Newsroom

Sorted by: Latest

-

Pas de licenciements, salaires versés à temps : Rizwan Sajan, président du Groupe Danube, rassure ses plus de 6 000 employés malgré l’incertitude géopolitique

Dubaï, Émirats arabes unis--(BUSINESS WIRE)--Alors que le conflit israélo-iranien redessine le paysage géopolitique et économique, les entreprises de la région sont mises à l’épreuve quant à leur capacité d’adaptation et de résilience. Dans ce contexte, Rizwan Sajan, fondateur et président du Groupe Danube, fait preuve d’un leadership exemplaire en réaffirmant son soutien indéfectible à ses employés. Mardi, M. Sajan a annoncé sur Instagram que l’entreprise ne procéderait à aucun licenciement. «...

-

MedTech Innovator Radar Forum April 7-9 Levels Up MedTech Industry’s Most Rigorous Evaluation Platform and Leading Accelerator Program

LOS ANGELES--(BUSINESS WIRE)--MTI evolves Road Tour with invite-only Radar Forum, uniting experts to evaluate top medtech startups and select 65 for accelerator....

-

No Layoffs, Salaries On Time: Danube Group Chairman Rizwan Sajan Assures Its 6000+ Workforce Despite Geopolitical Uncertainty

DUBAI, United Arab Emirates--(BUSINESS WIRE)--No Layoffs, Salaries On Time: Danube Group Chairman Rizwan Sajan Assures Its 6000+ Workforce Despite Geopolitical Uncertainty...

-

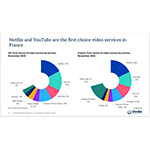

オムディア(Omdia)、Netflixが10億を突破する一方、YouTubeは2027年までに世界ユーザー30億人に近づく見込みと発表。

ロンドン--(BUSINESS WIRE)--(ビジネスワイヤ) -- オムディア(Omdia)の発表に によると、Netflixは2027年までに世界の月間アクティブユーザーが10億人を超える見込みであり、YouTubeは世界で30億人に迫ると予測されている。 本データは、Omdiaのメディア&エンターテインメント部門責任者であるMaria Rua Aguete氏がSeries Maniaで発表したもので、グローバルプラットフォームが欧州全域の動画消費をいかに再構築しているかを示している。 YouTubeフランスおよび南欧担当マネージングディレクターのJustine Ryst氏とのセッションで、Aguete氏は、フランスにおいてNetflixとYouTubeが従来の放送局や有料テレビを抑え、動画サービスの「第1選択」としてトップを走っていることを強調した。Netflixが18%で市場をリードし、続いてYouTubeが12%となっている このセッション「「YouTube」を自社のシリーズ番組の資産として変えるには?」では、コンテンツ・エコシステムにおけるYouTubeの進化する役割が...

-

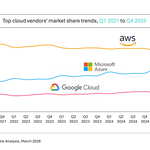

オムディア(Omdia)、ハイパースケーラーがAIインフラ投資を拡大する中、2025年Q4の世界クラウドインフラ支出は29%増と発表

ロンドン--(BUSINESS WIRE)--(ビジネスワイヤ) -- オムディアによると、2025年Q4の世界のクラウドインフラサービス支出は1,109億米ドルに達し、前年同期比で29%増加した。成長は前四半期から加速し、市場が20%以上の拡大を記録するのは6四半期連続となった。企業のAI需要が実験段階から本番導入へと移行する中、ハイパースケーラーはAIインフラ容量の拡大に向けた投資を増やしている。 2026年の見通しとして、オムディアは世界のクラウドインフラサービス支出が27%成長すると予測。差別化の鍵は、インフラの規模、資本効率、およびAIエージェント関連プラットフォーム機能の強さによってますます左右されるとしている。 ■ 主要クラウドベンダーの市場シェア動向(2021年Q1〜2025年Q4) 同四半期には、AWSの成長率は24%へと加速する一方、Microsoft AzureとGoogle Cloudはそれぞれ前年比39%と50%という力強い成長を記録した。AI需要はもはやGPUといった特化型コンピューティングに限定されず、CPU、ストレージ、ネットワーキングを含むより広範な...

