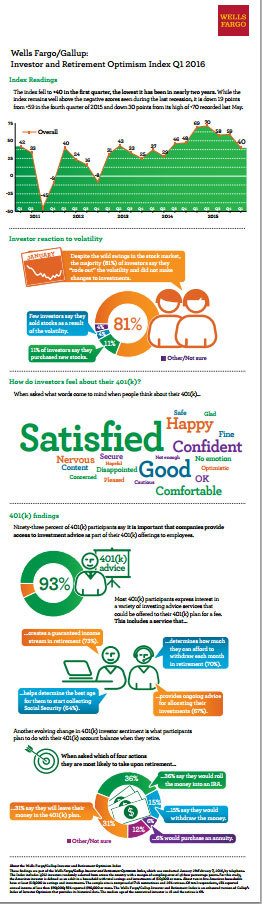

CHARLOTTE, N.C.--(BUSINESS WIRE)--The Wells Fargo/Gallup Investor and Retirement Optimism Index fell to +40 in the first quarter, the lowest it has been in nearly two years. While the index remains well above the negative scores seen during the last recession, it is down 19 points from +59 in the fourth quarter of 2015 and down 30 points from +70 last May.

The primary factor responsible for the decline is reduced optimism in the stock market. The percentage of investors optimistic about the 12-month outlook for the stock market fell from 45% last quarter to 32%. The overall index dropped more among non-retirees than among retirees; however, non-retirees remain slightly more optimistic at +41 vs. +35 for retirees. The percentage of investors feeling confident in the stock market as a place to save and invest for retirement also fell — from 43% to 36%.

These results are from the first-quarter Wells Fargo/Gallup Investor and Retirement Optimism Index survey conducted January 29-February 7 with 1,012 U.S. investors.

“This is yet another quarter that investors have had to weather significant market volatility. While it has weakened their confidence in the investment climate, it is still a minor adjustment relative to what we saw during the recession,” said Joe Ready, director of Wells Fargo Institutional Retirement and Trust. “However, a prolonged period of market volatility may ignite fears of a recession and further erode investor confidence down the road.”

Four in 10 Investors Consider Volatility the “New Normal”

When investors were asked if frequent stock market volatility will become “the new, normal pattern in the years ahead” or if it represents “a temporary pattern,” 40% of investors opted to call it the “new normal” while 54% said it was “temporary.”

Despite the wild swings in the stock market, the majority (81%) of investors say they “rode out” the volatility and did not make changes to investments. Few investors — just 4% — say they sold stocks as a result of the volatility in January, and 11% say they purchased new stocks. Even though a majority made no changes to their investments, 59% say they could use financial advice to deal with volatility in their 401(k).

Volatility is having a negative impact on many investors, with 39% agreeing with the statement that market volatility is making their life stressful. This breaks down to 46% of retired investors and 36% of non-retired investors. Another source of stress for investors is the fact that the Great Recession still has an impact, with a majority (70%) of respondents saying they know someone whose financial situation hasn’t recovered since the economic downturn, while 37% say their own financial situation has not recovered.

“The Great Recession is a period in history that so many Americans are still very familiar with, even seven years past the lows. With that so fresh, it makes sense that the volatility would create significant stress for people, particularly retirees,” Ready said.

Low Energy Prices Good for Consumers, Not So Good for the Markets

When asked about the impact low gas prices are having on the country, 71% of investors believe today’s low gas prices are good for the economy; just 25% say they are bad for the economy. However, investors are split in evaluating the impact on the financial markets: 49% say low gas prices are good for the markets; 46% say they are bad.

With oil prices reaching new lows, a third of investors (32%) say the decline in oil and gas prices is helping their household budget a lot — up from 27% a year ago — and another 36% say it is helping a little. Just 31% say it has not made much difference to them.

Similar to a year ago, 37% of investors say they are using the savings to pay down bills, 31% are putting more money into savings and 27% are using the money for additional purchases.

Confidence in Retirement Savings Drops

Dovetailing with retired investors who say market volatility is making their life stressful (46%), the poll shows that the percentage of retired investors who feel very confident they have enough savings to last throughout their retirement declined over the past year — from 47% to 39%.

Meanwhile, non-retired investors also have less confidence in their retirement savings. The percentage who say they are very confident they will have enough savings for retirement at the time they choose to retire slipped from 28% to 23%. However, these investors still have more time to wait for the market to recover, as well as the opportunity to increase their savings before reaching their retirement years.

“With increased longevity, retired investors are highly vulnerable to major market swings and the sequence of investment returns in their portfolio, making it particularly important for them to periodically evaluate their portfolio in terms of risk appetite, as well as their time horizon for retirement,” said Ready.

Do People Know to Save Their Way to Retirement?

Investors are evenly divided when asked which of two factors is more important to their success in preparing for a successful retirement: the amount of money they save during their working years (44%) or how they allocate and invest their money (43%).

