not limited to: (1) the occurrence of any event, change or other circumstances that could give rise to the termination of the merger agreement; (2) the outcome of any legal proceedings that may be instituted against P&W or G&W and others following announcement of the merger agreement; (3) the inability to complete the merger due to the failure to satisfy the conditions to the merger; (4) risks that the proposed transaction disrupts current plans and operations and potential difficulties in employee retention as a result of the merger; (5) the ability to recognize the benefits of the merger; (6) legislative, regulatory and economic developments; and (7) other factors described in G&W’s filings with the SEC. Many of the factors that will determine the outcome of the subject matter of this communication are beyond G&W’s ability to control or predict. Forward-looking statements in this press release should be evaluated together with the many uncertainties that affect G&W’s business, particularly those identified in the cautionary factors discussed in G&W’s annual report on Form 10-K for the year ended December 31, 2015. Any statements relating to the future performance of the combined company are made solely by G&W. G&W does not undertake, and expressly disclaims, any duty to publicly update any forward-looking statement, whether as a result of new information, future events, or otherwise, except as required by law.

Non-GAAP Financial Measures

This press release contains references to earnings before interest, income taxes, depreciation and amortization (EBITDA) which is a “non-GAAP financial measure” as this term is defined in Item 10(e) of Regulation S-K under the Securities Act of 1933 and the Securities Exchange Act of 1934 and Regulation G under the Securities Exchange Act of 1934. In accordance with these rules, G&W has reconciled this non-GAAP financial measure to the most directly comparable U.S. GAAP measure.

Management views this non-GAAP financial measure as an important measure of G&W’s operating performance. Management also views this non-GAAP financial measure as a way to assess comparability between periods.

Non-GAAP financial measures are not intended to represent, and should not be considered more meaningful than, or as an alternative to, their most directly comparable GAAP measures. This non-GAAP financial measure may be different from similarly-titled non-GAAP financial measures used by other companies.

The following tables set forth reconciliations of each non-GAAP financial measure to its most directly comparable GAAP measure (in millions).

|

Three Months Ended |

|||||||||||||||||||||||||||||||||||

| $ in millions |

Sept. 30, |

Dec. 31, |

Mar. 31, |

June 30, |

Last |

Adjustments |

Pro |

||||||||||||||||||||||||||||

| Net Income / (Loss) | $0.5 | $1.4 | ($1.0) | $0.2 | $1.1 | - | $1.1 | ||||||||||||||||||||||||||||

| Add Back | |||||||||||||||||||||||||||||||||||

| Provision for Income Taxes | 0.3 | 0.6 | (0.5) | 0.1 | 0.4 | - | 0.4 | ||||||||||||||||||||||||||||

| Interest Expense | - | 0.0 | 0.0 | 0.0 | 0.0 | - | 0.0 | ||||||||||||||||||||||||||||

| Other (Income) / Loss | (0.0) | 0.1 | (0.0) | (0.0) | (0.0) | - | (0.0) | ||||||||||||||||||||||||||||

| Depreciation & Amortization | 0.8 | 1.0 | 0.7 | 0.8 | 3.3 | - | 3.3 | ||||||||||||||||||||||||||||

| Pro Forma Adjustments | |||||||||||||||||||||||||||||||||||

| Short Line Tax Credit | - | - | - | - | - | (1.8) | (1.8) | ||||||||||||||||||||||||||||

| Expected Immediate Cost Savings | - | - | - | - | - | 8.0 | 8.0 | ||||||||||||||||||||||||||||

| Expected Business Growth (1) | - | - | - | - | - | 1.1 | 1.1 | ||||||||||||||||||||||||||||

| EBITDA | $1.4 | $3.1 | ($0.8) | $1.0 | $4.7 | $7.3 | $12.0 | ||||||||||||||||||||||||||||

| (1) | Full year run rate of recent new business initiatives, contractual rate increases and other rate and volume growth expectations | |||||||

About G&W

Genesee & Wyoming owns or leases 121 freight railroads worldwide that are organized in 10 operating regions with approximately 7,200 employees and more than 2,800 customers.

- G&W’s eight North American regions serve 41 U.S. states and four Canadian provinces and include 114 short line and regional freight railroads with more than 13,000 track-miles.

- G&W’s Australia Region provides rail freight services in New South Wales, the Northern Territory and South Australia and operates the 1,400-mile Tarcoola-to-Darwin rail line.

- G&W’s U.K./Europe Region is led by Freightliner, the U.K.’s largest rail maritime intermodal operator and second-largest rail freight company. Operations also include heavy-haul in Poland and Germany and cross-border intermodal services connecting Northern European seaports with key industrial regions throughout the continent.

G&W subsidiaries provide rail service at more than 40 major ports in North America, Australia and Europe and perform contract coal loading and railcar switching for industrial customers.

For more information, visit gwrr.com.