-

Ducon Announces Advanced Solutions to Mitigate Air Pollution from Missile Interceptions

NEW YORK--(BUSINESS WIRE)--Ducon Technologies (“Ducon”), a global leader in high-efficiency air pollution control and infrastructure related technologies, today announced solutions for the escalating environmental and public health crisis caused by high-altitude missile interceptions in the ongoing conflict in Iran. When an air defense system successfully intercepts a missile, the immediate reaction is one of relief. A fireball in the sky represents a catastrophe averted on the ground. However,...

-

RYAM Statement on Localized Fire at Jesup Facility

JACKSONVILLE, Fla.--(BUSINESS WIRE)--Rayonier Advanced Materials Inc. (NYSE: RYAM) confirmed that an isolated fire occurred at approximately 10:00 p.m. on April 4 in the digester area of its Jesup, Georgia facility during its scheduled annual maintenance outage. The fire was quickly contained and extinguished by the Company’s on-site team with assistance from local first responders. There were no injuries and no off-site impacts. The Company has initiated standard follow-up actions, including a...

-

Faraday Future Founder and Co-CEO YT Jia Shares Weekly Investor Update: FF to Establish the First Scaled EAI Education System in the United States With Deployment of Its EAI Robotics Products and Technology

LOS ANGELES--(BUSINESS WIRE)--Faraday Future Intelligent Electric Inc. (NASDAQ: FFAI) (“Faraday Future”, “FF” or the “Company”), a California-based global Embodied AI (EAI) ecosystem company, today shared a weekly business update from YT Jia, Founder and Global Co-CEO of FF. This week’s update will be in the form of a Q&A session with YT. “Q1: YT, you mentioned that, in your opinion, the most important highlight of this annual financial report is that the Company’s net equity turned from ne...

-

Huawei、LG Electronics、および Nokia がシズベルの新しい POS プールの創設ライセンサーに

ルクセンブルク--(BUSINESS WIRE)--(ビジネスワイヤ) -- シズベルは本日、2G から 5G 技術を対象とする新たな POS(販売時点情報管理)特許プールを発表し、その創設ライセンサーとして、世界クラスのイノベータ 3 社が参画していることを明らかにしました。 これら 3 社、Huawei、LG Electronics、Nokia は、セルラー通信対応の POS デバイスに関する標準必須特許(SEP)を、本プログラムを通じて利用できるよう提供し、ユビキタス化がますます進む技術へのアクセスを簡素化します。 本特許プールでは、ライセンサーの早期参加を促進するインセンティブを 5 月中旬までご提供しています。現在シズベルと協議中でない他のセルラー特許権者の皆様も、ぜひ参加をご検討のうえ、当社にお問い合わせください。 ハンドヘルド型カード決済端末からタブレット型レジスターまで、POS デバイスは顧客の支払い処理を大きく変革してきました。さらに近年では、在庫管理、リアルタイム追跡、詳細分析、自動再発注などの高度な機能も備えるようになっています。 標準化されたセルラー技術は、顧...

-

„Sensofusion“ pristato „Sensofusion Aviation“ – kovos su bepiločiais orlaiviais sistemas, skirtas naudoti ore

HELSINKIS--(BUSINESS WIRE)--Sparčiai auganti Suomijos gynybos technologijų įmonė „Sensofusion“ įsigijo Suomijos orlaivių gamintoją „Atol Aviation“. Įsigijusi šią gamintoją „Sensofusion“ grupė įgyja orlaivių ir bepiločių orlaivių gamybos patirties bei pajėgumų ir taip dar labiau išsiplečia įmonės galimybės vykdyti žvalgybą naudojant „oras–žemė“ jutiklius. „Atol Aviation“ vykdo veiklą Hali, Suomijoje, buvusioje Suomijos karinių oro pajėgų bazėje, kurioje įmonė sukūrė „Atol Aurora“ amfibinį orlaiv...