“Markets will go through unpredictable cycles so it’s important for investors to focus on what they can control, which is their savings rate. Saving money is the main driver of a successful retirement. Thoughtful investing adds to the process, but saving is the key,” said Ready.

The good news is that the largest segment of investors (44%) strongly view themselves as someone who consistently saved since they started working. A quarter (25%) somewhat agree, while 30% disagree. Interestingly, the poll finds that not all investors consider themselves “investors.” Just 30% strongly agree that they think of themselves as “an investor.” Another 32% somewhat agree, while 38% disagree.

“Whether you have money in the stock market or in a 401(k), you are an investor. When people perceive themselves as an investor, they’ll have a mindset that they are in control of their own retirement through saving, and then investing,” said Ready.

401(k) Sentiment Overwhelmingly Positive

The majority of non-retired investors who have a 401(k) (91%) say they are satisfied with it as a retirement tool. This includes 44% very satisfied and 47% somewhat satisfied. Only 9% are dissatisfied. When asked what words come to mind when people think about their 401(k), the top three responses are “satisfied,” “good,” and “happy.”

Additionally, among all investors, 59% think all businesses, regardless of size, should be required to offer their employees a 401(k) plan. Also, 40% think all workers should be required to deposit at least 3% of their income into a 401(k)-type retirement plan; 59% oppose this. A majority — 82% — oppose increasing fees and penalties for early withdrawals whereas 17% favor such penalties.

Further, 401(k) participants are eager to get the most out of their plans. Ninety-three percent of 401(k) participants say it is important that companies provide access to investment advice as part of their 401(k) offerings to employees. Two thirds (66%) say this is very important, and another 27% consider it somewhat important.

Most 401(k) participants also express interest in a variety of investing advice services that could be offered to their 401(k) plan for a fee. This includes a service that creates a guaranteed income stream in retirement (73%); a service that determines how much they can afford to withdraw each month in retirement (70%); ongoing advice for allocating their investments (67%); and help determining the best age for them to start collecting Social Security (64%).

Another evolving change in 401(k) investor sentiment is what participants plan to do with their 401(k) account balance when they retire. When asked which of four actions they are most likely to take upon retirement, 31% say they will leave their money in the 401(k) plan while slightly more — 36% — say they would roll the money into an IRA. Nearly one in seven (15%) say they would withdraw the money, while 6% would purchase an annuity.

According to Ready, “These findings represent a vote of confidence in the 401(k) system. Investors really value their workplace 401(k) and believe others should have access to a 401(k). In addition, they are starting to view it as a good place to invest during their retirement years.”

Investors Want to Delay Retirement

Not all non-retired investors are counting down the days until they can retire. Two-thirds of non-retired investors (67%) agree they want to work as long as possible because it’s better for their physical and mental health, and half (51%) want to delay retirement as long as possible to give them more time to save.

By contrast, 53% of retired investors agree they want to work part time in their retirement years because they think it will benefit them mentally and physically.

For more information and investment strategies to consider, read “Living Longer, Living Better” from Wells Fargo Investment Institute.

About the Wells Fargo/Gallup Investor and Retirement Optimism Index

These findings are part of the Wells Fargo/Gallup Investor and Retirement Optimism Index, which was conducted January 29-February 7, 2016, by telephone. The Index includes 1,012 investors randomly selected from across the country with a margin of sampling error of +/- four percentage points. For this study, the American investor is defined as an adult in a household with total savings and investments of $10,000 or more. About two in five American households have at least $10,000 in savings and investments. The sample size is comprised of 74% non-retirees and 26% retirees. Of total respondents, 45% reported annual income of less than $90,000; 55% reported $90,000 or more. The Wells Fargo/Gallup Investor and Retirement Index is an enhanced version of Gallup’s Index of Investor Optimism that provides its historical data. The median age of the non-retired investor is 45 and the retiree is 69.

The Index had a baseline score of 124 when it was established in October 1996. It peaked at 178 in January 2000, at the height of the dot-com boom, and hit a low of negative 64 in February 2009.

About Wells Fargo & Company (Twitter @WellsFargo)

Wells Fargo & Company (NYSE:WFC) is a diversified, community-based financial services company with $1.8 trillion in assets. Founded in 1852 and headquartered in San Francisco, Wells Fargo provides banking, insurance, investments, mortgage, and consumer and commercial finance through 8,700 locations, 13,000 ATMs, the internet (wellsfargo.com) and mobile banking, and has offices in 36 countries to support customers who conduct business in the global economy. With approximately 265,000 team members, Wells Fargo serves one in three households in the United States. Wells Fargo & Company was ranked No. 30 on Fortune’s 2015 rankings of America’s largest corporations. Wells Fargo’s vision is to satisfy our customers’ financial needs and help them succeed financially. Wells Fargo perspectives are also available at Wells Fargo Blogs and Wells Fargo Stories.

About Gallup

Gallup delivers analytics and advice to help leaders and organizations solve their most pressing problems. Combining more than 80 years of experience with its global reach, Gallup knows more about the attitudes and behaviors of employees, customers, students and citizens than any other organization in the world.